A Look At Philip Morris International (PM) Valuation After Recent Share Price Moves

Philip Morris International Inc. PM | 0.00 |

Why Philip Morris International is on investors’ radar today

Philip Morris International (PM) has drawn fresh attention after its recent share move, with the stock closing at $173.66. Investors are weighing this latest pricing against recent returns and the company’s current fundamentals.

The latest move to $173.66 comes after a 1-month share price return of 4.38%, while the stock is down 3.00% on a 3-month share price basis and the 1-year total shareholder return declined 1.40%. This suggests that short term momentum looks softer than its strong 3 and 5 year total shareholder returns of 116.61% and 128.43%.

If Philip Morris International has you reassessing your watchlist, it can be useful to widen the lens and look at other income and defensively tilted companies via our 20 top founder-led companies

So with Philip Morris International trading at $173.66, solid recent multi year returns and analyst targets sitting higher, is the stock offering you a valuation gap today, or is the market already pricing in its future growth?

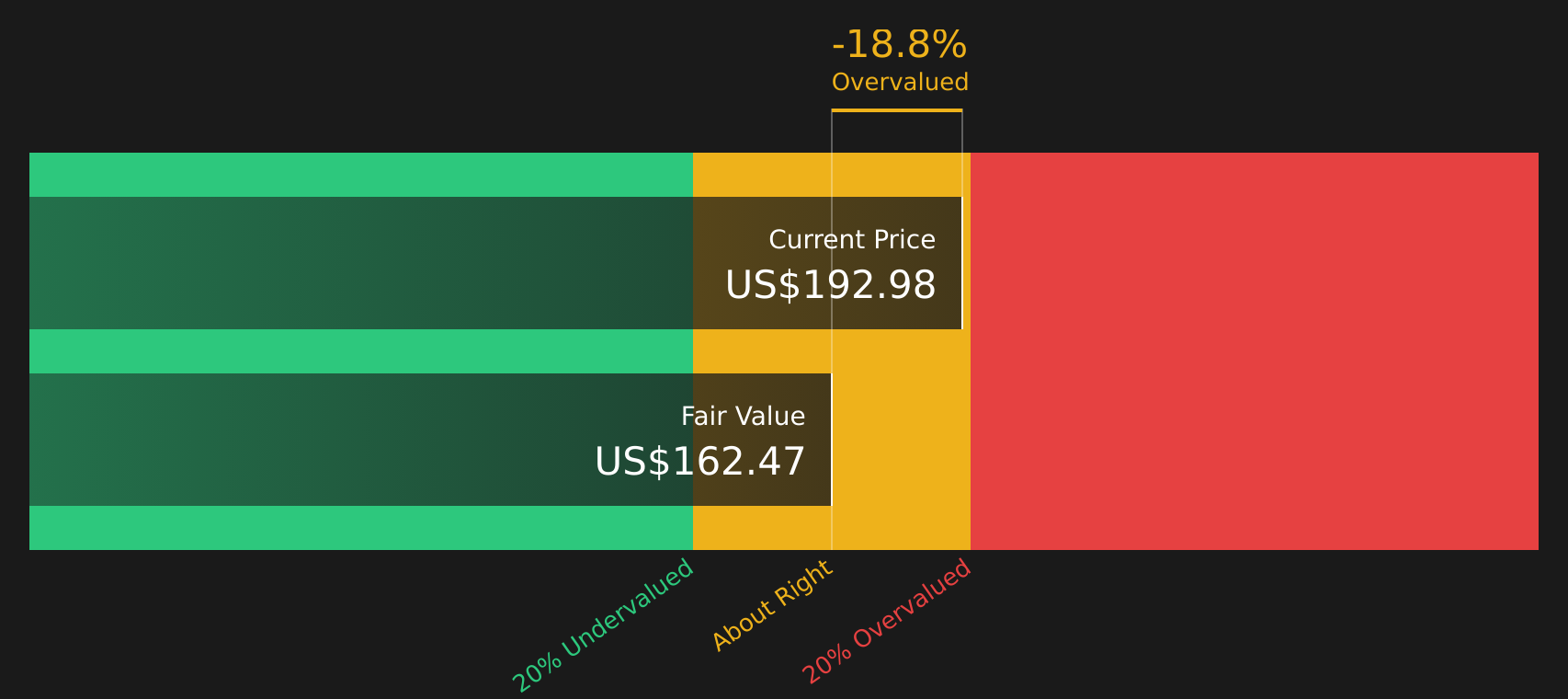

Most Popular Narrative: 10.1% Undervalued

On the most followed narrative, Philip Morris International's fair value of $193.14 sits above the last close at $173.66, with that gap resting on a detailed view of smoke free growth and margins.

The accelerating global adoption of smoke-free alternatives, driven by increasing health awareness and regulatory moves away from combustibles, is associated with strong double-digit volume and margin growth in PMI's IQOS, ZYN, and VEEV platforms. This secular shift allows the company to reach new consumer segments, expand its addressable market, and structurally increase net revenues and operating margins over time.

Curious what sits behind that fair value gap? The narrative places significant emphasis on smoke free earnings, rising profitability and a future earnings multiple that assumes those trends hold.

Result: Fair Value of $193.14 (UNDERVALUED)

However, the picture can change quickly if regulatory taxes on smoke free products rise faster than expected, or if smoke free growth slows and fails to offset cigarette declines.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Way To Look At Value

Analysts see Philip Morris International as 10.1% undervalued based on a fair value of $193.14, but a different lens tells a cooler story. Our DCF model values future cash flows at $160.03 per share, which is below the current $173.66 price and points to an overvalued result instead.

That gap between what the cash flows suggest and what the smoke free narrative supports raises a simple question for you: are expectations being set too high, or is the model too cautious on long term earnings power?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Philip Morris International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and caution has you on the fence, act now by digging into both sides of the story and weighing the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Philip Morris International has sharpened your focus, do not stop here. Broaden your opportunity set now and let data driven tools surface fresh stock ideas.

- Spot potential upside by checking companies our screener flags as mispriced on quality and fundamentals through the 46 high quality undervalued stocks.

- Strengthen your income stream by reviewing higher yielding opportunities screened via the 11 dividend fortresses.

- Dial down portfolio risk by focusing on companies filtered for resilience and lower risk profiles using the 63 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.