A Look At Stanley Black & Decker (SWK) Valuation After Recent Share Price Momentum

Stanley Black & Decker, Inc. SWK | 0.00 |

Recent performance snapshot

Stanley Black & Decker (SWK) has drawn fresh attention after recent share price moves, with the stock near US$79.42 and showing mixed returns over the past week, month, past 3 months, and year to date.

Set against a 1-year total shareholder return of 27.2%, the recent 3.9% 7-day share price return and 4.7% 1-month share price return suggest momentum has picked up again after a softer 90-day patch, even though the 5-year total shareholder return is still down 55.7%.

If this kind of rebound has you thinking about where else value or recovery stories might be forming, it could be a good moment to check out 20 top founder-led companies

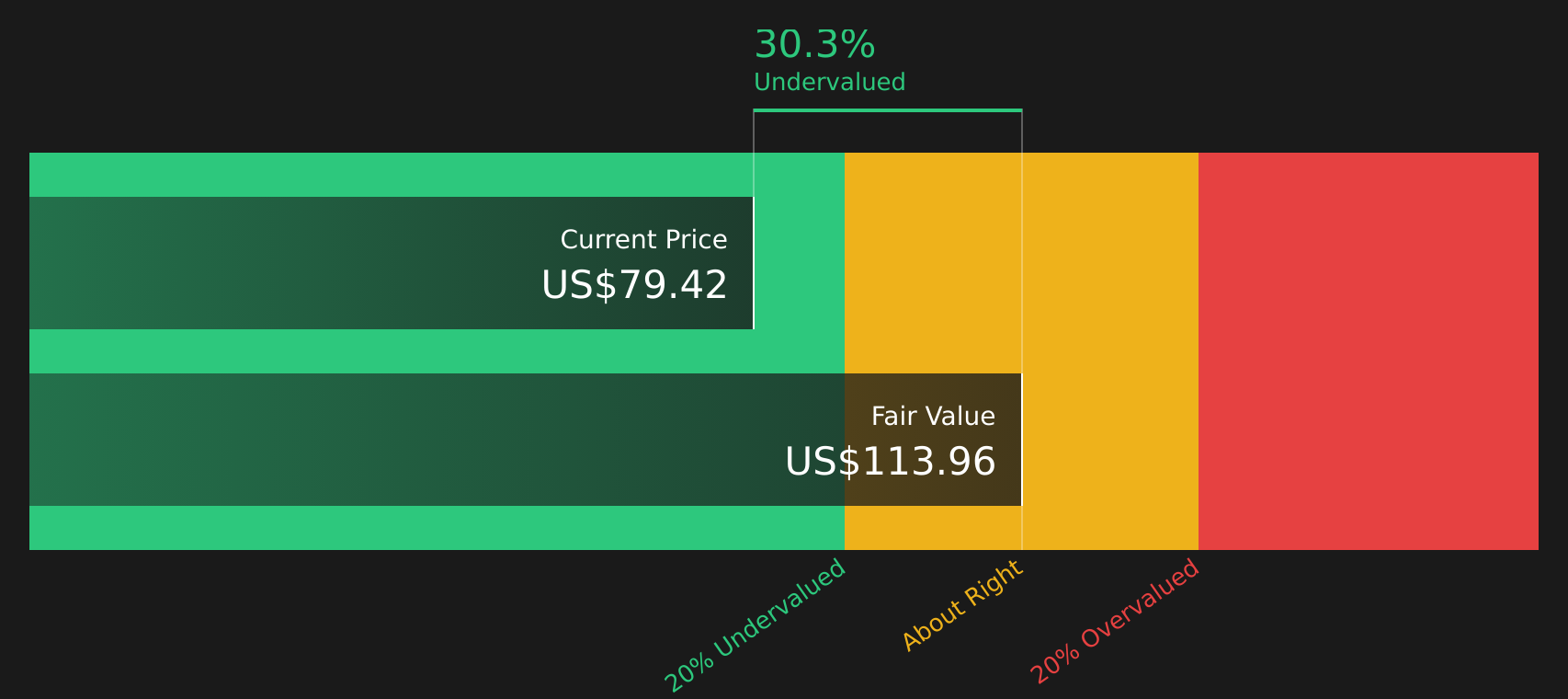

With Stanley Black & Decker trading around US$79.42 and sitting at a 30.1% estimated intrinsic discount, plus a 14% gap to the average analyst target, investors may ask whether this is a genuine value opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 11.6% Undervalued

Against the last close at $79.42, the most followed narrative points to a fair value of $89.87. This frames the current discount as primarily about execution on margins and steady but measured growth assumptions.

The multi-year supply chain transformation nearing its final phase is delivering substantial recurring cost reductions, improved operational flexibility, and resilience to trade/tariff shocks. Management expects these initiatives to drive gross margin back to 35%+ by late 2026, supporting sustained improvements in net margins and earnings.

Want to see what turns those margin ambitions into that fair value gap? The narrative leans heavily on earnings expansion, modest revenue growth and a future valuation multiple that does a lot of work.

Result: Fair Value of $89.87 (UNDERVALUED)

However, there are still pressure points, including softer DIY and Outdoor demand and heavy reliance on big-box retailers, that could quickly challenge this recovery story.

Another angle on valuation

The SWS DCF model paints a stronger picture, with an estimated future cash flow value of $113.66 per share versus the current $79.42 price. That points to a sizeable gap, but it hinges on those long term cash flow and margin assumptions actually playing out. How comfortable are you with those inputs?

Next Steps

This mix of risks and rewards raises a simple question: are you comfortable with the trade off at today’s price or not? To answer that for yourself, move quickly from headline numbers to the underlying drivers and weigh both sides of the story through 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might fit your goals even better, so keep widening your field of view.

- Target stronger value potential by scanning for companies trading below what fundamentals suggest through the 46 high quality undervalued stocks.

- Build a steadier income stream by checking out businesses that qualify as 10 dividend fortresses.

- Strengthen your defense by reviewing companies highlighted in the 62 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.