A Look At Rackspace Technology (RXT) Valuation After New AI Partnerships And Reaffirmed 2026 Guidance

Rackspace Technology, Inc. RXT | 0.00 |

Rackspace Technology (RXT) is back on investor radar after a fresh memorandum of understanding with AMD and expanded AI partnerships, along with reaffirmed 2026 guidance following Q1 revenue and EPS results that topped expectations.

The stock has swung sharply higher in recent weeks, with a 1 month share price return of 234.46% and a year to date share price return above 5x. However, the 1 year total shareholder return of 474.76% follows a much weaker 5 year total shareholder return.

If this AI focused story has you looking beyond a single stock, it could be a good time to scan for other opportunities in enterprise AI and infrastructure through our 47 AI infrastructure stocks

After a swing like this, investors are left with a simple but important question: Is Rackspace still trading below what its fundamentals and AI partnerships might justify, or is the market already pricing in years of future growth?

Most Popular Narrative: 173.2% Overvalued

Rackspace closed at $5.92, while the most followed narrative puts fair value closer to $2.17, so the market price currently sits well above that model.

Ongoing digital transformation and increasing complexity of hybrid or multi cloud environments are driving strong demand for Rackspace's managed cloud services, as evidenced by double digit year over year bookings growth and a shift toward larger, longer term enterprise contracts. This is likely to support a sustained rebound in revenue and enhance revenue visibility.

Curious what kind of revenue mix shift and margin profile would need to line up with that demand story to support the modeled fair value and earnings path.

Result: Fair Value of $2.17 (OVERVALUED)

However, there are still clear execution risks, including declining Public and Private Cloud revenues, as well as pressure on margins and free cash flow that could challenge this upbeat narrative.

Another View: Cash Flows Tell a Different Story

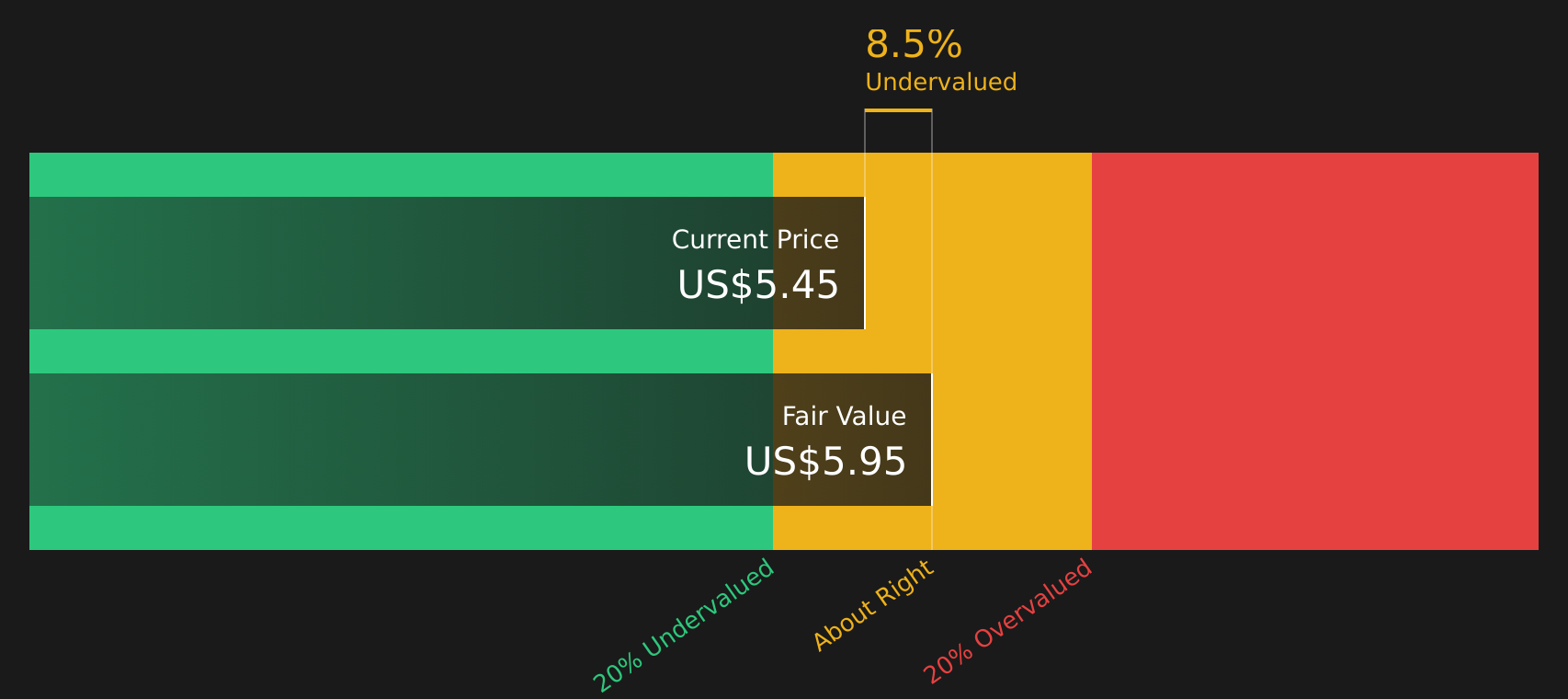

While the most followed narrative flags Rackspace as about 173% above its modeled fair value at $2.17, our DCF model paints a more balanced picture, with the stock at $5.92 trading just below an estimated future cash flow value of $5.95. That split begs the question: which set of assumptions do you trust more, the story built around earnings multiples or the one grounded in cash flow?

Next Steps

If this mix of risks and potential rewards feels finely balanced, move quickly to review the figures for yourself and weigh both sides using the 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

If Rackspace has sharpened your focus, do not stop here. Broaden your watchlist with other stocks that align with your goals using the Simply Wall Street Screener.

- Target potential upside across quality companies that trade below their assessed worth through our 47 high quality undervalued stocks.

- Prioritise stability and capital preservation by scanning stocks with lower risk profiles using the 62 resilient stocks with low risk scores.

- Hunt for less followed opportunities with solid fundamentals by checking the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.