A Look At Personalis (PSNL) Valuation After New ASCO Data On NeXT Personal MRD Platform

Personalis PSNL | 0.00 |

ASCO data puts NeXT Personal in focus

Personalis (PSNL) is back in the spotlight after releasing new clinical data at the 2026 ASCO Annual Meeting on its NeXT Personal platform for ultrasensitive minimal residual disease detection across six solid tumor types.

For you as an investor, the key takeaway is that ASCO collaborators reported early relapse detection ahead of imaging, sensitivity at very low ctDNA levels, and links between molecular clearance and future recurrence or progression across colorectal, lung, ovarian, endometrial, melanoma, and renal cell cancers.

The stock has pulled back recently, with a 1-day share price return of 6.6% lower and a 7-day share price return of 10.8% lower. However, the 30-day share price return of 67.9% and 1-year total shareholder return of 85.9% suggest momentum has been building over a longer window despite volatility around the ASCO data and other news.

If you are interested in how other cancer and AI focused platforms are trading, it is worth scanning opportunities in 39 healthcare AI stocks

With the stock up 67.9% over 30 days and 85.9% over 1 year, yet trading only about 8% below the average analyst target, you have to ask: Is Personalis still mispriced, or is the market already baking in future growth?

Most Popular Narrative: 7.5% Undervalued

Analysts see fair value at $10.86 per share versus the latest close of $10.04. As a result, the current narrative leans toward a modest undervaluation with tight upside to the target.

The analysts have a consensus price target of $10.86 for Personalis based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $13.0, and the most bearish reporting a price target of just $9.0.

Want to know what kind of revenue ramp, margin shift, and future earnings multiple are built into that fair value story? The narrative reflects expectations of strong top line expansion, a turn toward healthier profitability assumptions, and a premium P/E that is closer to high growth leaders than mature life sciences peers.

Result: Fair Value of $10.86 (UNDERVALUED)

However, this hinges on timely reimbursement decisions and managing high cash usage; any setbacks here could quickly challenge both the growth story and valuation case.

Another View: Price Versus Sales Tells A Tougher Story

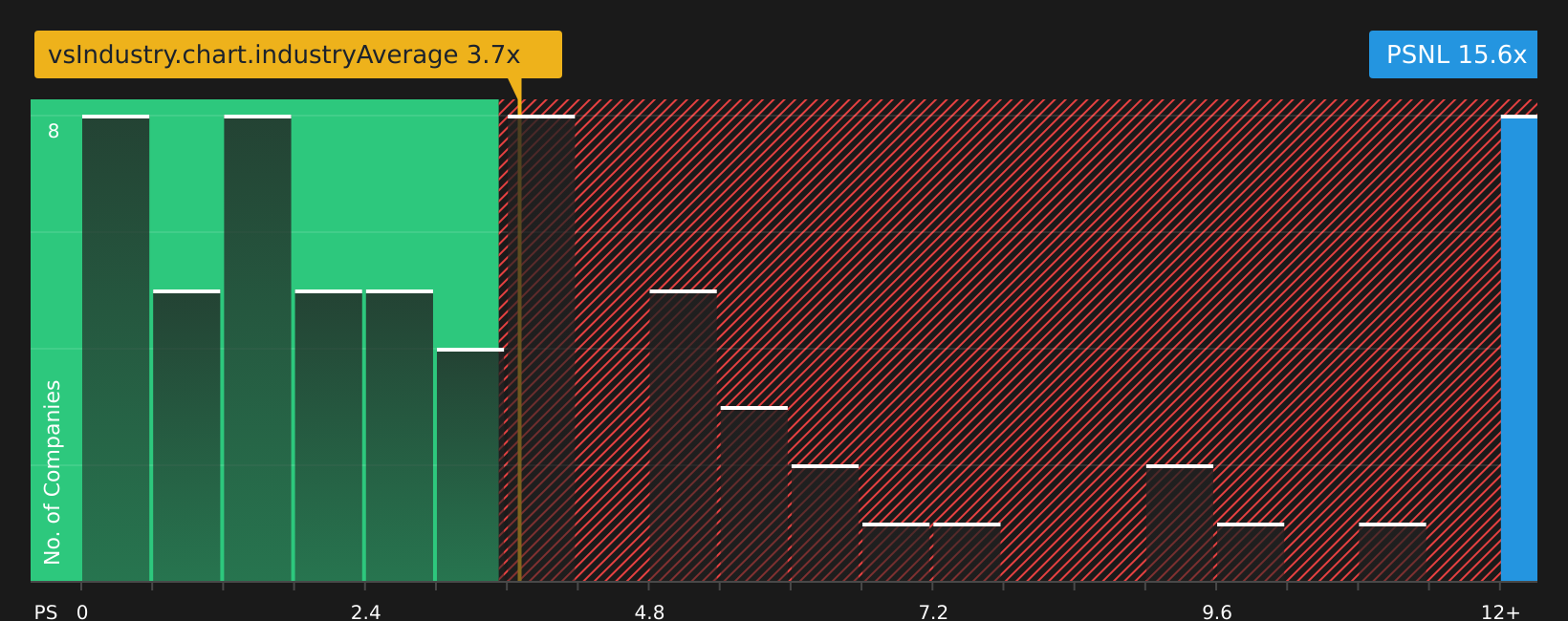

The analyst target suggests roughly 7.5% upside, but the current P/S of 16.3x is far higher than the US Life Sciences industry at 3.7x, the peer average at 7.5x, and the fair ratio of 3.5x. That gap points to meaningful valuation risk if sentiment cools.

To see what the numbers say about this price, check the valuation breakdown in See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given this mix of excitement and concern around Personalis, it makes sense to review the full picture quickly and form your own view using the 1 key reward and 3 important warning signs.

Looking for more investment ideas?

If Personalis has caught your attention, do not stop there. A few minutes exploring other opportunities now could make a real difference to your portfolio later.

- Target potential high-growth outliers before they are widely followed by scanning 23 elite penny stocks with strong financials that already show stronger financial foundations.

- Zero in on companies where quality and valuation work together by reviewing the 47 high quality undervalued stocks that meet your return and risk preferences.

- Strengthen the core of your holdings with the solid balance sheet and fundamentals stocks screener (46 results) if you want stocks that prioritize resilience and financial discipline.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.