A Look At Procter & Gamble (PG) Valuation As It Commits US$205 Million To New Automated Facility

Procter & Gamble Company PG | 0.00 |

Procter & Gamble (PG) has committed US$205 million to a new automated distribution facility in Georgia, a logistics expansion that creates 350 jobs and could influence how investors view the stock’s U.S. supply chain footprint.

PG stock trades at US$142.96, and despite the logistics expansion, the 90 day share price return is down 12.5%, while the 1 year total shareholder return is down 12.33%. This points to fading momentum after a modest 0.83% year to date share price gain.

If you are weighing consumer staples against other themes, this could be a moment to broaden your watchlist with 20 top founder-led companies

With PG trading at US$142.96 after a 12.5% decline over 90 days and showing steady annual revenue and net income growth, should you view this as an undervalued consumer staple, or assume the market is already pricing in its future growth?

Most Popular Narrative: 18.1% Overvalued

According to the most followed valuation narrative, Procter & Gamble’s fair value of $121.06 sits below the current $142.96 share price, which puts the latest logistics expansion into a tighter pricing context.

Procter & Gamble, despite being within a very competitive industry, still has some competitive advantages shown in its higher operating margin above the approximately 20% mark and the Morning Star Wide Moat. Also, the fact that the ROIC is double the Cost of Capital means its capital allocation is being well managed.

This narrative leans heavily on premium margins, strong returns on capital, and disciplined capital costs. It blends them with moderate growth expectations and a conservative hurdle rate to reach that fair value.

Result: Fair Value of $121.06 (OVERVALUED)

However, this overvaluation call could be challenged if PG’s wide moat supports earnings resilience or if sentiment shifts toward defensive, cash-generative consumer stocks.

Another Angle on Value

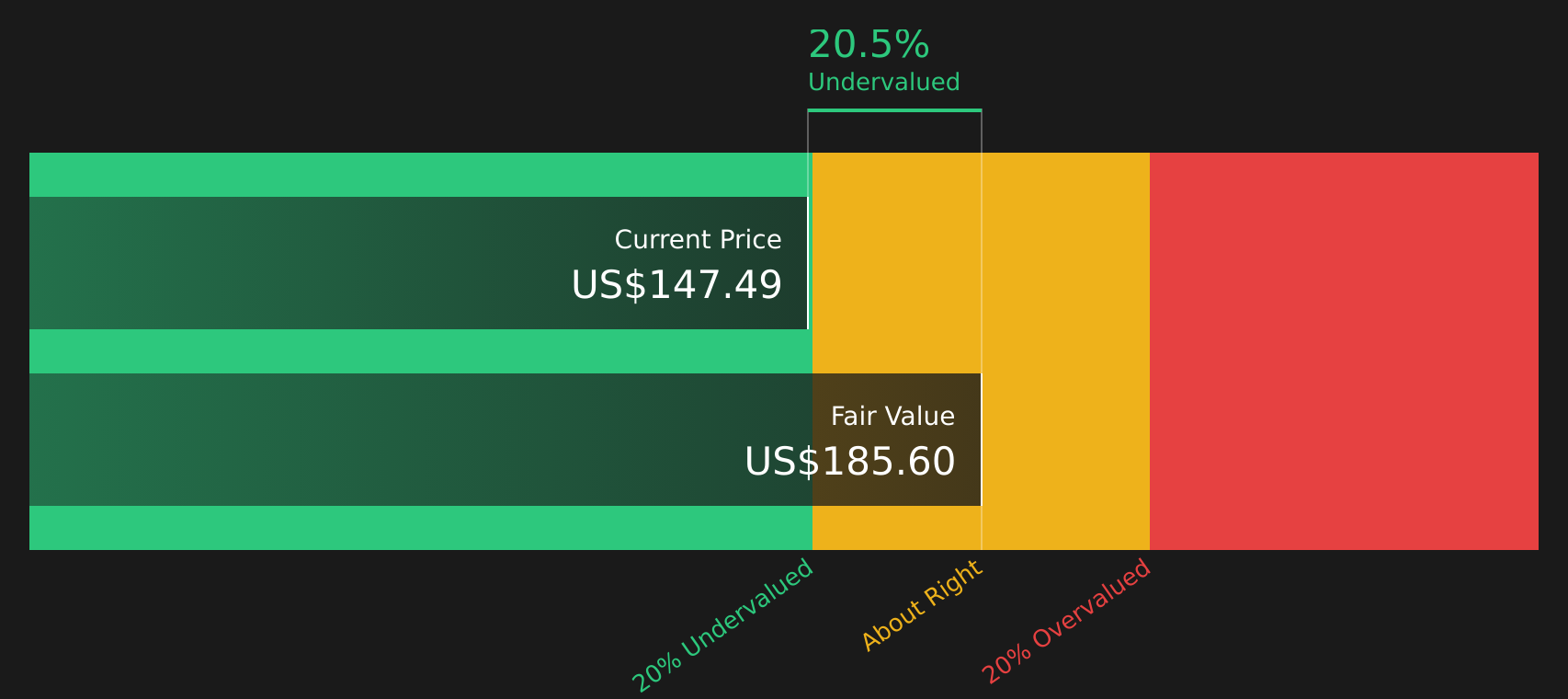

There is a sharp contrast between the user narrative that points to a fair value of $121.06 and our own SWS DCF model, which indicates PG at $142.96 trades around 23% below an estimated future cash flow value of $185.60. That split raises a simple question: which framework do you trust more for a slow growing, high margin business like this?

For readers who want to see how those cash flow assumptions translate into a single number over time, Look into how the SWS DCF model arrives at its fair value.

Next Steps

With mixed signals across price, valuation, and fundamentals, are you seeing caution or opportunity here, and how quickly do you want to test that view against the data and narratives behind PG's 1 or more risks and 1 or more rewards? To weigh those factors side by side and pressure test your own stance, start with 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If you want to stress test your PG view, do not stop here. Broaden your opportunity set with focused screeners built to surface clear, data driven ideas.

- Target income first and review companies offering resilient cash returns through 10 dividend fortresses

- Zero in on quality at a reasonable price and scan 46 high quality undervalued stocks for candidates to add to your watchlist.

- Prioritise capital preservation and filter for stability using the 65 resilient stocks with low risk scores so you do not miss lower volatility options.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.