A Look At Valero Energy (VLO) Valuation After Strong Fourth Quarter Earnings Performance

Valero Energy Corporation VLO | 244.09 | +1.09% |

Valero Energy (VLO) is back in the spotlight after fourth quarter 2025 results showed net income of US$1,134 million on sales of US$30,372 million, with earnings per share rising sharply year over year.

Investors have reacted strongly to the latest earnings, with the share price at US$202.68 after a 4.40% 1 day share price return and a 22.61% year to date share price return. The 1 year total shareholder return of 56.78% points to momentum that has been building rather than fading.

If Valero’s recent move has you looking across the energy space, it might be a good moment to scan other power related names with our 23 power grid technology and infrastructure stocks.

With earnings per share jumping to US$3.73 in the quarter and the stock near US$203 after a 1 year total return above 50%, the key question is whether Valero still trades below its intrinsic value or if the market is already pricing in future growth.

Most Popular Narrative: 9.3% Overvalued

Valero’s most followed narrative, according to StickmanCyborg, sets a fair value of $185.51 per share, below the last close at $202.68, which creates a clear valuation gap for investors to weigh.

In this regard, outstanding is VLO, with excellent free cash flow per share of $18.34 and a dividend coverage ratio of 2.65%, the highest among peers. Even though its profit margins are lower compared to the previous year at 2.9% versus 7.4%, respectively, VLO's valuation is 71.8% below its fair value, and its dividend yield is attractive at 3.49%.

Curious how a company with moderating margins still lands at that fair value? The narrative leans heavily on expectations for future profitability, steadier cash generation, and a valuation multiple that assumes those trends take hold. Want the full picture behind those assumptions? Read the story that connects these moving parts.

Result: Fair Value of $185.51 (OVERVALUED)

However, if refining margins weaken further or cash generation falls short of expectations, that $185.51 fair value and the 42.07% intrinsic discount could be challenged.

Another View: Cash Flows Tell a Different Story

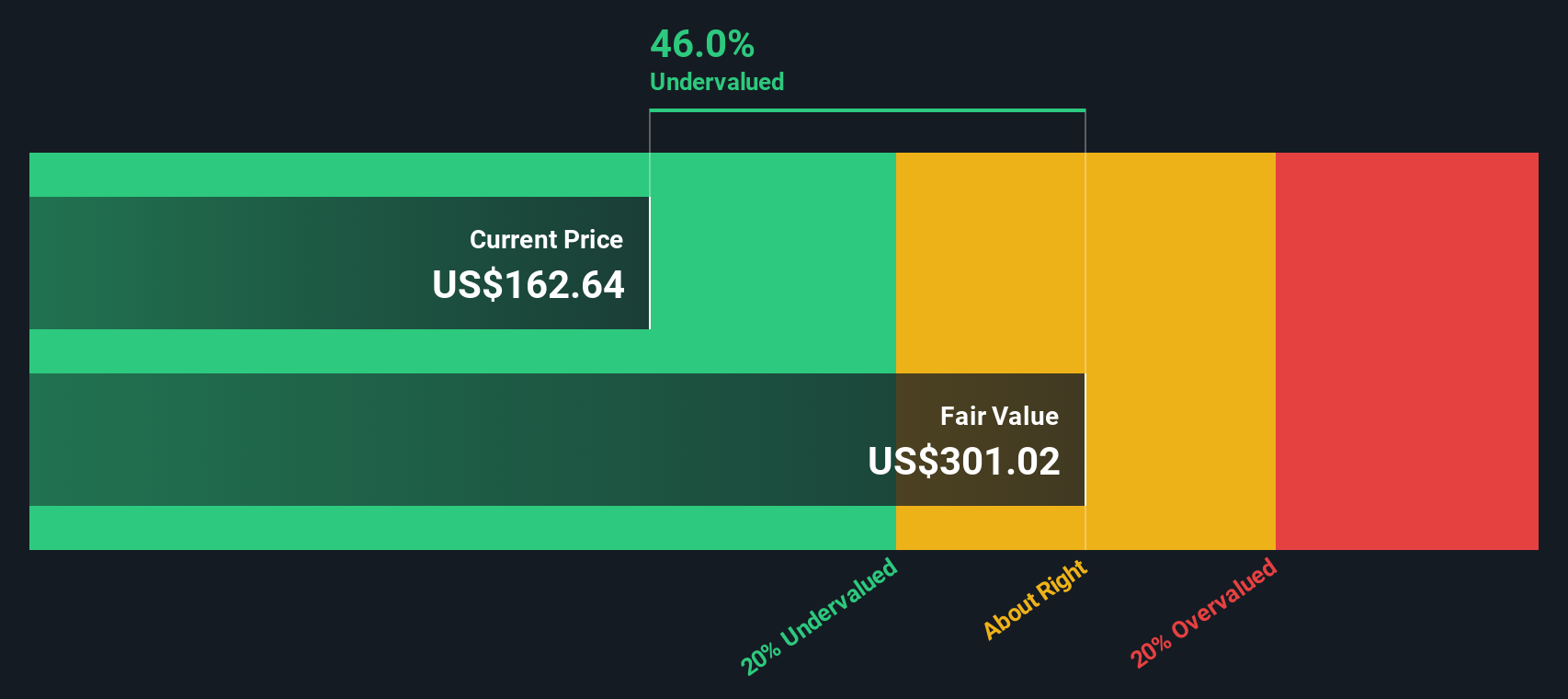

While the user narrative flags Valero as 9.3% overvalued at $202.68 versus a $185.51 fair value, our DCF model points the other way. On this framework, Valero at $194.14 is trading well below an estimated future cash flow value of $349.88, which frames the current price as cheap relative to its projected cash generation.

These two models send very different signals. Which one feels closer to how you think about risk around refining margins and future earnings quality?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Valero Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Valero Energy Narrative

If you look at the numbers and reach a different conclusion, or prefer to test your own assumptions, you can build and publish a full narrative in just a few minutes. To get started, use Do it your way.

A great starting point for your Valero Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities that fit your style better, so use the screener to line up your next candidates.

- Target value first and see which companies stand out as 53 high quality undervalued stocks based on their fundamentals.

- Focus on strength and filter for companies in our solid balance sheet and fundamentals stocks screener (45 results) that prioritise financial resilience.

- Build a watchlist of future contenders using our screener containing 25 high quality undiscovered gems that may not be widely followed yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.