A Look At Virtu Financial (VIRT) Valuation As EU MiCA License Expands Crypto Service Reach

Virtu Financial VIRT | 0.00 |

MiCA license puts Virtu’s EU crypto capabilities in focus

Virtu Financial (VIRT) is back on investor radars after its Irish subsidiary secured a Markets in Crypto Assets license, clearing the way for regulated digital asset services across all 27 EU member states.

The MiCA approval lands at a time when momentum in Virtu’s stock has been building, with a 1-day share price return of 1.81% and a 90-day share price return of 40.03%. The 3-year total shareholder return of 234.32% and 5-year total shareholder return of 130.54% indicate that the long term has also been rewarding.

If this crypto move has your attention, it could be a good moment to broaden your watchlist and check out 20 cryptocurrency and blockchain stocks

With the stock up strongly over the past year and trading at a premium to its analyst price target, the key question is whether Virtu is still undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 7.4% Overvalued

The most followed Virtu Financial narrative puts fair value at $51.71, below the last close of $55.55, and ties that gap to a specific earnings path.

Expanded retail trading activity, particularly through digital brokers and increased engagement in both U.S. and international markets, including overnight sessions, is driving higher trading volumes, directly boosting Virtu's core revenue and expanding its addressable opportunity set.

Rising volatility in the markets, fueled by ongoing geopolitical and macroeconomic shifts, continues to widen trading spreads and increase client activity, which supports higher trading revenues and net margins for Virtu.

Curious how a falling revenue line, fatter margins, and a lower future P/E are all stitched together into that fair value story? The earnings trajectory, revenue reset, and profitability assumptions sit at the heart of this narrative, and the balance between them is tighter than it looks at first glance.

Result: Fair Value of $51.71 (OVERVALUED)

However, there are still pressure points, including higher technology spend and tougher competition, that could squeeze margins and challenge the earnings path that supports that fair value view.

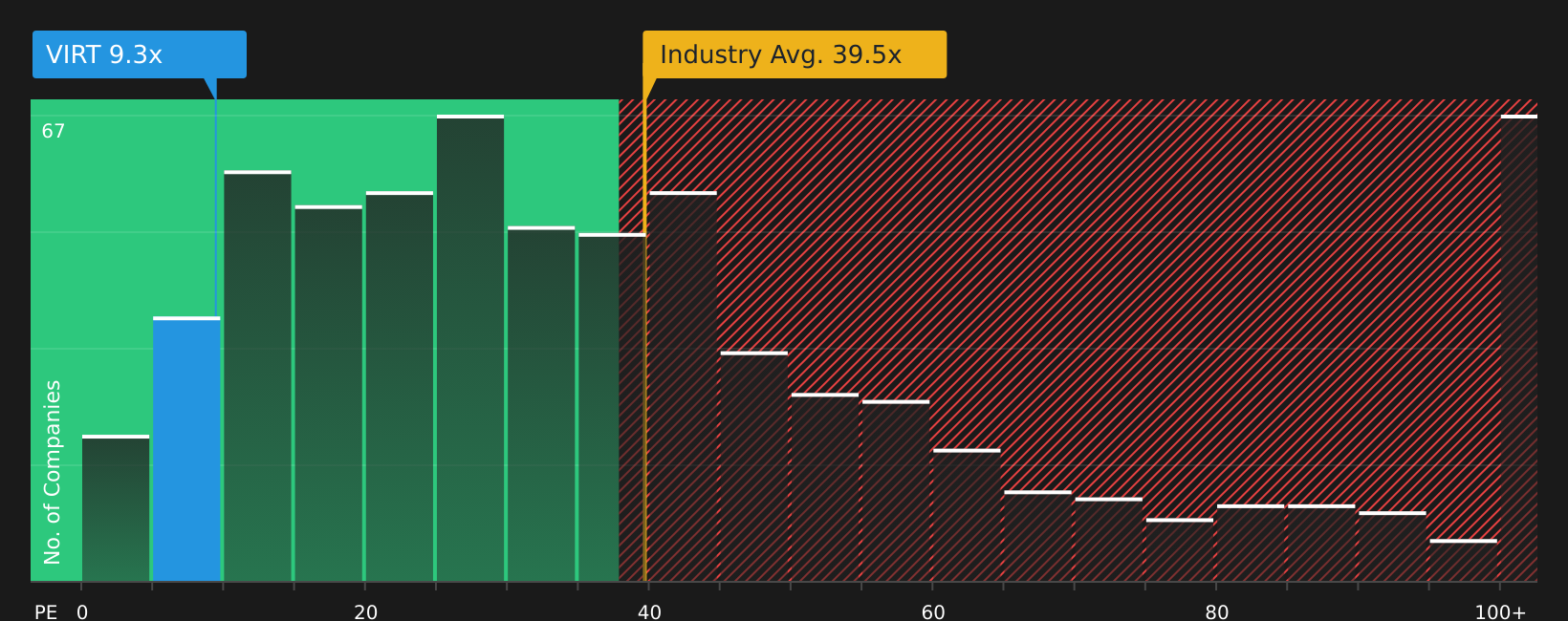

Another View: Multiples Point To A Different Story

While the narrative points to Virtu as 7.4% overvalued versus a $51.71 fair value, the current P/E of 9.4x tells a very different story. It sits far below the peer average of 26.7x and below a fair ratio of 15.2x, which suggests the market could be pricing in a lot of valuation risk already.

If you want to stress test how this P/E gap might close or widen over time, it is worth looking at the full valuation breakdown and how the earnings profile compares with peers, not just the headline multiples, before deciding what matters more for you: the narrative or the numbers in front of you.

Next Steps

With sentiment split between crypto upside and valuation questions, this is the moment to move quickly, check the data for yourself, and weigh up the 5 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Virtu has sharpened your focus, do not stop here. Use the Simply Wall Street Screener to uncover more stocks that fit your style and goals.

- Target potential value opportunities by scanning companies that combine earnings power with attractive pricing through the 48 high quality undervalued stocks.

- Strengthen your watchlist with businesses that carry less balance sheet stress by filtering candidates via the 63 resilient stocks with low risk scores.

- Spot underfollowed opportunities by sorting stocks with solid fundamentals using the screener containing 20 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.