A Look At RB Global (RBA) Valuation After Strong First Quarter Earnings And Recent Share Price Move

RB Global, Inc. RBA | 0.00 |

RB Global (RBA) reported first quarter results with revenue of US$1,234.6m and net income of US$135.5m, compared with US$1,108.6m and US$113.4m a year earlier, drawing fresh attention to the stock.

The stock has moved higher in the very short term, with a 1 day share price return of 1.11%, but the 90 day share price return is down 12.35%, while the 3 year total shareholder return of 104.45% points to a very strong longer term outcome. Recent quarterly earnings, the confirmed quarterly dividend and the addition of a new director give investors fresh information to weigh against that mixed momentum.

If this earnings update has you thinking about where else growth and income stories might be building, it could be worth scanning 19 top founder-led companies

With the stock near US$104 and trading at a sizeable discount to the average analyst price target and an indicated intrinsic value gap, the key question is whether this is a genuine opportunity or whether the market already anticipates future growth.

Most Popular Narrative: 15.9% Undervalued

RB Global's most followed narrative points to a fair value of about $124.20 per share, compared with the last close at $104.43. That puts the focus firmly on what has to go right for that gap to close.

Expansion of the international buyer base and new alliance partnerships, along with ongoing growth in e-commerce marketplace activities, are expected to drive higher transaction volumes and revenue as more asset sales and auctions move online.

Curious what kind of revenue mix, margin lift and future earnings multiple are baked into that fair value? The full narrative spells out a precise growth path, share count assumptions and a required valuation reset that goes well beyond simple top line forecasts.

Result: Fair Value of $124.20 (UNDERVALUED)

However, this depends heavily on execution. A slowdown in transaction volumes from cautious buyers, or weaker results from recent acquisitions, could quickly challenge the upbeat fair value narrative.

Another Angle on Valuation

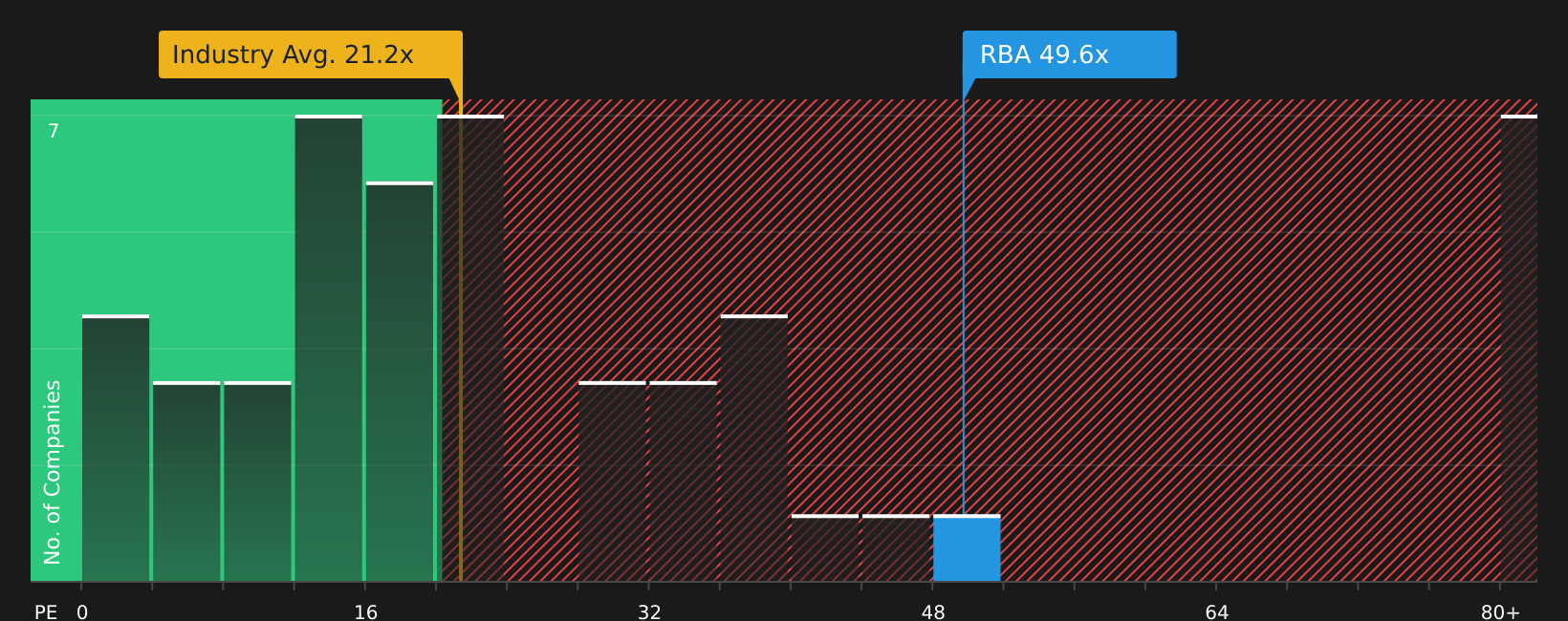

The fair value narrative points to RB Global trading 48.3% below an estimated intrinsic value, yet the current P/E of 48.3x is far above the industry at 22.3x and a fair ratio of 30.6x. That gap suggests investors need to weigh upside potential against the risk of a P/E reset.

For a closer look at what the numbers imply about this pricing gap, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mix of optimism and caution in this update, it makes sense to act promptly, review the underlying data, and evaluate the potential upside for yourself by checking the 4 key rewards

Looking for more investment ideas?

If you stop here, you risk missing other stocks that might fit your goals, so take a few minutes to widen your watchlist with fresh ideas.

- Target potential bargains by scanning 47 high quality undervalued stocks that combine attractive pricing with solid underlying fundamentals.

- Strengthen your income stream by reviewing 12 dividend fortresses that focus on higher yielding, income oriented opportunities.

- Dial down portfolio risk by checking 70 resilient stocks with low risk scores built around companies with more resilient profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.