A Look At Tri Pointe Homes (TPH) Valuation After Strong Recent Returns And Full Pricing To Analyst Targets

Tri Pointe Homes, Inc. TPH | 0.00 |

What Tri Pointe Homes’ Recent Returns Tell You

Tri Pointe Homes (TPH) has drawn attention after a past 3 months total return of 32.4% and year to date return of 48.7%. These figures are prompting investors to reassess the stock’s recent momentum and underlying fundamentals.

Tri Pointe Homes’ recent share price return over 90 days of 32.4% and year to date share price return of 48.7%, alongside a 5 year total shareholder return of 93.37%, points to building momentum around the current US$46.95 share price as investors reassess growth prospects and risk.

If you are comparing Tri Pointe Homes with other opportunities in the market, this could be a good moment to broaden your search and check out the 19 top founder-led companies

With Tri Pointe Homes trading near its analyst price target at US$46.95 and carrying an intrinsic discount flag, the key question is whether the strong recent run leaves limited upside or if the market is still underpricing future growth.

Most Popular Narrative: 0% Undervalued

The most followed narrative pegs Tri Pointe Homes’ fair value at $47.00, almost identical to the last close of $46.95, and anchors that view in detailed forecasts and deal terms.

Analysts are assuming Tri Pointe Homes's revenue will decrease by 2.3% annually over the next 3 years. Analysts assume that profit margins will shrink from 6.9% today to 5.9% in 3 years time.

Want to see what justifies a fair value right on top of the agreed cash offer? The narrative links shrinking earnings, lower margins and a richer future earnings multiple into one tight valuation story.

Result: Fair Value of $47 (ABOUT RIGHT)

However, there are still red flags, such as a 25% home order decline and exposure to softer Western markets, which could pressure margins and challenge this fair value story.

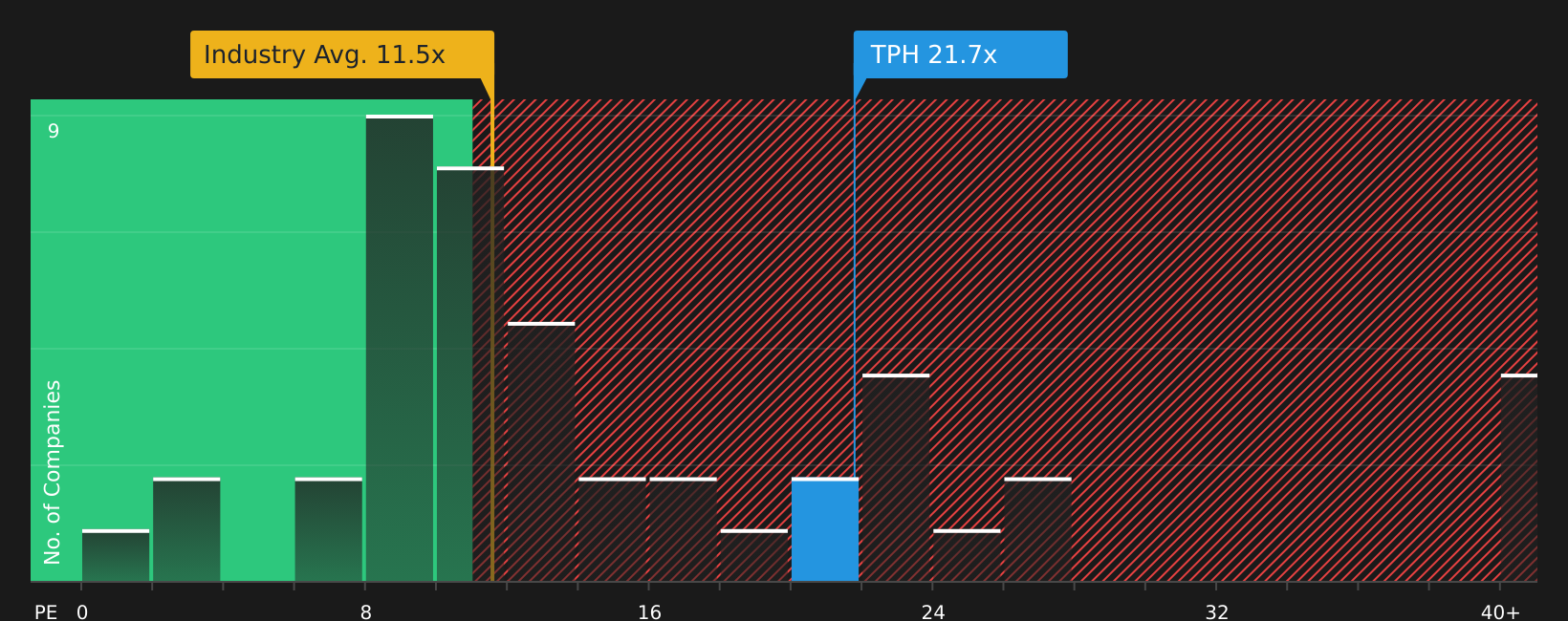

Another Way To Look At Valuation

So far the focus has been on fair value around $47, but the current P/E of 21.7x stands out against a Consumer Durables industry average of 12.4x and a peer average of 14.8x, as well as a fair ratio of 16x that the market could move toward.

If the P/E did move closer to that 16x fair ratio, a larger portion of today’s price would be tied to deal completion and sentiment rather than long-term earnings power. This raises a simple question: how much multiple risk are you really comfortable owning here?

Next Steps

If this combination of momentum and valuation questions leaves you unsure, do not wait for a clearer headline before examining the finer print yourself and reviewing the 3 important warning signs

Ready To Act On Your Next Idea?

If you only focus on Tri Pointe Homes, you could overlook other strong opportunities, so use this moment to widen your search with targeted stock ideas.

- Target potential mispricings by scanning companies that combine quality fundamentals with attractive valuations using the 51 high quality undervalued stocks.

- Prioritize resilience by focusing on businesses with strong finances through the solid balance sheet and fundamentals stocks screener (44 results).

- Hunt for underfollowed opportunities by checking the screener containing 23 high quality undiscovered gems before others catch on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.