A Look At SM Energy (SM) Valuation After Debt Redemption, Asset Sales And Higher Shareholder Payouts

SM Energy Company SM | 0.00 |

Dividend affirmation and debt redemption draw fresh focus to SM Energy

SM Energy (SM) is back in the spotlight after confirming a quarterly dividend of $0.22 per share and fully redeeming its 6.75% senior notes due 2026, moves that reshape its cash returns and debt profile.

Recent events around debt repayment, asset divestitures and higher production guidance have unfolded against a strong backdrop. SM Energy’s latest share price is $33.96, and its 90 day share price return of 30.77% feeds into a 1 year total shareholder return of 46.61%. This suggests momentum has been building as investors reassess both growth prospects and balance sheet risk.

If you are looking beyond SM Energy and want to see how other companies tied to energy infrastructure are trading, this is a good moment to scan 33 power grid technology and infrastructure stocks

Put simply, SM Energy now combines a higher dividend, lower net debt and an intrinsic value estimate that sits well above the US$33.96 share price. This raises the question of whether this is a genuine mispricing or whether markets are already factoring in future growth.

Most Popular Narrative: 18% Overvalued

SM Energy’s most followed narrative pegs fair value at $28.82, below the latest $33.96 close. This creates a valuation gap investors will want to unpack.

The analysts have a consensus price target of $40.0 for SM Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $59.0, and the most bearish reporting a price target of just $27.0.

Curious what justifies a higher price target when the narrative fair value sits below today’s share price? Revenue assumptions, margin expectations and a re rated future earnings multiple sit at the core of this story. The exact mix of those inputs matters far more than any single headline number.

Result: Fair Value of $28.82 (OVERVALUED)

However, that higher price target still sits against real pressure points, including Uinta Basin logistics and the ongoing capital needed just to keep shale output from slipping.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: DCF Points the Other Way

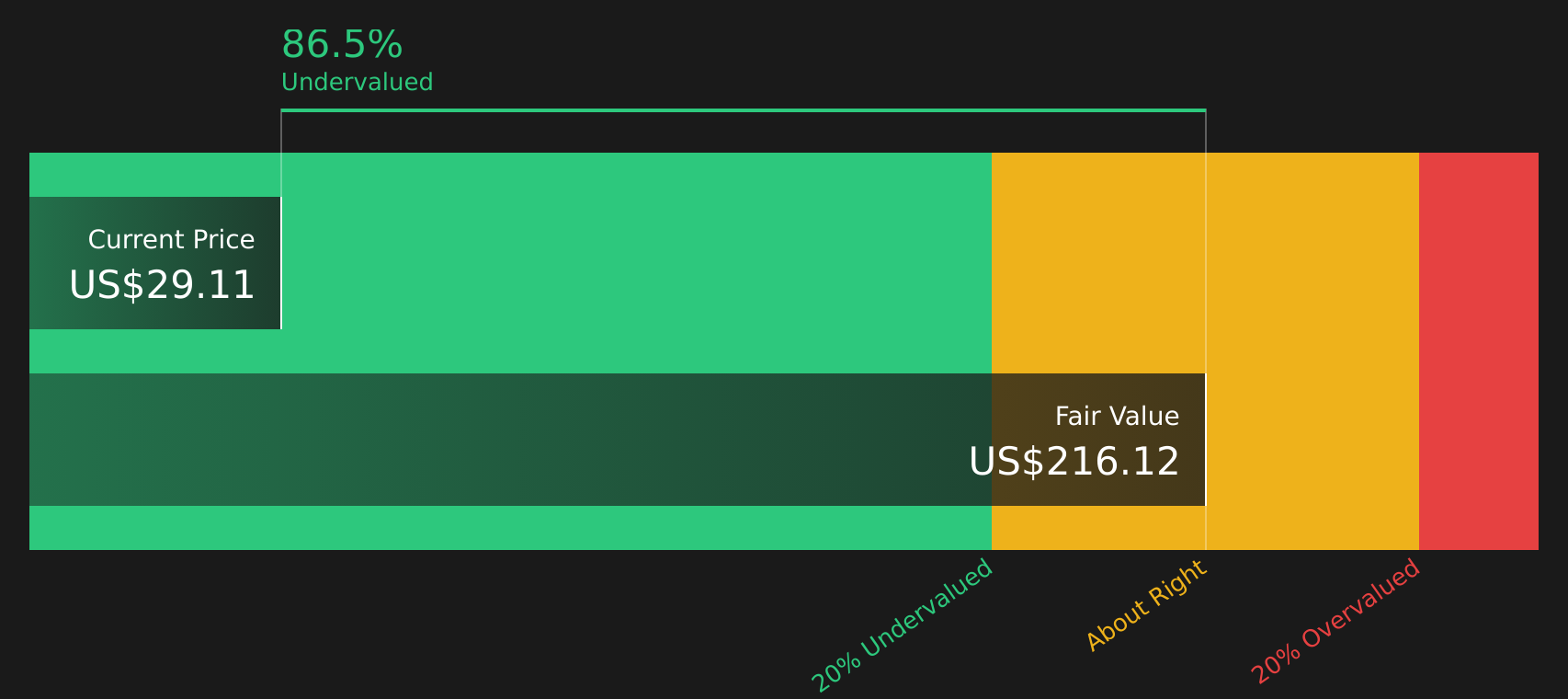

The popular narrative prices SM Energy at $28.82, which sits below the $33.96 share price and labels the stock as overvalued. Our DCF model, however, presents a different perspective, with a future cash flow value of $219.51 per share that indicates a very large gap in the opposite direction. When two methods disagree this sharply, it raises the question of which one you place more weight on and why.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SM Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The split in sentiment is clear. If you are weighing both the concerns and the potential upside, it helps to move quickly and test the data yourself with 3 key rewards and 5 important warning signs

Looking for more investment ideas?

Do not stop with a single stock when there are other opportunities that might fit your goals just as well or even better.

- Spot potential bargains before the crowd by scanning 47 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect them yet.

- Prioritize resilience and sleep easier at night by reviewing 65 resilient stocks with low risk scores that stand out for steadier risk profiles.

- Target income-focused ideas by checking 10 dividend fortresses offering higher yields that could support a regular cash return stream.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.