A Look At Willis Lease Finance (WLFC) Valuation As Willis Aviation Capital Launches With New Institutional Partnerships

Willis Lease Finance Corporation WLFC | 175.89 | +0.15% |

Willis Lease Finance (WLFC) has drawn fresh investor attention after launching Willis Aviation Capital, a new division that manages third-party aviation assets and capital through discretionary funds, in partnership with Blackstone Credit & Insurance and Liberty Mutual Investments.

The WAC launch and new partnerships appear to coincide with a sharp shift in sentiment, with a 90 day share price return of 18.77% and a five year total shareholder return of 344.13%. This suggests momentum is building after a weaker one year total shareholder return with a 24.08% decline.

If this kind of aviation engine story interests you, it could be a useful moment to widen your watchlist with aerospace and defense stocks as potential comparison ideas.

With WLFC shares up strongly in recent months, trading at US$155.82 and only a small discount to a US$160 price target, the key question is whether the market still undervalues the new WAC engine or if future growth is already priced in.

Price to Earnings of 9.1x: Is it justified?

On a P/E of 9.1x and a last close of US$155.82, Willis Lease Finance screens as inexpensive compared to both its peer group and the wider US market.

The P/E multiple compares the current share price to earnings per share, so it is essentially the market’s price tag on each dollar of current earnings. For a business that leases and services commercial aircraft engines, earnings quality and consistency tend to matter more to investors than rapid top line expansion.

Here, WLFC’s current P/E of 9.1x sits well below the US market average of 19.3x. This suggests investors are paying a lower price for each dollar of earnings. At the same time, the company reports high quality earnings and earnings growth of 23.4% over the past year, although this growth rate is below its 5 year earnings growth average and current net profit margins of 17.3% are lower than last year’s 18.2%.

The discount looks even clearer when you compare WLFC to the US Trade Distributors industry on 21.9x and a peer average on 27.6x. In both cases, WLFC’s P/E of 9.1x is less than half those levels. This points to a much lower earnings multiple than what similar businesses are trading on right now.

Result: Price to Earnings of 9.1x (UNDERVALUED)

However, you still need to weigh risks such as the recent 24.08% one-year total shareholder return decline and execution challenges as Willis Aviation Capital ramps up.

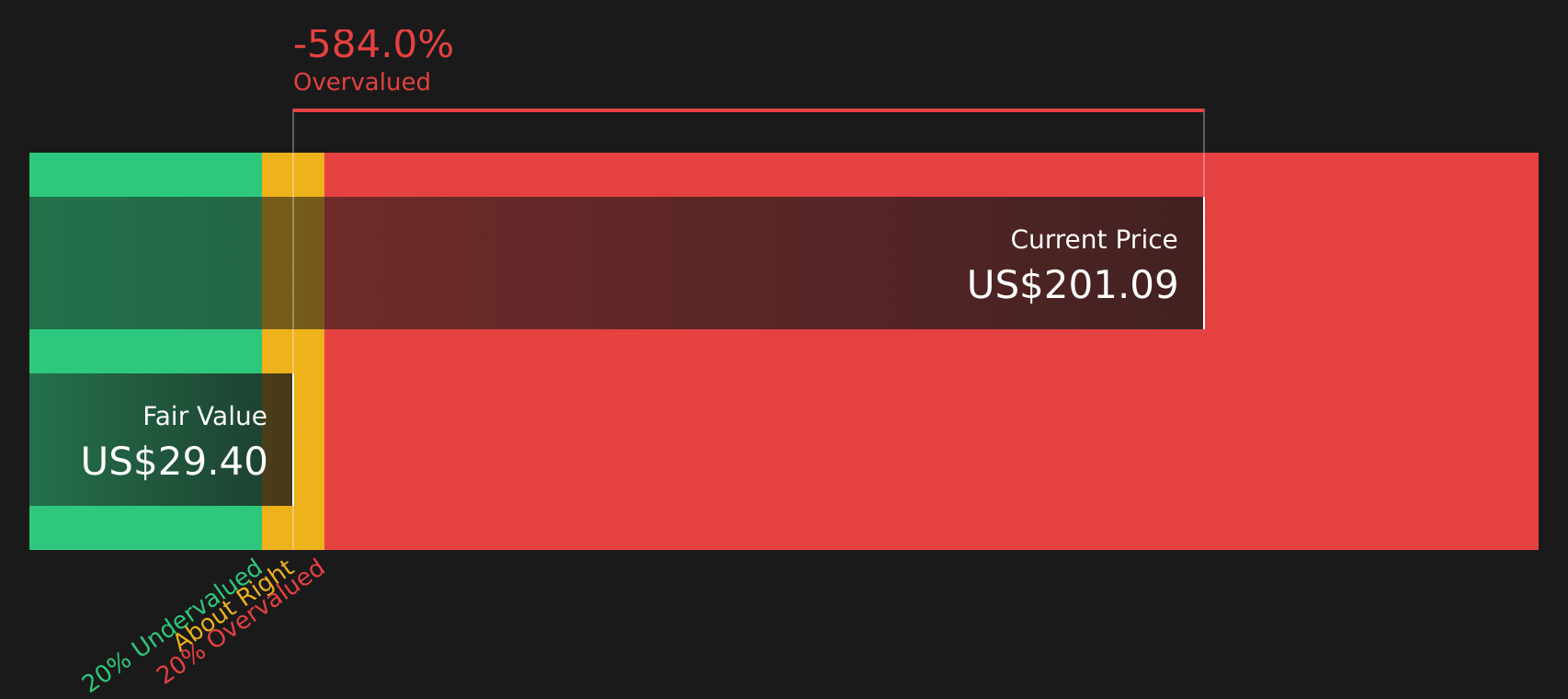

Another View: Our DCF Model Flags Overvaluation

While the 9.1x P/E makes Willis Lease Finance look inexpensive next to the US market and Trade Distributors peers, our DCF model points in the opposite direction. At a last close of US$155.82 versus a fair value estimate of US$28.04, the stock screens as overvalued on this approach.

This gap suggests that if cash flows end up closer to the DCF assumptions than to current market optimism, there is valuation risk rather than a clear bargain. It raises a simple question for you as an investor: which view do you trust more, the earnings multiple or the cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Willis Lease Finance for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 882 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Willis Lease Finance Narrative

If you look at the numbers and reach a different conclusion, that is a strength. You can test your own view and build a full narrative in under three minutes, starting with Do it your way.

A great starting point for your Willis Lease Finance research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Willis Lease Finance has sharpened your focus, do not stop here; the real edge comes from comparing a few carefully chosen alternatives side by side.

- Spot potential value candidates by checking out these 882 undervalued stocks based on cash flows that may be pricing in more caution than their cash flows suggest.

- Target high yield potential and review these 12 dividend stocks with yields > 3% that could help you build a steady income stream alongside capital growth ideas.

- Lean into structural change in digital assets and scan these 79 cryptocurrency and blockchain stocks that are building businesses around cryptocurrency and blockchain themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.