A Look At W. P. Carey (WPC) Valuation As Steady Returns Draw Fresh Investor Attention

W. P. Carey Inc. WPC | 0.00 |

Recent performance snapshot and why W. P. Carey is on investor radars

With no single headline event driving attention, W. P. Carey (WPC) is back on watchlists as investors reassess its recent share performance, income profile, and valuation signals in the current real estate backdrop.

At a share price of US$74.35, W. P. Carey has seen short term share price softness over the past week but a stronger year to date share price return of 14.63%, which sits alongside a 1 year total shareholder return of 25.11% and 5 year total shareholder return of 29.46%. This suggests momentum has been gradually building around both income and price appreciation.

If this kind of steady real estate performance has your attention, it may be worth broadening your watchlist to see which other income oriented stocks are holding up in today’s market using the Simply Wall St screener for 20 top founder-led companies

So with W. P. Carey trading at US$74.35 and an indicated intrinsic value gap plus only a small discount to the US$76.75 analyst target, is the stock genuinely undervalued or already pricing in future growth?

Most Popular Narrative: 60% Undervalued

At a last close of $74.35 against a narrative fair value of $74.83, the widely followed model points to a large intrinsic value gap built on specific growth, margin and discount rate assumptions.

Significant lease structures feature inflation-linked escalators (CPI-based) and higher fixed annual bumps (around 2.8% on recent deals), enabling robust same-store rent growth even in a stable inflation environment, which directly enhances rental revenues and overall earnings.

Curious what kind of revenue build, margin profile and future earnings multiple are baked into that fair value call. The full narrative lays out a detailed path from rent escalators and international funding costs through to earnings and the discount rate that underpins the model.

Result: Fair Value of $74.83 (UNDERVALUED)

However, this depends on continued tenant health and asset sales; weaker credit outcomes or a slower disposition market could quickly challenge that undervaluation story.

Another way to look at value

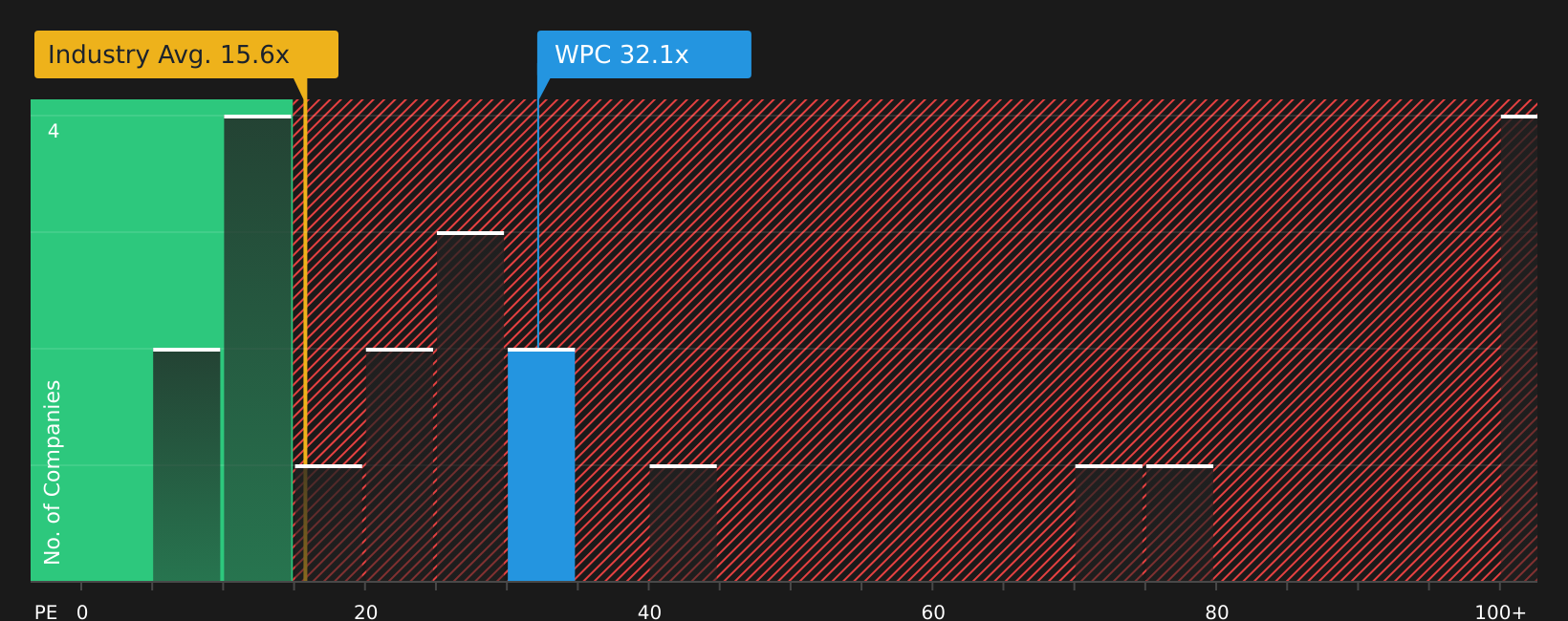

That big intrinsic value gap comes from a cash flow model, but the market is telling a different story through the P/E ratio. W. P. Carey trades on 32x earnings, roughly double the Global REITs average of 15.6x and below a fair ratio estimate of 36.7x. That mix of premium vs peers but discount vs fair ratio raises a key question: is the stock priced for comfort or for upside?

Next Steps

Seen enough to sense both optimism and caution around W. P. Carey? If you want to move quickly and build your own view of the balance between risks and potential rewards, start by weighing the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If W. P. Carey has sharpened your focus, do not stop here, the wider market is full of income, value and resilience ideas worth your attention.

- Spot potential bargains early by scanning companies that screen as high quality and priced below their estimated value using the 47 high quality undervalued stocks.

- Strengthen your income stream by researching stocks that feature in the 9 dividend fortresses and see which yields align with your risk comfort.

- Sleep easier at night by reviewing companies highlighted in the 64 resilient stocks with low risk scores, where balance sheets and risk scores help support long term confidence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.