A Look At Selective Insurance Group (SIGI) Valuation As Growth And Margins Show Signs Of Strain

Selective Insurance Group, Inc. SIGI | 0.00 |

Selective Insurance Group (SIGI) is back in focus after recent analyst commentary pointed to slowing demand, with estimated sales growth for the next 12 months projected at just 1.7%.

Despite concerns about slowing sales, recent trading has been firm, with a 12.13% 1 month share price return and the stock at US$90.69, while the 3 year total shareholder return has declined 3.18%, which hints that longer term momentum has been softer.

If this kind of mixed momentum has you looking around the market, it could be a good moment to see what is happening across 20 top founder-led companies

So with a projected 1.7% sales growth, a value score of 3, an intrinsic value estimate suggesting roughly a 50% gap, and the share price sitting close to analyst targets, should you see Selective Insurance Group as undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 1% Overvalued

The most popular narrative pegs Selective Insurance Group's fair value at about $90.14, which sits almost exactly in line with the latest close at $90.69, so the gap between price and model is very narrow.

The analysts have a consensus price target of $90.14 for Selective Insurance Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $100.0, and the most bearish reporting a price target of just $72.0.

Want to see what kind of earnings curve and margin profile have to line up to land almost exactly at today's price? The narrative leans on specific growth, profitability and future P/E assumptions that leave very little room for error. The exact mix of those inputs is where the story gets interesting.

Result: Fair Value of $90.14 (ABOUT RIGHT)

However, there are still clear fault lines in this story. Casualty claim severity trends and potential reserve charges are both capable of quickly challenging that finely balanced valuation.

Another Angle On Valuation

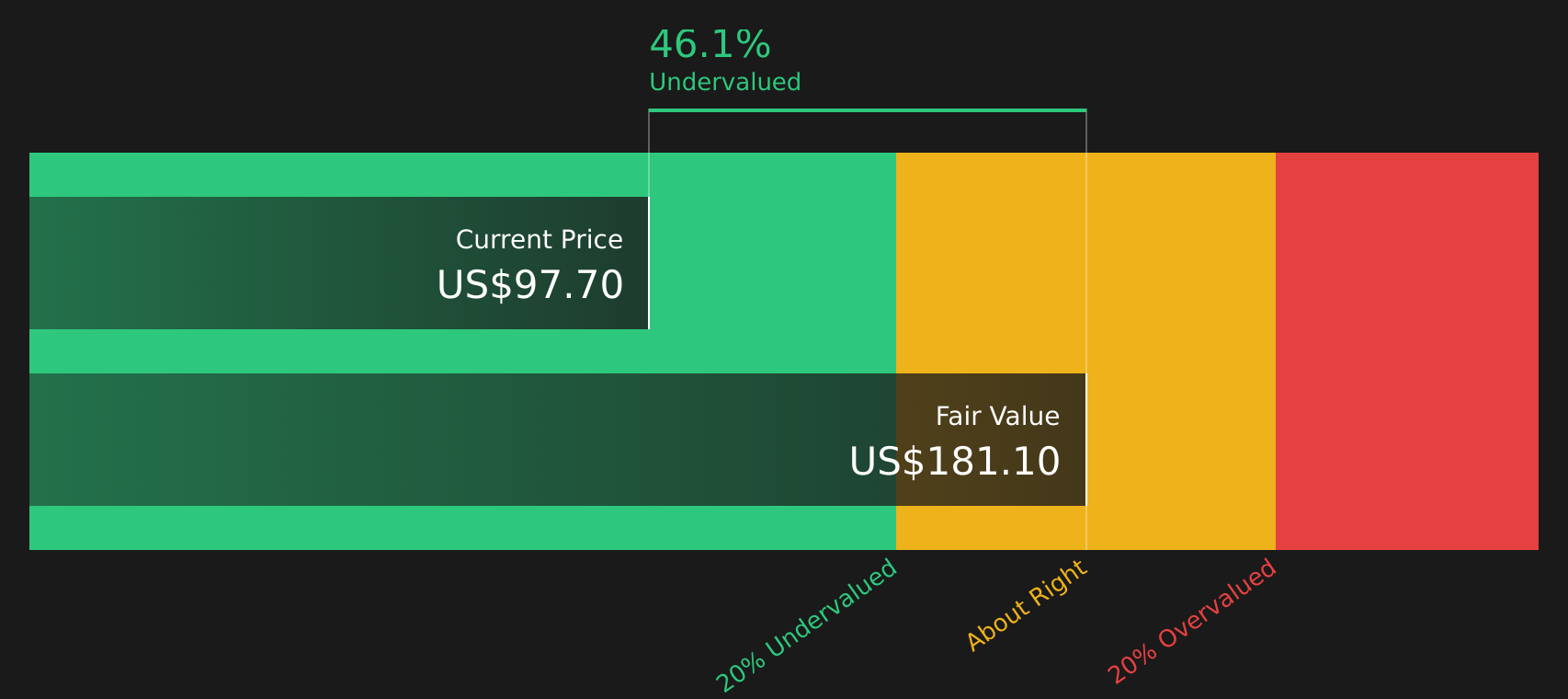

Analysts see Selective Insurance Group trading almost exactly in line with their US$90.14 fair value, while the SWS DCF model points to a future cash flow value of about US$179.97, implying the stock trades roughly 50% below that estimate. So which yardstick do you rely on more for your own work?

Next Steps

This mix of cautious and optimistic signals only goes so far. The real edge comes from reviewing the underlying data yourself and deciding how comfortable you are with the trade off between risk and reward, starting with the 4 key rewards

Looking for more investment ideas?

If Selective Insurance Group sits in the maybe pile for you, do not stop here, there are plenty of other stocks that could better match your goals.

- Target resilient cash generators that still look overlooked by screening for screener containing 20 high quality undiscovered gems.

- Prioritise durable balance sheets and steady fundamentals by checking the solid balance sheet and fundamentals stocks screener (46 results).

- Focus on stability and sleep better at night by reviewing companies in the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.