A Look At Waters (WAT) Valuation After Recent Share Price Volatility

Waters Corporation WAT | 0.00 |

Waters (WAT) is back on investors’ radar after recent share price swings, with the stock down about 11.8% over the past year but slightly higher over the past month.

The recent 7 day share price return of a 10.67% decline and 1 day drop of 3.25% sit against a 90 day share price return of a 23.15% decline and a 1 year total shareholder return of an 11.8% loss. This suggests momentum has been fading after a brief rebound.

If Waters's recent volatility has you comparing opportunities, this could be a good moment to widen your watchlist and check out 32 healthcare AI stocks.

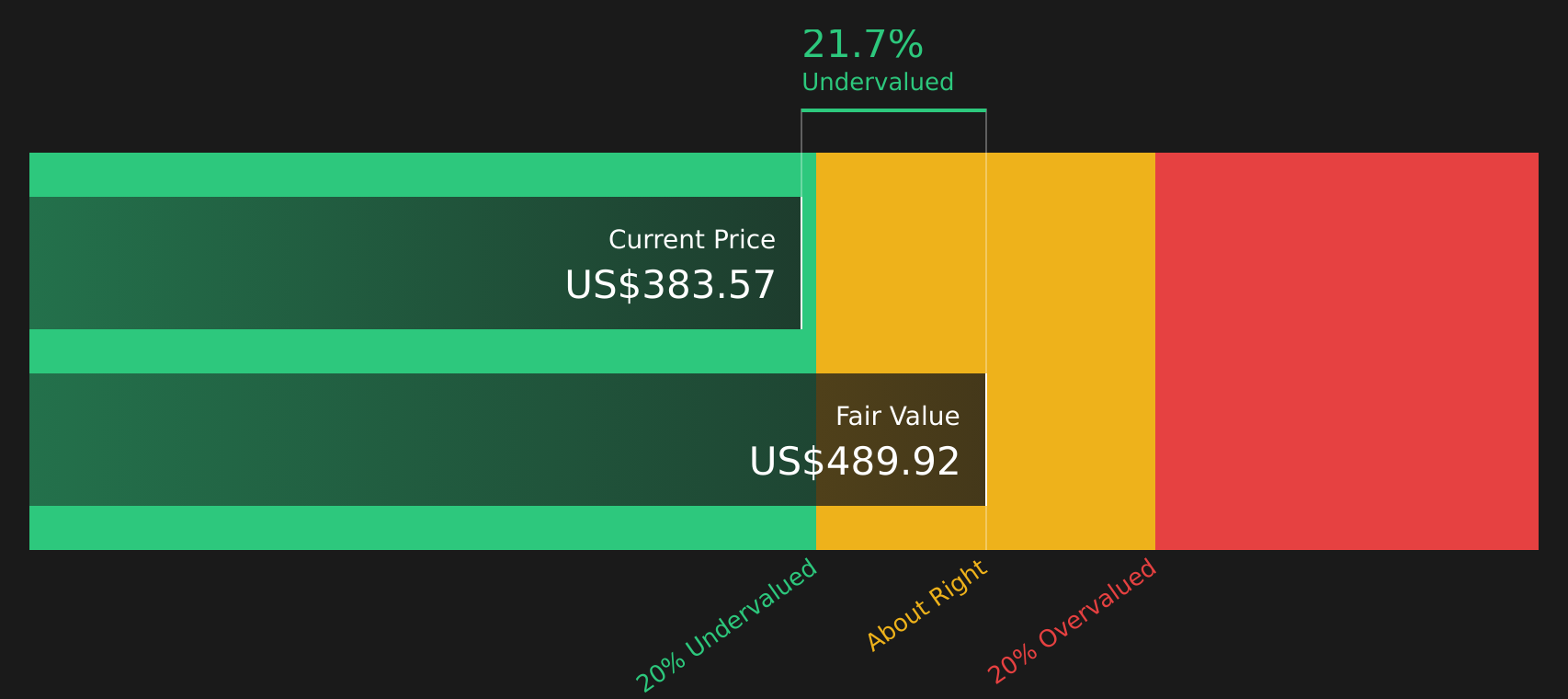

Waters trades at a discount to one set of analyst price targets and an estimated intrinsic value, even as it reports US$3.2b in revenue and US$642.6m in net income. Is this weakness a buying opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 23.7% Undervalued

Waters' most followed narrative sets a fair value of $393.14 per share, compared with the last close of $299.79, using a 7.9% discount rate to frame long term cash flows.

Recurring revenues are accelerating (up 11% this quarter), underpinned by expanding service plan attachments and e-commerce adoption, which enhances revenue stability and net margins, setting up the combined company for more resilient earnings across CapEx cycles.

Curious what kind of revenue trajectory and margin profile need to line up for that fair value to work? The narrative leans on ambitious top line expansion, evolving profitability, and a future earnings multiple that assumes Waters keeps earning a premium position in its niche.

Result: Fair Value of $393.14 (UNDERVALUED)

However, this hinges on Waters managing the BD integration without major synergy shortfalls and on keeping margin pressure from tariffs and regional mix from biting harder than expected.

Another Way To Look At Value

The Simply Wall St DCF model puts Waters' future cash flow value at $439.45 per share, compared with the current price of $299.79. That points to a sizeable gap on paper. However, it rests on long range cash flow assumptions, so how comfortable are you with those inputs?

Next Steps

Seeing mixed signals on value, risks and rewards here? Take a closer look at the full data, cross check the assumptions, and weigh the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Waters is on your radar, do not stop here, the right mix of quality and price often shows up where most investors are not yet looking.

- Target quality at a discount by scanning companies that combine strong fundamentals with appealing valuations through the 53 high quality undervalued stocks.

- Prioritise resilience by checking businesses that rank well on financial strength and balance sheet quality via the solid balance sheet and fundamentals stocks screener (43 results).

- Hunt for underfollowed opportunities by reviewing a screener containing 25 high quality undiscovered gems before others catch on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.