A Look At Zymeworks (ZYME) Valuation After Recent Clinical And Regulatory Milestones

Zymeworks Inc. ZYME | 0.00 |

Zymeworks (ZYME) stock has been reacting to a series of clinical and regulatory milestones, including new Phase 1 data, a U.S. PDUFA date, and a China filing for its HER2 targeted therapy.

Despite the recent clinical and regulatory progress, Zymeworks shares have come under pressure in the short term, with the 1 month share price return down 12.93% and the year to date share price return down 9.69%. However, the 1 year total shareholder return of 90.79% and 3 year total shareholder return of 182.16% point to strong momentum over a longer horizon.

If this kind of biotech news has your attention, it can be useful to widen the lens and see what else is gaining traction in healthcare focused AI, starting with 39 healthcare AI stocks.

With the stock recently under pressure despite clinical and regulatory milestones, and with Zymeworks trading below some analyst price targets, the key question is whether there is a fresh entry point here or whether the market already reflects expectations for future growth.

Most Popular Narrative: 40% Undervalued

At a last close of $24.04 against a narrative fair value of about $40.08, the market price and the most followed valuation story are clearly out of sync.

Zymeworks' strategic partnership and out licensing approach with large pharmaceutical companies (e.g., Jazz, BeiGene, BMS, J&J) is generating significant near term and long term non dilutive cash inflows, diversifying revenue streams and reducing the R&D burn rate, thus supporting better EBITDA margins and enhanced cash flow stability as the partnered assets advance.

Want to see what kind of revenue mix, margin shift, and future earnings multiple are baked into that fair value? The narrative leans on bold growth, profitability and royalty assumptions that are anything but conservative.

Result: Fair Value of $40.08 (UNDERVALUED)

However, investors still need to watch for partner execution and regulatory timing, as well as the high dependency on milestone and royalty payments to support cash flows.

Another Angle on Valuation

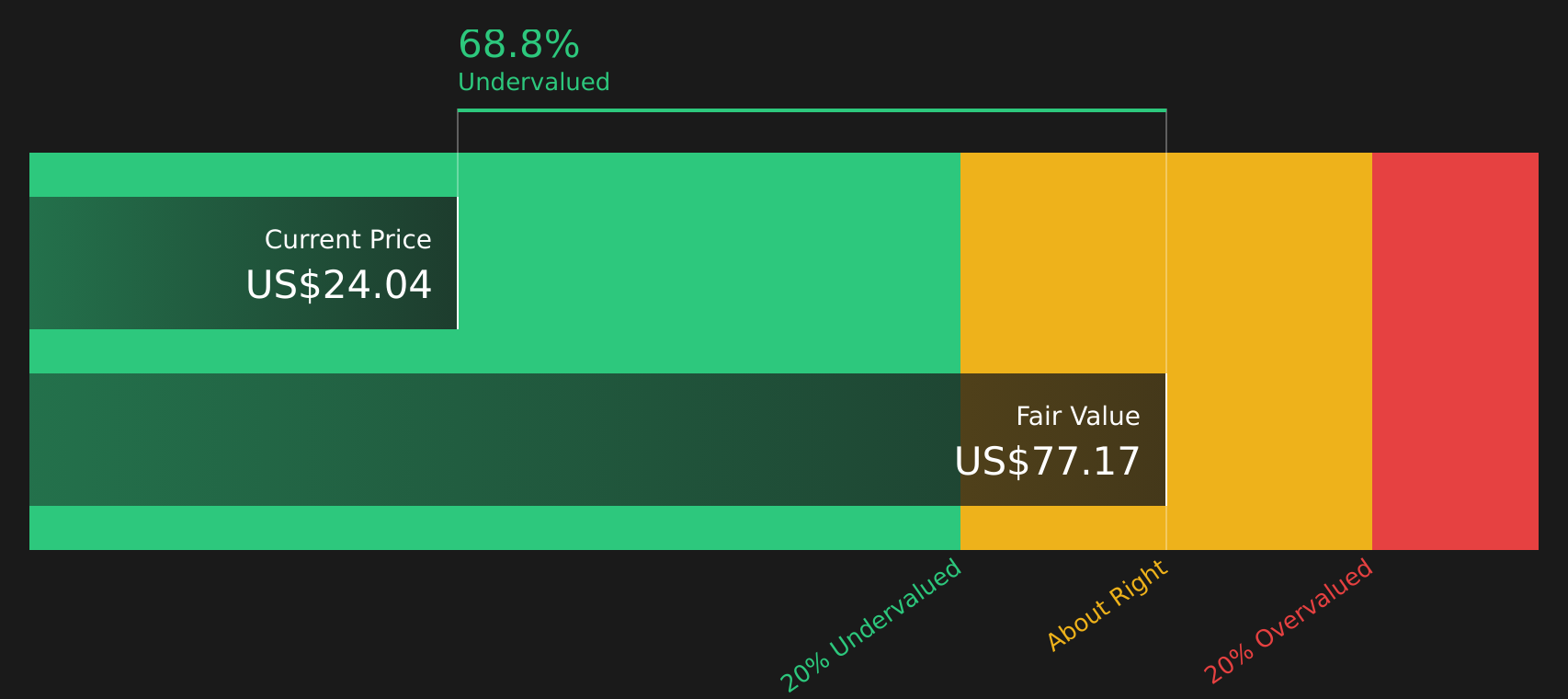

While the narrative fair value sits at $40.08, our DCF model presents a more optimistic view, putting Zymeworks' future cash flow value at $77.17, with the stock trading about 68.8% below that estimate. If both signals are pointing higher, the key consideration is how comfortable you are with the assumptions underlying each approach.

Next Steps

If the mix of optimism and caution in this article feels familiar, use it as a prompt to move quickly and test the numbers yourself rather than just the headlines, then round out your view by checking the 3 key rewards

Looking for more investment ideas?

If Zymeworks has sharpened your thinking, do not stop here. Broaden your watchlist with a few focused ideas that could round out your portfolio.

- Target stability by scanning companies that pass strict balance sheet checks with the solid balance sheet and fundamentals stocks screener (46 results).

- Hunt for potential mispricings using the 49 high quality undervalued stocks before others catch on to the same opportunities.

- Spot lesser known opportunities with solid fundamentals through the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.