A Look At Palo Alto Networks (PANW) Valuation After AI Automation Jitters And Recent Share Price Weakness

Palo Alto Networks, Inc. PANW | 166.97 167.46 | +1.74% +0.29% Post |

Trending interest in Palo Alto Networks (PANW) has intensified after fresh AI automation releases from Anthropic and OpenAI fed the “AI replacement” narrative, pressuring tech and cybersecurity stocks and raising questions about software revenue durability.

Those AI driven worries have come on top of existing concerns around valuation and acquisition risk, with the share price at US$159.32 after a 17.8% 30 day share price decline and a 24.9% 90 day share price decline. Even so, the 3 year total shareholder return of 92.8% and 5 year total shareholder return of 141.9% still reflect a strong longer term run.

If AI security is your focus and you want to see how other names are being priced, now could be a good time to scan our list of 56 profitable AI stocks that aren't just burning cash.

With Palo Alto Networks now at US$159.32 after a sharp pullback, yet still carrying a premium P/E versus the wider software sector and trading at a discount to analyst targets, is recent weakness a genuine opening or simply the market coolly recalibrating expectations for future growth?

Most Popular Narrative: 33.6% Undervalued

According to the most followed narrative on Simply Wall St, Palo Alto Networks' fair value sits at $240.06 versus the last close of $159.32, a sizeable gap that frames the current pullback in a very different light.

Palo Alto Networks represents the clearest beneficiary of cybersecurity's inevitable platform consolidation. As the world's largest cybersecurity company ($130B market cap, $9B+ revenue), PANW has successfully transformed from a firewall vendor into a comprehensive security ecosystem that customers increasingly view as essential infrastructure.

Curious what kind of revenue climb, margin profile, and future profit multiple are baked into that $240.06 figure? The narrative leans heavily on platform consolidation, assumes meaningful earnings expansion over time, and applies a premium valuation usually reserved for category leaders without spelling out every step in the model.

Result: Fair Value of $240.06 (UNDERVALUED)

However, that story could unravel if growth slows after the recent pullback in returns or if the CyberArk integration fails to deliver the expected revenue benefits.

Another View: High P/E Flags a Very Different Message

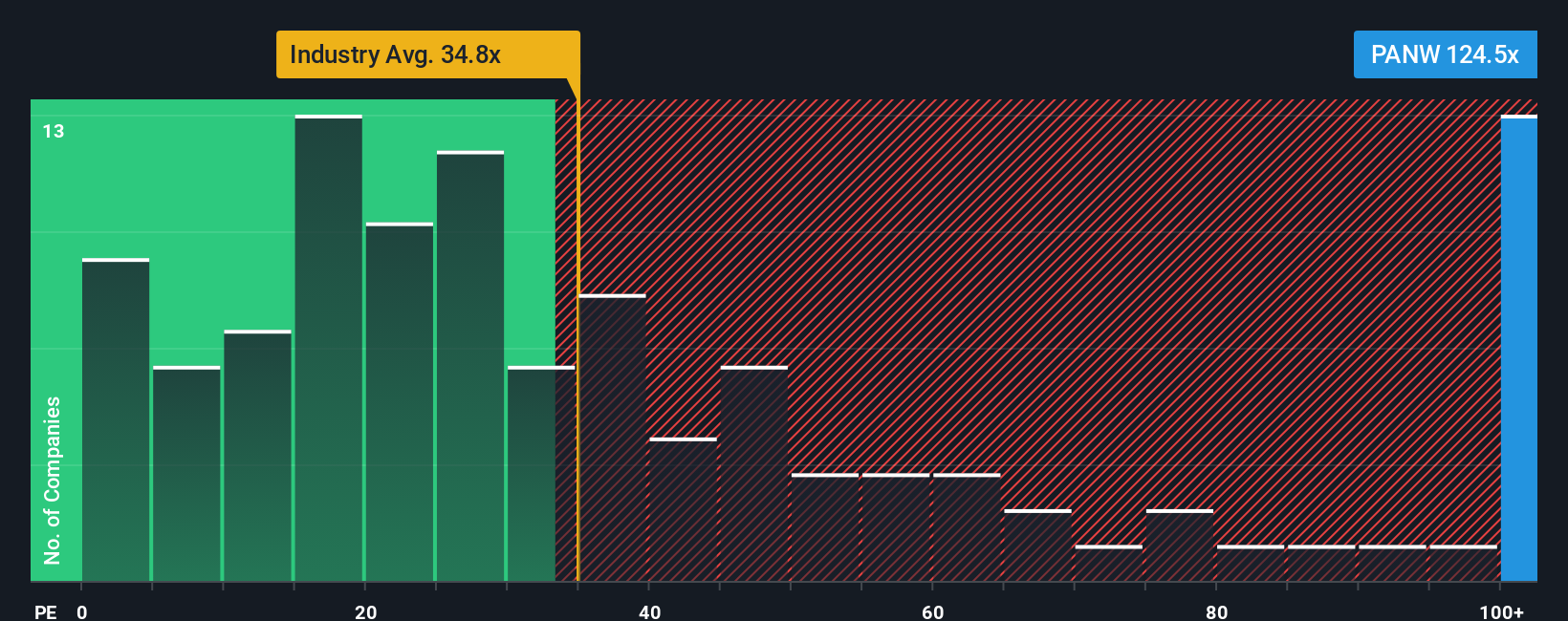

That user narrative and our DCF work both point to Palo Alto Networks trading below an estimated fair value, yet the simple P/E picture is far less forgiving. At $159.32, the stock sits on a 99.4x P/E, versus a 38.5x fair ratio, 34.8x peer average, and 26.9x for the wider US Software group. That gap suggests a lot of optimism is still baked into the price. The key question is whether future earnings can justify paying such a premium.

Build Your Own Palo Alto Networks Narrative

If you feel the market story here does not quite fit your view, you can stress test the numbers yourself and build a custom thesis in minutes by starting with Do it your way.

A great starting point for your Palo Alto Networks research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready For More Investment Ideas?

If Palo Alto Networks has sharpened your thinking, do not stop here. Broaden your watchlist with focused ideas that match how you like to invest.

- Target potential value opportunities by scanning our 53 high quality undervalued stocks that combine quality fundamentals with prices that some investors may see as appealing.

- Prioritise resilience by checking out 86 resilient stocks with low risk scores, built around companies with lower risk scores that may suit a more cautious approach.

- Hunt for fresh opportunities by reviewing our screener containing 24 high quality undiscovered gems, where strong fundamentals have not yet attracted widespread attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.