A Look At NXP Semiconductors (NXPI) Valuation As Strong Q1 2026 Beat Lifts Growth Expectations

NXP Semiconductors NV NXPI | 0.00 |

NXP Semiconductors (NXPI) grabbed investor attention after reporting Q1 2026 results with revenue of US$3.18b and net income of US$1.12b, alongside above-consensus guidance for Q2 that emphasized automotive, industrial and AI-related demand.

The latest Q1 surprise has come on top of a strong run, with a 51% 30 day share price return and a 60% 1 year total shareholder return pointing to building momentum around NXP’s AI and automotive story.

If this earnings move has you rethinking the chip space, it could be a good moment to scan for other potential beneficiaries of AI infrastructure demand using our focused screener of 37 AI infrastructure stocks

With NXP trading around US$295, just above its average analyst target and carrying a modest value score, the rapid 60% 1 year return raises the real question: is there still an entry point here, or has the market already priced in future growth?

Most Popular Narrative: 13.2% Overvalued

At around $295, the most followed narrative pegs NXP Semiconductors' fair value closer to $261, which creates a clear valuation gap to interrogate.

NXP's disciplined cost management, ongoing portfolio optimization, and plans to resume share buybacks in Q3 are expected to support operating leverage and drive mid-term EPS growth. In addition, manufacturing consolidation and hybrid sourcing are improving supply chain resilience while enabling lower fixed costs over time, supporting operating margin expansion.

Want to see what kind of revenue and margin profile underpins that fair value cut, even as buybacks and auto and IoT growth stay in focus? The key inputs pull together earnings expansion, profitability improvement and a specific profit multiple that has to hold up over time.

Result: Fair Value of $260.84 (OVERVALUED)

However, there are still clear pressure points, including intense China competition and higher operating expenses from recent acquisitions, that could challenge the optimistic fair value story.

Another Way To Look At Valuation

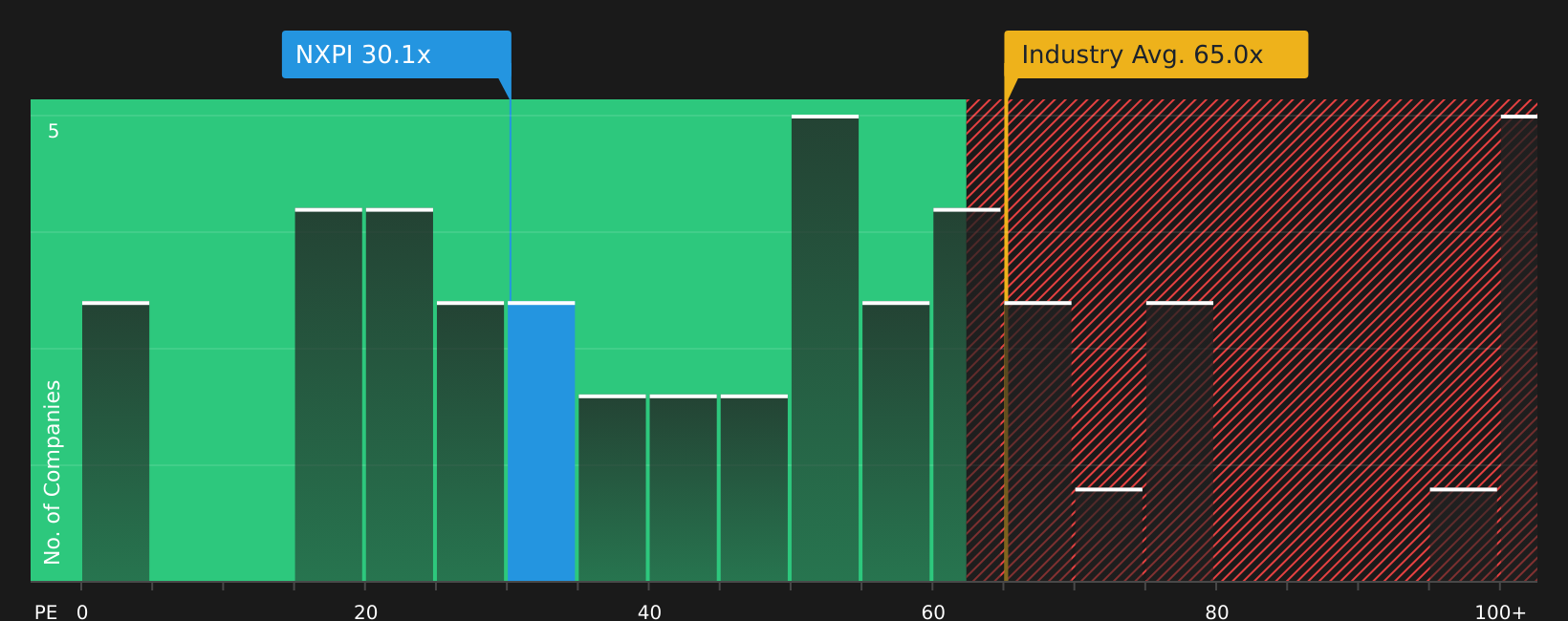

The first narrative argues NXP is about 13.2% overvalued versus a fair value of roughly $261, using earnings and growth assumptions. Yet on a simple P/E basis, the shares trade at 28.1x, well below both the US Semiconductor industry at 48.6x and peers at 71.4x, and also under an estimated fair ratio of 36.2x. That mix of signals raises a straightforward question for you: is the risk now in the growth assumptions, or in the market eventually re-rating the multiple closer to that fair ratio?

Next Steps

With all these mixed signals on value and expectations, the real edge comes from testing the numbers yourself and deciding what feels realistic. Take a closer look at both sides of the story and weigh the 4 key rewards and 1 important warning sign

Ready to hunt for more ideas?

If NXP has sharpened your thinking, do not stop here; widen your watchlist with focused screeners that surface different types of opportunities you might otherwise miss.

- Target potential mispricings by scanning for companies that look attractively valued on quality and fundamentals using the 51 high quality undervalued stocks.

- Prioritise resilience by reviewing companies that pair financial strength with cleaner balance sheets via the solid balance sheet and fundamentals stocks screener (45 results).

- Spot potential hidden winners early by checking the screener containing 25 high quality undiscovered gems before attention and capital fully catch up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.