A Look At Privia Health Group (PRVA) Valuation After Recent Share Price Pressure

Privia Health Group, Inc. PRVA | 22.38 22.38 | +3.66% 0.00% Post |

Privia Health Group (PRVA) has been drawing attention after recent share price pressure, with the stock showing negative returns over the past month and past 3 months as investors reassess expectations.

With the latest share price at $20.02, the stock’s 30 day share price return of 11.61% and year to date share price return of a 14.66% decline sit alongside a 3 year total shareholder return of a 27.49% decline, pointing to fading momentum as investors reassess the risk and growth trade off.

If you are weighing what to do next after Privia Health Group’s recent pullback, it can help to see how other healthcare names are trading by scanning 34 healthcare AI stocks

After a tough stretch for the share price, with analysts’ targets and intrinsic value models still sitting well above the current US$20.02 level, investors are left asking whether this weakness is a fresh entry point or if the market is already pricing in future growth.

Most Popular Narrative: 37.1% Undervalued

Privia Health Group's most followed valuation narrative pegs fair value at $31.85, well above the recent $20.02 close, which naturally raises questions about what assumptions sit behind that gap.

The industry wide movement towards value based care, with associated shared savings and care management fees, is enabling Privia to grow its value based attributed lives at a double digit rate and to expand margins as risk sharing agreements mature, positively impacting earnings and long term EBITDA growth.

Curious what is driving that valuation gap? Revenue growth, margin expansion and a future earnings profile are all wired into this model, but the exact mix may surprise you.

Result: Fair Value of $31.85 (UNDERVALUED)

However, this story can change quickly if healthcare labor costs keep climbing, or if tighter regulations push up compliance expenses and squeeze margins more than expected.

Another Way to Look at Valuation

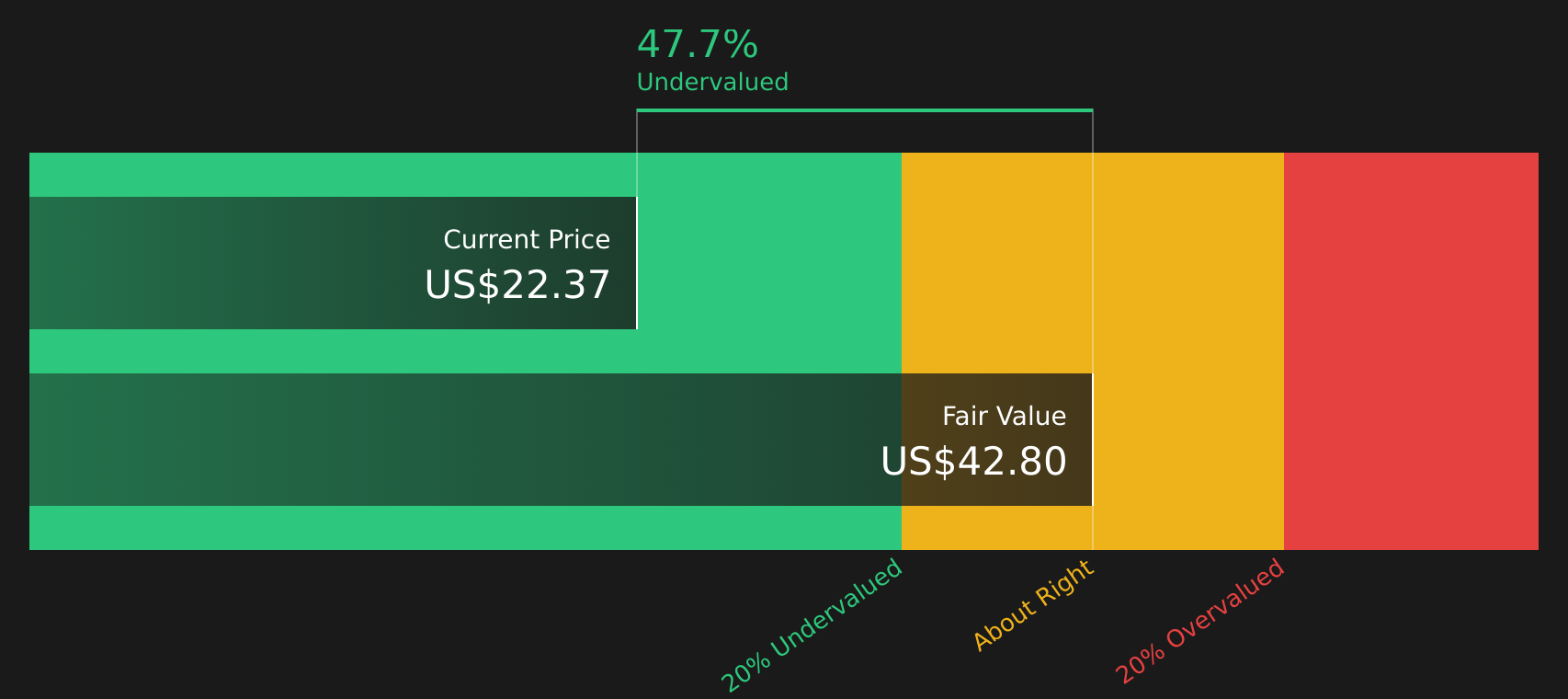

The SWS DCF model paints an even stronger picture, with PRVA at $20.02 compared with an estimated future cash flow value of $42.82. That flags the shares as undervalued on this method. It also raises a key question: are the cash flow assumptions too generous, or is the market too cautious?

Next Steps

Mixed signals on value and risk so far. If you want to move faster than the crowd, consider those trade offs carefully and review the full picture via 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If you only focus on Privia, you could miss other opportunities that fit your goals, so broaden your watchlist with a few targeted stock ideas.

- Spot potential value opportunities early by scanning 60 high quality undervalued stocks that combine quality fundamentals with pricing that may not fully reflect those characteristics yet.

- Prioritise resilience by reviewing 67 resilient stocks with low risk scores if you want companies with relatively lower risk scores to balance out your portfolio.

- Hunt for off the radar potential by checking the screener containing 26 high quality undiscovered gems that many investors may not be watching closely yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.