A Look At Ventas (VTR) Valuation After Raised 2026 Guidance And First Quarter Earnings

Ventas, Inc. VTR | 0.00 |

Guidance raise and first quarter earnings put Ventas in focus

Ventas (VTR) raised its full year 2026 earnings guidance and reported first quarter results, highlighting higher property performance in its senior housing portfolio and contributions from recent investment activity.

After the guidance raise and first quarter results, Ventas’s recent share price moves tell a story of steady interest, with a 30 day share price return of 3.5%, year to date share price return of 11.9%, and a 1 year total shareholder return of 35.6%, suggesting that momentum has been building over a longer stretch.

If you are thinking beyond healthcare real estate and want to see what else has been attracting attention, this is a good moment to check out 36 power grid technology and infrastructure stocks

With guidance now higher, revenue at US$1,656.94 million in the quarter, and the stock already up 35.6% over 1 year, investors may question whether Ventas is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 7% Undervalued

Ventas last closed at $86.55, compared with a widely followed fair value estimate of $93.10 that uses a 7.48% discount rate and detailed long term cash flow assumptions.

Ongoing active portfolio management, such as converting underperforming triple net assets to SHOP, acquisitions focused on high performing newer assets in strong demographic markets, and expanding relationships with best in class operators, creates a runway for outsized top line revenue and FFO per share growth.

Want to see what is driving that growth runway? The narrative focuses on faster earnings, rising margins, and a rich future profit multiple. The full story sits in the detailed forecasts.

Result: Fair Value of $93.10 (UNDERVALUED)

However, you still need to weigh risks, such as operator underperformance in senior housing and pressure on margins if acquisition returns or labor costs do not line up with expectations.

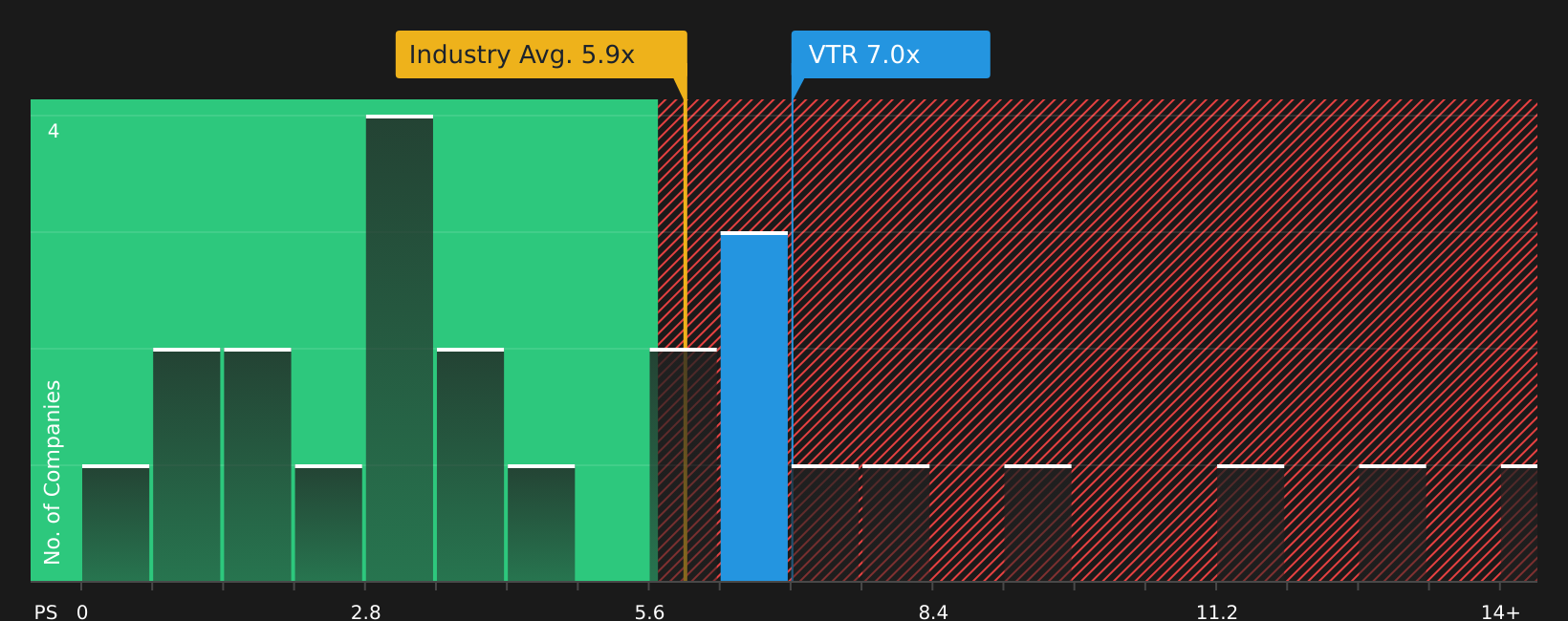

Another Angle on Valuation

The fair value of $93.10 suggests Ventas is 7% undervalued, but the P/S ratio paints a tighter picture. Ventas trades on 6.9x sales, above the North American Health Care REITs industry at 5.8x and above its own fair ratio of 5.8x, so the margin for error may be thinner than it looks.

For anyone weighing what that gap could mean for future entry points or position sizing, it is worth seeing how the numbers stack up in a fuller breakdown: See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed signals in the story so far? Use this as a prompt to move quickly, review the data first hand, and weigh both sides through 3 key rewards and 4 important warning signs

Looking for more investment ideas?

If Ventas has your attention, do not stop here. Widen your watchlist with other stocks that could fit your goals using targeted screeners.

- Zero in on potential mispricings by checking companies that look cheap on quality metrics through the 51 high quality undervalued stocks.

- Build a steadier income stream by reviewing stocks that feature the 12 dividend fortresses.

- Sleep easier at night by focusing on companies flagged in the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.