A Look At Powell Industries (POWL) Valuation After Record Backlog And Major AI Data Center Win

Powell Industries, Inc. POWL | 0.00 |

Why Powell Industries (POWL) is back on investors’ radar

Powell Industries (POWL) is drawing attention after reporting a near doubling of March quarter orders, securing its largest AI data center project and lifting its order backlog to record levels.

Powell’s share price has surged recently, with a 30 day share price return of 51.68% and a year to date share price return of 160.35%, while the 1 year total shareholder return is very large. This reflects how the record US$1.8b backlog and mega AI data center project have shifted investors’ expectations, even after a 4.49% pullback in the last session.

If this kind of order driven rerating catches your attention, it is worth seeing what else is moving in power and grid infrastructure by checking the 36 power grid technology and infrastructure stocks.

With Powell trading at US$305.93 after a very strong run and sitting above the US$276.25 analyst price target, the key question now is whether the stock still offers upside or if the market is already pricing in future growth.

Most Popular Narrative: 12.6% Undervalued

Powell Industries' most followed narrative sets a Fair Value of $350.00, above the last close at $305.93. This frames the current debate around whether recent AI and grid related wins are fully reflected in the price.

The multi year build out of U.S. LNG export facilities and related natural gas infrastructure is contributing to a pipeline of large, complex projects, supporting backlog stability, higher plant utilization and stronger gross margins.

Strategic capacity expansions in Houston and ongoing productivity investments are increasing throughput and manufacturing leverage. This may enable Powell to convert its record backlog more efficiently and support higher operating margins over time.

Want to see how this backlog centric story translates into that Fair Value figure? The narrative leans on steady top line expansion, firm margins and a future earnings profile that has been priced using a 9.06% discount rate. The real curiosity is how those ingredients combine into the premium earnings multiple required to justify $350.00.

Result: Fair Value of $350.00 (UNDERVALUED)

However, this optimistic story can change quickly if LNG projects are delayed or if utility and data center orders slow, which could put backlog conversion and margins under pressure.

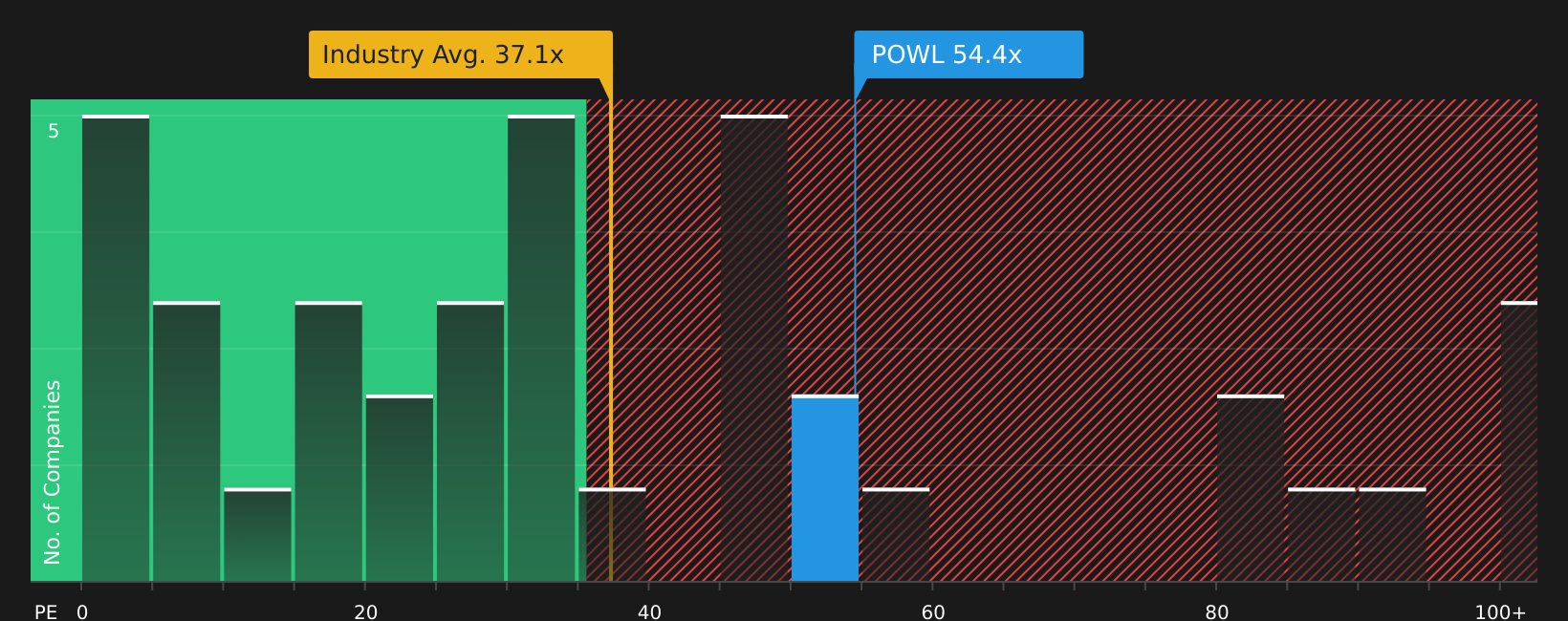

Another View: What Earnings Multiples Are Saying

The bullish narrative points to a Fair Value of $350.00, yet Powell trades on a P/E of 59.6x, compared with 36.7x for the US Electrical industry and a fair ratio of 38.1x. That is a wide gap, so is this a premium story or valuation risk building in?

Next Steps

With enthusiasm and caution both showing up in the story so far, take a moment to review the numbers yourself and decide what stands out. To balance the upside potential against the concerns investors are flagging, start by checking the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Powell has grabbed your attention, do not stop here. Broadening your watchlist with other clear ideas could help you prepare for your next move.

- Target potential value opportunities by scanning 51 high quality undervalued stocks that pair strong fundamentals with prices that may not fully reflect them yet.

- Strengthen your income focus by checking 12 dividend fortresses that combine higher yields with resilience around their payouts.

- Prioritise peace of mind by reviewing 71 resilient stocks with low risk scores designed to highlight companies with steadier risk profiles and solid underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.