A Look At Ultra Clean Holdings (UCTT) Valuation As AI Infrastructure Demand And Analyst Upgrades Draw Interest

Ultra Clean Holdings, Inc. UCTT | 0.00 |

Ultra Clean Holdings (UCTT) is back on investors’ radar after being lifted to a top Zacks Rank, with analysts raising earnings estimates in response to AI infrastructure demand and upgrades in wafer fab equipment spending.

The stock’s momentum has been strong, with a 93.44% 90 day share price return and a 204.32% year to date share price return, contributing to a 332.35% 1 year total shareholder return as AI infrastructure interest and earnings revisions gain attention.

If you want to see how other chip related stocks are reacting to AI infrastructure demand, it is a good time to scan the market using the 39 AI infrastructure stocks

With Ultra Clean up sharply this year, trading at US$83.14 and sitting roughly 26% below the average analyst price target of US$104.40 while still reporting a net loss, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 2.3% Overvalued

Ultra Clean Holdings closed at $83.14, a touch above the most followed fair value estimate of $81.25, which is built on detailed long term forecasts and a specific 11.27% discount rate.

Analysts are assuming Ultra Clean Holdings's revenue will grow by 12.5% annually over the next 3 years. In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 125.3x on those 2029 earnings, up from -19.9x today. This future PE is greater than the current PE for the US Semiconductor industry at 47.2x.

Revenue rising at a steady clip. Margins turning from loss making to positive. And a future earnings multiple that assumes a premium story. It may be worth examining which specific growth and profitability assumptions are doing the heavy lifting behind that fair value.

Result: Fair Value of $81.25 (OVERVALUED)

However, there are still clear warning flags, including reliance on a handful of large customers and ongoing tariff and supply chain pressures that could affect margins and growth assumptions.

Another View: Sales Ratios Tell a Different Story

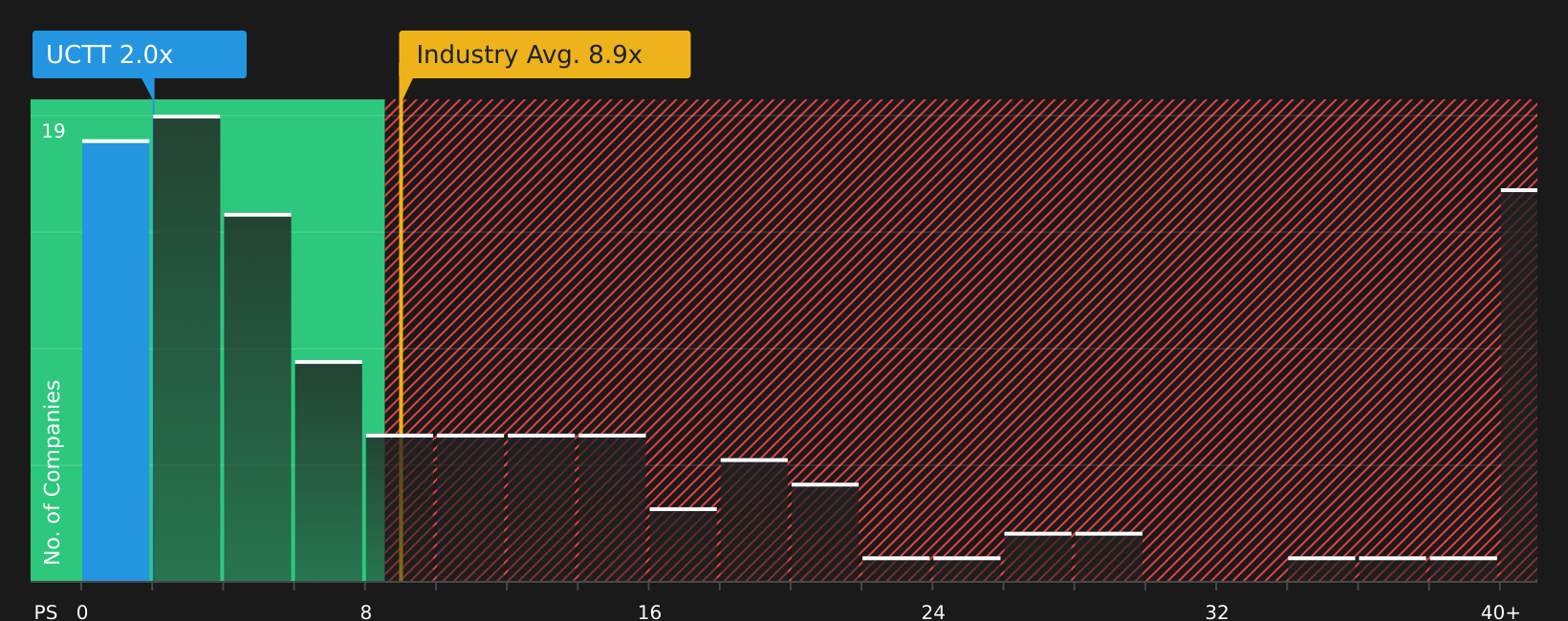

While the fair value model suggests Ultra Clean Holdings is slightly overvalued, the current P/S of 1.8x looks low compared with the US Semiconductor industry at 8.1x and the 2.7x fair ratio. That gap points to meaningful upside risk or downside protection, depending on which framework you trust more.

To see how this pricing gap lines up with earnings quality, profit expectations and peer comparisons, take a closer look at the valuation breakdown, including where the fair ratio suggests the market could move over time, in the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With that mix of optimism and caution in mind, act quickly to review the numbers yourself, weigh both sides, and see the full picture in the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop here, you only see one part of the opportunity set. Use the screeners below to quickly spot other stocks that could deserve a place on your radar.

- Target quality at a discount by scanning for companies that combine strong fundamentals with attractive pricing using the screener containing 24 high quality undiscovered gems.

- Prioritise resilience first and sort for companies with steadier profiles and lower overall risk characteristics through the 74 resilient stocks with low risk scores.

- Zero in on financial strength by filtering for companies with robust balance sheets and solid fundamentals using the solid balance sheet and fundamentals stocks screener (46 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.