A Look At Rush Street Interactive (RSI) Valuation After Analyst Buy Ratings And Colombia Tax Update

Rush Street Interactive, Inc. Class A RSI | 22.80 | +2.10% |

Why Rush Street Interactive is back on investors’ radar

Rush Street Interactive (RSI) has drawn fresh attention after multiple analysts reiterated positive views on the stock alongside new coverage, while investors weigh the earnings impact of Colombia’s updated tax framework on its international business.

The recent run of reaffirmed Buy ratings and fresh coverage has arrived as RSI’s US$17.67 share price shows mixed momentum, with a 1 day share price return of 5.37% but a 30 day decline of 4.59%. At the same time, the 1 year total shareholder return of 25.32% and the very large 3 year total shareholder gain suggest longer term holders have experienced strong compounding despite short term swings.

If this kind of rebound after volatility interests you, it could be worth widening your watchlist to see 22 top founder-led companies that might be setting up for their next move.

With RSI trading at US$17.67 and sitting at a reported 22% intrinsic discount and around a 35% gap to the average analyst price target, you have to ask: is this a genuine opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 24.6% Undervalued

With Rush Street Interactive last closing at $17.67 against a most followed fair value estimate of about $23.43, the current gap is driving a clear valuation story built around growth, margins and discounting future cash flows at an 8.25% rate.

The digitalization of entertainment is accelerating migration from offline to online gaming, and with record-high monthly active users (MAUs) growing over 30% in North America and 40%+ in Latin America, Rush Street Interactive is well-positioned to capture this expanding addressable market, supporting sustained future revenue growth.

Want to see what powers that growth claim? The narrative leans on compound revenue gains, rising profitability and a future earnings multiple that assumes investors keep paying up. Curious which specific growth path and margin profile are baked into that $23.43 figure?

Result: Fair Value of $23.43 (UNDERVALUED)

However, this story can change quickly if Latin American tax or regulatory rules tighten again, or if heavier marketing spend begins to squeeze RSI’s margins.

Another angle: richer multiples, cheaper cash flows

So far, the story has leaned on future cash flows and a fair value of about $23.43, which points to RSI trading at a discount. If you switch to earnings multiples, you get a very different feel for the risk you are taking on at $17.67.

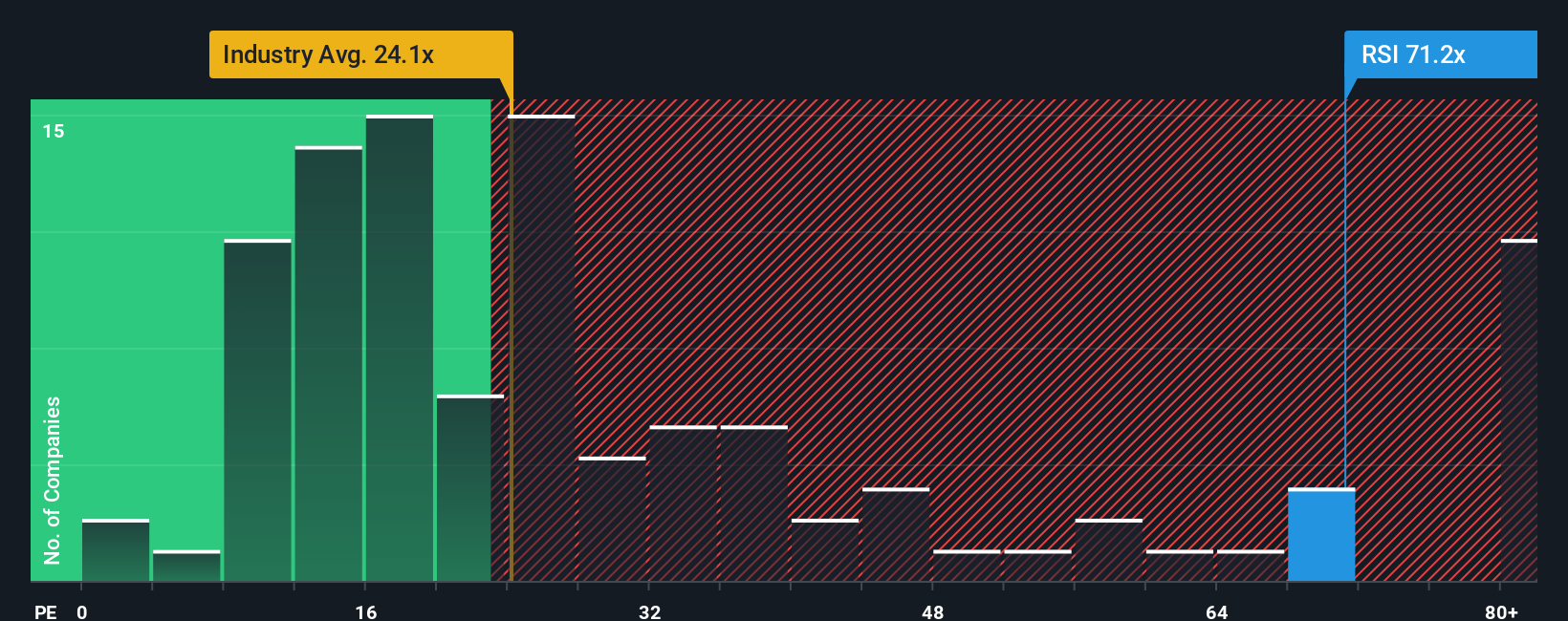

RSI currently trades on a P/E of 57.5x, compared with 21x for the US Hospitality industry, 25.5x for peer companies and a fair ratio estimate of 45.2x. In plain terms, the share price already bakes in a lot more optimism than both the sector and the fair ratio suggest. How comfortable are you paying a premium for a stock that screens as undervalued on cash flows?

Build Your Own Rush Street Interactive Narrative

If you are not fully on board with this view, or you simply want to stress test the numbers yourself, you can build a personalised thesis in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Rush Street Interactive.

Looking for more investment ideas?

If you stop with just one stock, you could miss out on better fits for your goals, so use the screener to pressure test and expand your watchlist.

- Target potential value opportunities by scanning 53 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect their financial profile.

- Prioritise resilience by reviewing 86 resilient stocks with low risk scores that score well on balance sheet strength and lower risk indicators.

- Spot early stage opportunities by checking the 25 elite penny stocks with strong financials that still meet meaningful financial quality filters instead of relying on hype.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.