A Look At TriMas (TRS) Valuation After Recent Share Price Momentum

TriMas Corporation TRS | 0.00 |

TriMas stock snapshot and recent performance

TriMas (TRS) has been drawing attention after recent share price moves, with the stock last closing at $39.21. Investors are weighing this level against its recent returns and the company’s current fundamentals.

Recent moves have added to an already strong run, with an 8.05% year to date share price return and a 53.54% total shareholder return over the past year suggesting momentum has been building rather than fading.

If TriMas has caught your attention and you want to see what else is moving, this is a good moment to broaden your search with 20 top founder-led companies

With TriMas trading at $39.21 and indications of both an intrinsic value gap and a discount to analyst targets, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 5.5% Undervalued

TriMas' widely followed narrative pegs fair value at $41.50, slightly above the last close of $39.21, which frames the stock as modestly undervalued on that view.

New leadership with significant packaging industry expertise is implementing operational standardization and integration across global manufacturing sites and recent acquisitions. This push is expected to drive margin expansion and improved operating leverage, positively impacting net margins and earnings potential.

Want to see what sits behind that confidence in higher margins and earnings power? The narrative leans heavily on faster profit growth than revenue and a richer profitability profile built over several years.

Result: Fair Value of $41.50 (UNDERVALUED)

However, there are still clear risks, particularly if packaging integration drags on or if sustainability rules and material shifts weigh on demand for parts of the product range.

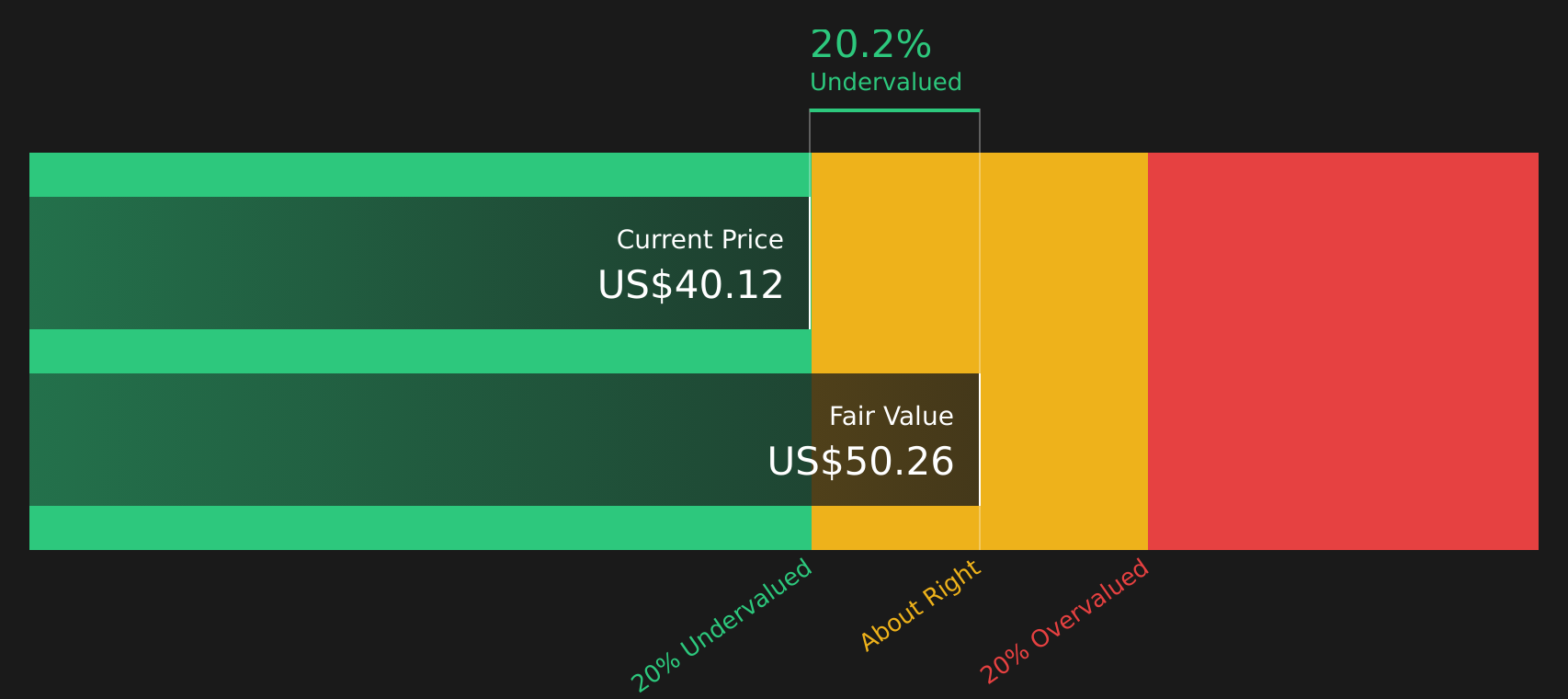

Another way to look at TriMas' valuation

The DCF view presents TriMas as attractive, with the stock at $39.21 compared to an estimated future cash flow value of $50.26, or about a 22% gap. That appears to be a decent cushion on paper, but it also raises a question: how comfortable are you with the cash flow assumptions underlying this estimate?

Next Steps

Mixed messages so far, right, with both risks and rewards in play. To move quickly from headline views to your own conclusion, spend a few minutes reviewing the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If TriMas looks interesting, do not stop here. Use focused stock lists to quickly surface other opportunities that could fit your goals and risk appetite.

- Spot potential mispriced opportunities early by scanning 51 high quality undervalued stocks that combine quality fundamentals with attractive entry points.

- Strengthen the income side of your portfolio by reviewing 10 dividend fortresses built around higher-yield payouts.

- Prioritise resilience by checking 67 resilient stocks with low risk scores that score well on balance sheet strength and risk metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.