A Look At Plains GP Holdings (PAGP) Valuation As New Shelf Registration Raises Dilution Questions

Plains GP Holdings LP Class A PAGP | 0.00 |

Plains GP Holdings (PAGP) recently filed a shelf registration for up to US$938.9 million of Class A shares, giving the company flexibility to raise equity capital that could affect future dilution and investor sentiment.

At a share price of US$24.06, Plains GP Holdings has logged a 90 day share price return of 23.96% and a 1 year total shareholder return of 26.46%. The new US$938.9 million shelf registration gives context to this recent momentum after a strong 3 year total shareholder return of about 12x and a very large 5 year total shareholder return.

If this kind of move has you curious about what else is out there, it could be a good time to size up 28 power grid technology and infrastructure stocks

With the share price near US$24 and a recent US$938.9 million shelf registration in place, investors may question whether Plains GP Holdings is still trading at a discount or if the market is already pricing in future growth.

Most Popular Narrative: 15.4% Overvalued

Compared with the last close of $24.06, the most followed narrative points to a fair value of about $20.85, which frames the recent strength in a different light.

The analysts have a consensus price target of $21.458 for Plains GP Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.0, and the most bearish reporting a price target of just $17.5.

Want to see what is behind that spread in targets and fair value? The narrative leans on specific revenue paths, margin shifts and a future profit multiple that may surprise you.

Result: Fair Value of $20.85 (OVERVALUED)

However, the story could change quickly if crude demand softens or Permian volumes disappoint, particularly given heavier capital needs and greater exposure to regulatory shifts.

Another Angle on Valuation

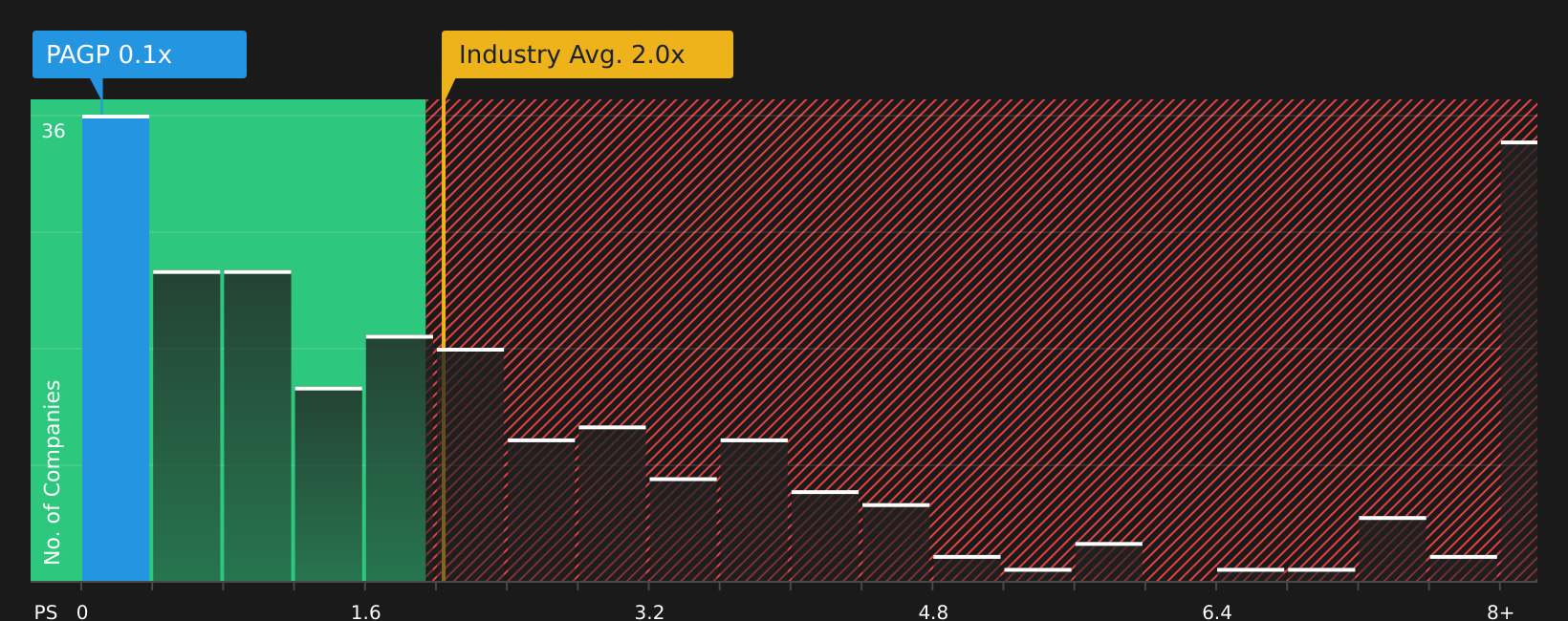

The narrative work points to a fair value of about $20.85 and labels Plains GP Holdings as overvalued at $24.06, but the P/S ratio tells a very different story. The current P/S of 0.1x sits far below the US Oil and Gas industry at 2.1x, peers at 6.4x, and a fair ratio of 0.6x. This signals a wide gap that the market could potentially close over time. The key question is whether the share price is stretched, or whether the sales-based yardstick is instead hinting at room for sentiment to shift further.

Next Steps

Mixed messages in the data so far? With investors flagging both risks and rewards around Plains GP Holdings, this is a good moment to review the numbers yourself and pressure test the narrative using 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Plains GP Holdings has your attention, do not stop here, use the Simply Wall St screener to spot other opportunities that fit the way you like to invest.

- Target value as you refine your watchlist with companies that combine quality fundamentals and attractive pricing through the 62 high quality undervalued stocks.

- Prioritize resilience by focusing on businesses with robust finances using the solid balance sheet and fundamentals stocks screener (39 results).

- Hunt for potential standouts before the crowd notices by scanning the screener containing 25 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.