A Look At RLJ Lodging Trust (RLJ) Valuation After Conflicting Analyst Calls And Sector Rally

RLJ Lodging Trust RLJ | 7.35 | +0.27% |

RLJ Lodging Trust (RLJ) is back in focus after two contrasting analyst calls, with Barclays taking a cautious view on leverage and hotel mix, while Raymond James issued an upgrade following strong quarterly results and a sector rally.

At a share price of US$7.70, RLJ has posted an 11.11% 3 month share price return. However, its 1 year total shareholder return of 14.06% decline and 5 year total shareholder return of 36.29% decline suggest that recent momentum contrasts with a tougher longer term picture. The recent analyst debate and hotel REIT sector rally are likely influencing how investors view its income potential and balance sheet risk.

If you are weighing up hotel REITs against other areas of the market, this could be a useful moment to broaden your search and check out fast growing stocks with high insider ownership.

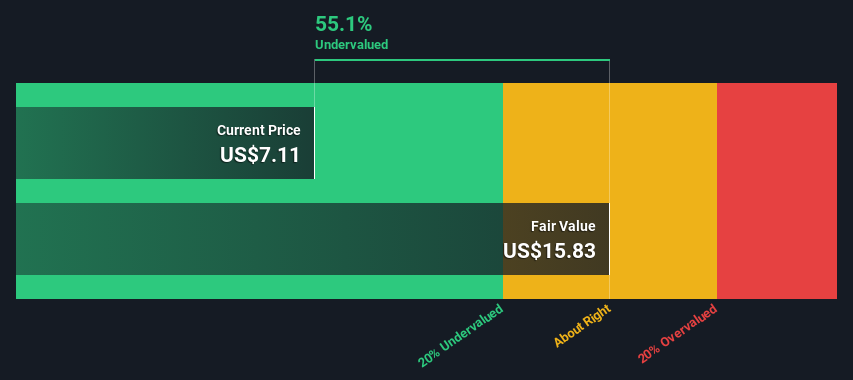

With RLJ trading at US$7.70, a 9.42% discount to the average analyst price target and a 35.70% intrinsic discount estimate, the key question is whether this gap signals a genuine opportunity or whether the market is already factoring in future growth.

Price-to-Sales of 0.8x: Is it justified?

RLJ Lodging Trust is trading on a P/S of 0.8x at a last close of US$7.70, which screens as inexpensive compared to both peers and the wider hotel REIT space.

The P/S ratio compares the company’s market value to its annual revenue. For a hotel REIT like RLJ it gives you a clean read on what investors are currently paying for each dollar of hotel revenue, regardless of short term earnings swings.

RLJ’s 0.8x P/S is below the peer average of 1.5x and also below the Global Hotel and Resort REITs industry average of 3.8x. This suggests the market is attaching a lower valuation to its revenue stream than to comparable hotel REITs. Relative to an estimated fair P/S of 1.4x, it also sits at a discount, which could be a level the valuation moves closer to if sentiment or fundamentals line up with those expectations.

Result: Price-to-Sales of 0.8x (UNDERVALUED)

However, the long term total shareholder return decline, together with RLJ’s modest US$7.2m net income on US$1.35b revenue, leaves little room if operating trends or financing costs worsen.

Another view: DCF points to a wider gap

Our DCF model puts RLJ Lodging Trust’s fair value at US$11.97 per share, versus the current US$7.70. That 35.7% discount also frames the stock as undervalued, but in a stronger way than the 0.8x P/S suggests. So which signal do you treat as more important?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out RLJ Lodging Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own RLJ Lodging Trust Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a personalised view in just a few minutes, starting with Do it your way.

A great starting point for your RLJ Lodging Trust research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one stock, you could overlook other opportunities that better match your goals, risk comfort, and income or growth preferences.

- Target potential growth early by checking out these 3556 penny stocks with strong financials that already carry strong financials instead of chasing stories without numbers behind them.

- Position yourself in one of the most talked about themes by scanning these 26 AI penny stocks and focusing on businesses where AI is tied to real revenues.

- Focus on value opportunities by reviewing these 877 undervalued stocks based on cash flows and comparing their cash flow profiles with what you are seeing in RLJ and other REITs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.