A Look at Schrödinger (SDGR) Valuation Following Improved Revenue and Updated Financial Guidance

Schrodinger SDGR | 11.58 11.58 | +0.26% 0.00% Post |

Schrödinger (SDGR) just released its latest earnings and revised financial outlook, showing stronger sales and revenue for the quarter and past nine months, as well as a smaller net loss compared to last year.

After posting improved revenue numbers and nudging its drug discovery revenue targets higher, Schrödinger's share price has seen continued downward pressure, with a 1-day share price return of -2.5%, a rough month at -11.9%, and a year-to-date drop of -16.6%. Over the past year, total shareholder return has fallen 10.1%, and long-term investors have not fared well either, with a five-year total shareholder return of -74.3%. This shows momentum is still fading despite better operational results and shifting guidance.

If you're interested in what other players in the healthcare space are doing, now's a great time to explore fresh opportunities with the See the full list for free.

Given these developments, is Schrödinger trading at a bargain after steep declines and stronger earnings, or has the market already accounted for any future rebound in its current valuation?

Most Popular Narrative: 37.7% Undervalued

Schrödinger’s narrative fair value stands at $27.30, a significant premium above the last close of $17.02. This wide gap reflects optimism around the company’s software and drug discovery catalysts despite recent price declines.

Strong pipeline advancement and early clinical success, such as positive Phase I data for SGR-1505, positions the company to secure additional milestone payments, royalties, and out-licensing deals. This creates potential for substantial long-term revenue growth and more predictable future cash flows.

Want to know why consensus sees a big rebound from here? The secret lies in bold revenue acceleration, a dramatic profit turnaround, and sky-high future multiples. These numbers are not often seen for healthcare names. Curious what assumptions drive such an aggressive price target? Dig deeper to see which projections fuel this undervalued call.

Result: Fair Value of $27.30 (UNDERVALUED)

However, persistent margin pressures and continued reliance on volatile milestone revenues could quickly dampen optimism if industry headwinds become more severe.

Another View: Multiple-Based Valuation Signals Caution

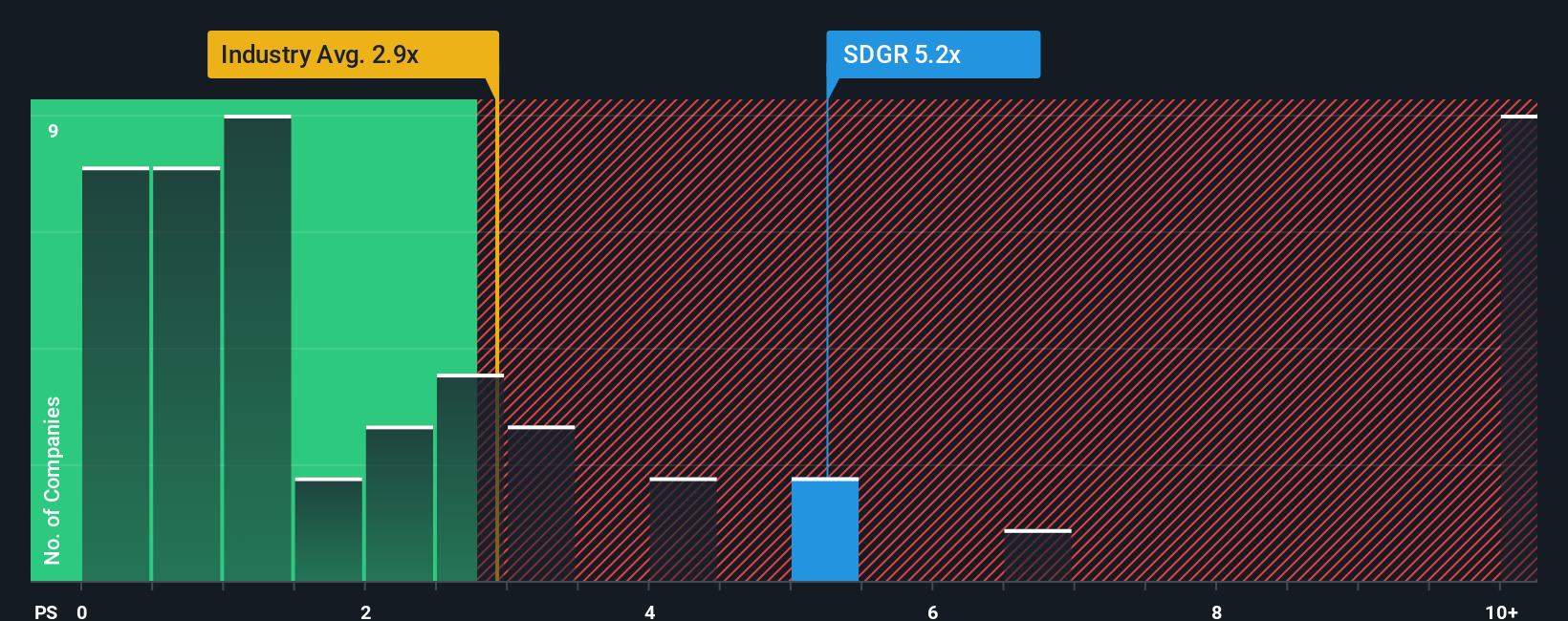

Looking through a price-to-sales lens, Schrödinger trades at a much higher ratio: 4.9x compared to the US Healthcare Services industry’s 2.7x, and peers’ average of 1.9x. This means the market is still asking investors to pay a sizeable premium, even though the fair ratio suggests a level of just 2.7x. Could this premium bring risk if growth slows, or is there hidden value that justifies the gap?

Build Your Own Schrödinger Narrative

If you want to dig deeper or see things differently, you can analyze the numbers and shape your own story in just minutes, then Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Schrödinger.

Looking for More Investment Ideas?

If you want to get ahead of the market crowd, now is the perfect time to tap new opportunities with investment themes set to disrupt entire industries. Don’t let the next winning idea slip by. These tailored picks could put you one step ahead.

- Spot game-changing tech names as you check out these 27 AI penny stocks, which are poised for powerful growth in artificial intelligence, automation, and next-generation computing.

- Boost your passive income strategies by reviewing these 18 dividend stocks with yields > 3%, where you’ll find companies offering attractive yields and a track record of consistent payouts.

- Ride early waves of innovation and hunt for breakout winners among these 3585 penny stocks with strong financials that are disrupting their spaces and offering remarkable upside potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.