A Look At Virtu Financial (VIRT) Valuation After Earnings Beat And Strong Trading Technology Revenues

Virtu Financial VIRT | 0.00 |

Why Virtu Financial (VIRT) Is Back On Investors’ Radar

Virtu Financial (VIRT) is drawing attention after adjusted earnings per share beat expectations by 34.9%. Commissions and technology services revenue also reflected higher trading activity and firm performance across Market Making and Execution Services.

The 1 day share price return of 2.79% and 30 day share price return of 7.13% put Virtu Financial at US$51.55, while a 90 day share price return of 23.80% sits alongside a 3 year total shareholder return of 217.51%, hinting that momentum has been building over time.

If you like how Virtu is tied to trading technology, it could be worth scanning the market for other opportunities using the Simply Wall St screener for 47 AI infrastructure stocks.

With Virtu trading close to analyst price targets yet showing a large implied intrinsic discount, the key question is whether the stock still trades below its underlying worth or whether the market already prices in future growth.

Most Popular Narrative: 5.5% Overvalued

Compared with Virtu Financial’s last close at $51.55, the most followed narrative sets fair value at $48.86, using a detailed discounted cash flow framework.

Virtu's investments in trading technology, cross-asset platform integration, and digital asset capabilities (including crypto, stablecoins, and tokenized assets) position it to capture new wallet share, providing earnings growth and improved revenue diversification.

Want to know what has to happen for that valuation to hold up? The narrative leans heavily on fatter profit margins and a very specific earnings path. Curious how far revenue can contract while earnings still rise and the P/E multiple drifts lower, yet the model still calls the stock close to fairly priced? The full breakdown joins those moving parts into one tight set of assumptions.

Result: Fair Value of $48.86 (OVERVALUED)

However, investors also need to weigh risks, including rising tech driven competition and potential regulatory shifts around digital assets that could affect Virtu’s margins and growth assumptions.

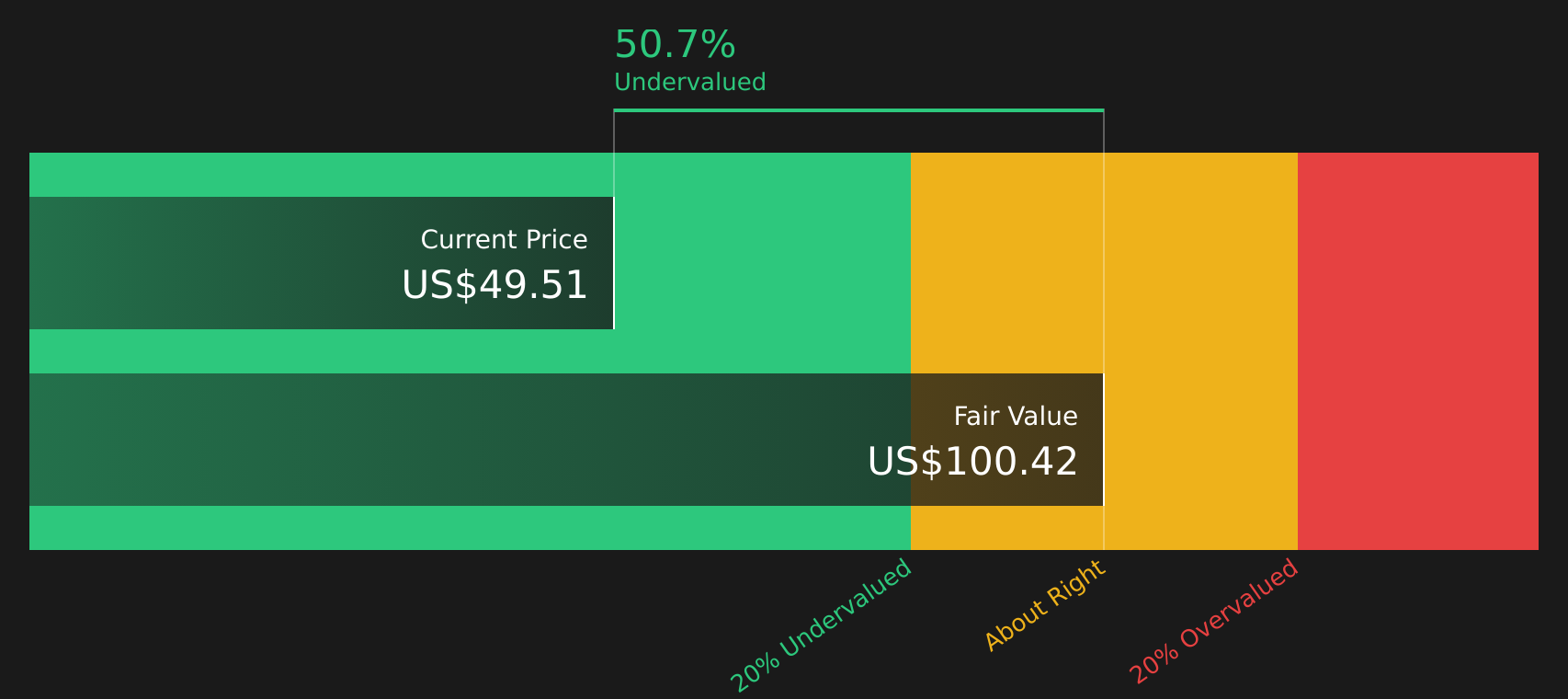

Another Take On Value

The DCF based narrative suggests Virtu looks about 5.5% overvalued at $48.86, while our DCF model points to a future cash flow value closer to $100.38. This implies the stock trades well below that estimate. When two cash flow views disagree this sharply, which set of assumptions would you trust more?

Next Steps

Sensing mixed signals from the story so far, with both risks and rewards in play, it makes sense to move quickly and weigh the full picture using 5 key rewards and 1 important warning sign.

Ready to hunt for your next idea?

If Virtu has sharpened your focus, do not stop here. Use the screeners below to quickly narrow the market to a few focused, actionable ideas.

- Target stocks that combine quality with a valuation gap by running a search through the 47 high quality undervalued stocks.

- Prioritise resilience by filtering for companies with strong finances using the solid balance sheet and fundamentals stocks screener (45 results).

- Aim for potential income and price appreciation together by scanning the market with the 10 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.