A Look At Ultra Clean Holdings (UCTT) Valuation After Strong AI Infrastructure Demand And Improved Growth Outlook

Ultra Clean Holdings, Inc. UCTT | 0.00 |

Ultra Clean Holdings (UCTT) drew fresh attention after reports of rising demand for its subsystems tied to leading edge foundry logic, high bandwidth memory, and advanced packaging that support AI centered semiconductor workloads.

Those AI related orders helped the stock surge earlier in the year, and even after a 12.4% share price pullback in the last session and a softer 7 day patch, Ultra Clean still sits on a 90 day share price return of 62.3% and a very large 1 year total shareholder return of 296.1%. This points to strong momentum that has recently cooled at the margin.

If this AI hardware wave has your attention, it could be a good moment to scan a broader set of enablers through Simply Wall St’s screener for 48 AI infrastructure stocks

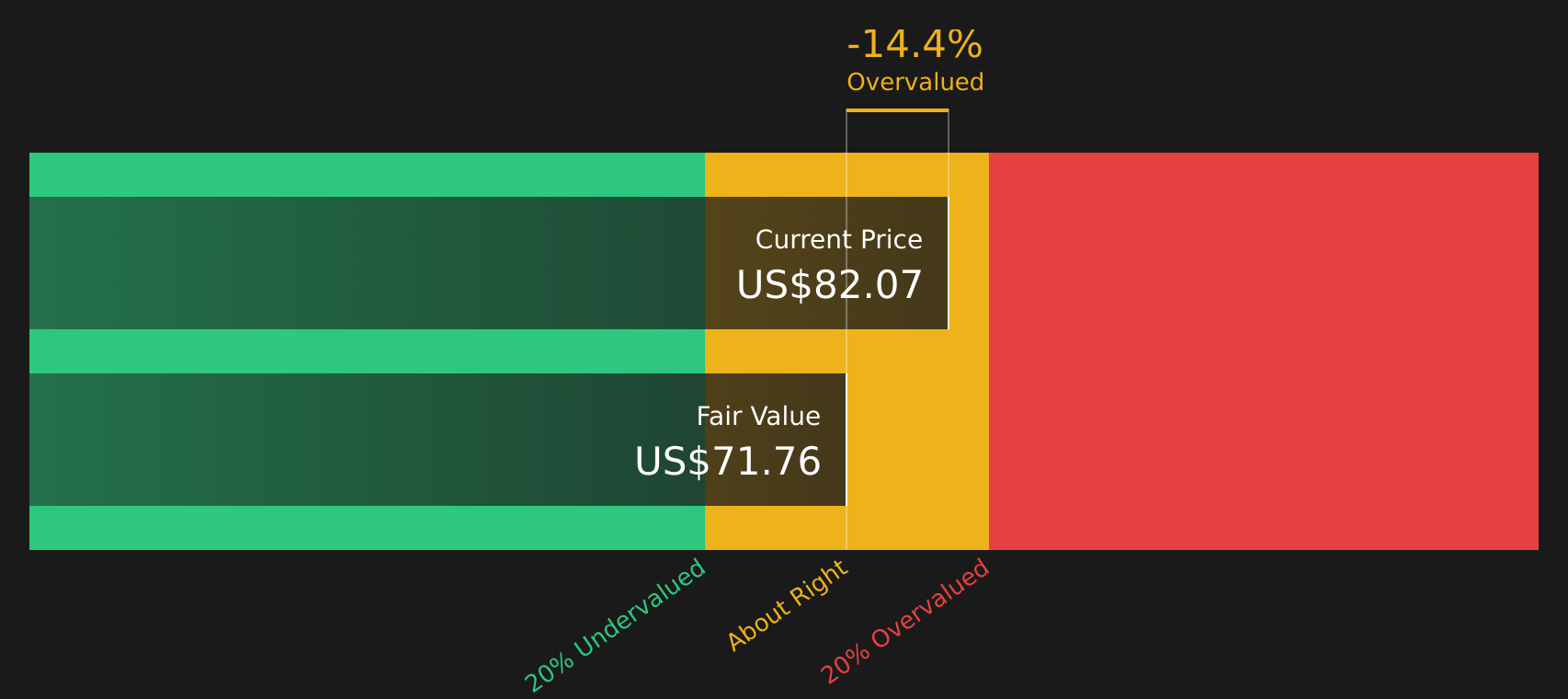

With Ultra Clean now trading at $82.07 after a sharp run and a recent pullback, the key question is whether current enthusiasm around AI subsystems leaves upside on the table or if the stock already reflects years of future growth.

Most Popular Narrative: 1% Overvalued

At $82.07, Ultra Clean is trading slightly above the most followed fair value estimate of $81.25, which is built on detailed long range forecasts and a specific discount rate.

A surge in AI-driven capital investment and strong expectations for new fab buildouts in 2026 support solid long-term demand for Ultra Clean's advanced process subsystems, reinforcing the company's exposure to the ongoing expansion of digital infrastructure and complex chip manufacturing (supports long-term revenue trajectory).

Want to see what is backing that small valuation gap? Revenue compounding, margin repair and a future earnings multiple that leans heavily on the AI equipment buildout.

Result: Fair Value of $81.25 (OVERVALUED)

However, the story can change quickly if key customers cut orders, or if prolonged industry softness keeps Ultra Clean running well below its scaled capacity and limits operating leverage.

Another Angle on Valuation

While the most followed fair value sits just below the current $82.07 share price, the SWS DCF model indicates Ultra Clean is trading above an estimated future cash flow value of $72.83, which points to an overvalued signal. The question for you is which framework better fits how you think about risk around AI driven cycles and cyclic equipment spending.

Next Steps

Given the mix of excitement and caution running through this story, it makes sense to look at the underlying data yourself and move quickly to form your own view based on the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Ultra Clean has caught your eye, do not stop here. Put the same energy into finding other opportunities that fit your style and risk comfort.

- Target value focused opportunities by scanning 49 high quality undervalued stocks that combine quality fundamentals with price points some investors may be overlooking.

- Prioritise resilience by checking 64 resilient stocks with low risk scores if you want stocks with steadier risk profiles at the core of your portfolio.

- Spot potential future standouts early by reviewing the screener containing 22 high quality undiscovered gems before everyone else starts talking about them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.