A Look At Ternium (NYSE:TX) Valuation As Profitability Jumps On Latest Earnings Report

Ternium S.A. Sponsored ADR TX | 0.00 |

Earnings jump puts Ternium (TX) in focus

Ternium (NYSE:TX) is on investors’ radar after reporting first quarter 2026 results, with sales of US$3,934 million and net income of US$213 million, compared with US$67 million a year earlier.

At a share price of US$44.11, Ternium’s 1 month share price return of 10.77% and year to date share price return of 12.73% sit alongside a 1 year total shareholder return of 64.06%. This suggests momentum has been building as profitability has improved.

If this earnings move has you looking beyond a single steel producer, it may be a good moment to scan for other materials and infrastructure plays using our 35 power grid technology and infrastructure stocks

On one hand, Ternium appears discounted on some intrinsic measures. However, the stock trades close to one analyst’s price target and has already delivered strong 1 year returns, so investors may question whether there is meaningful upside remaining or whether the market is already pricing in future growth.

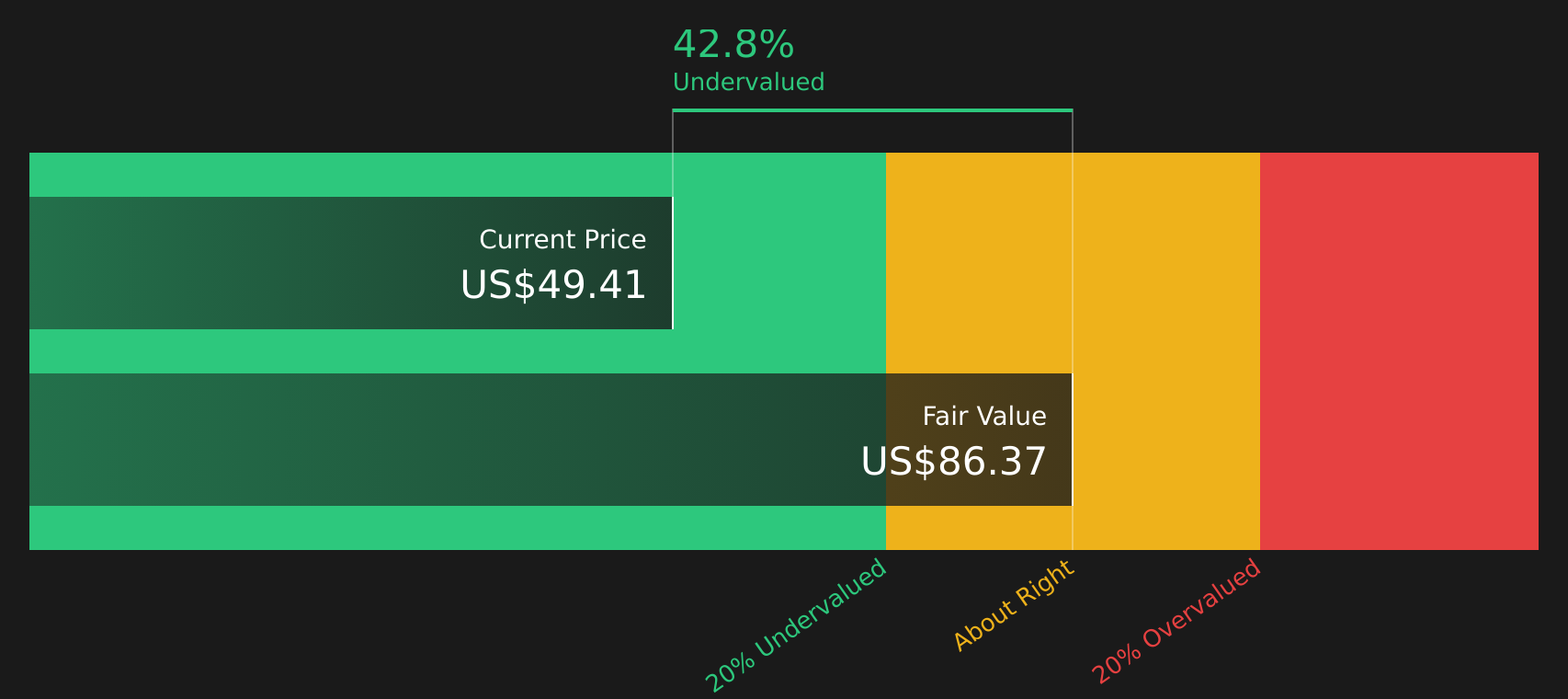

Most Popular Narrative: 1.5% Overvalued

With Ternium’s last close at $44.11 and the most followed narrative pointing to a fair value of $43.46 using an 8.91% discount rate, the gap between price and modelled value is very tight but still slightly on the expensive side.

Substantial ongoing investment in the Pesqueria Industrial Center in Mexico is set to increase capacity by 1.5 million tons annually, with new cold rolling and galvanized lines starting ramp-up from late 2025 onward. This is described as positioning Ternium to capitalize on potential long-term demand growth from nearshoring and infrastructure projects, supporting potential future top-line growth and operational leverage.

The fair value hinges on how much extra earnings this new capacity and product shift can support, and what kind of profit margin and earnings multiple the company can sustain once those projects are fully reflected in the financials.

Result: Fair Value of $43.46 (OVERVALUED)

However, there is still the risk that heavy capital spending strains free cash flow, or that sustained import pressure keeps pricing and margins under pressure.

Another Angle on Value

The narrative based on analyst targets suggests Ternium is slightly overvalued around $44.11 versus a fair value of $43.46. Yet our DCF model points the other way, with an estimated future cash flow value of $82.43, implying a wide gap investors cannot ignore. Which story do you trust more: price targets or cash flows?

Next Steps

With sentiment clearly mixed between upside potential and real risks, it makes sense to move quickly and test the assumptions against your own expectations using our 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Ternium has sharpened your focus, do not stop here. Use the tools available to quickly spot other opportunities and pressure test your portfolio.

- Target potential turnaround stories by scanning 22 elite penny stocks with strong financials with tighter financial filters than a broad market search.

- Hunt for quality at a reasonable price by checking companies in the 51 high quality undervalued stocks that pair fundamentals with appealing valuations.

- Prioritize resilience and balance sheet strength by reviewing the solid balance sheet and fundamentals stocks screener (46 results) so you are not caught off guard in tougher conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.