ADTRAN Holdings (ADTN) Settles Patent Litigation, Is The Stock Trading At A Premium?

ADTRAN Holdings, Inc. ADTN | 0.00 |

ADTRAN Holdings (ADTN) has fully settled a multi year patent lawsuit, with all claims dismissed with prejudice and a payment received. This removes a legal overhang that had been in place since 2020.

Despite the legal resolution, ADTRAN Holdings’ recent momentum has cooled, with the share price down 30.28% over the past month and 9.33% over the past week, even though the year to date share price return is 46.66% and the 1 year total shareholder return is 33.16%.

If this kind of legal and boardroom activity has you thinking about where else capital could work hard, it may be worth scanning 20 top founder-led companies for other compelling business stories.

With ADTRAN Holdings now past a major legal hurdle yet still trading well below analyst targets and reporting a loss of $31.3 million on revenue of $1.12 billion, is the recent pullback a genuine opportunity, or is the market already discounting weaker future growth?

Most Popular Narrative: 34.7% Undervalued

At a last close of $12.73 against a fair value narrative of $19.50, ADTRAN Holdings is framed as materially mispriced by the most followed story on the stock.

Expanding global demand for high-speed broadband, particularly residential fiber upgrades and multi-gigabit services, is fueling strong customer wins and backlog growth across both North America and Europe, supporting continued revenue acceleration over the coming quarters. Rising infrastructure investment for AI computing, cloud, and 5G densification is driving higher demand for ADTRAN's optical networking solutions and cross-selling opportunities, which should boost both revenue and market share as these trends intensify.

Curious how a modest revenue growth outlook, a slim profit margin swing and a rich future earnings multiple are combined to support that $19.50 fair value? The narrative leans on a detailed earnings path and a specific discount rate to bridge today’s loss making position with a future profit stream that justifies a steep valuation hurdle.

Result: Fair Value of $19.50 (UNDERVALUED)

However, ADTRAN Holdings still faces meaningful risks, including currency swings affecting margins and the possibility that current vendor replacement wins will be difficult to repeat.

Another View: ADTRAN Holdings Through a Cash Flow Lens

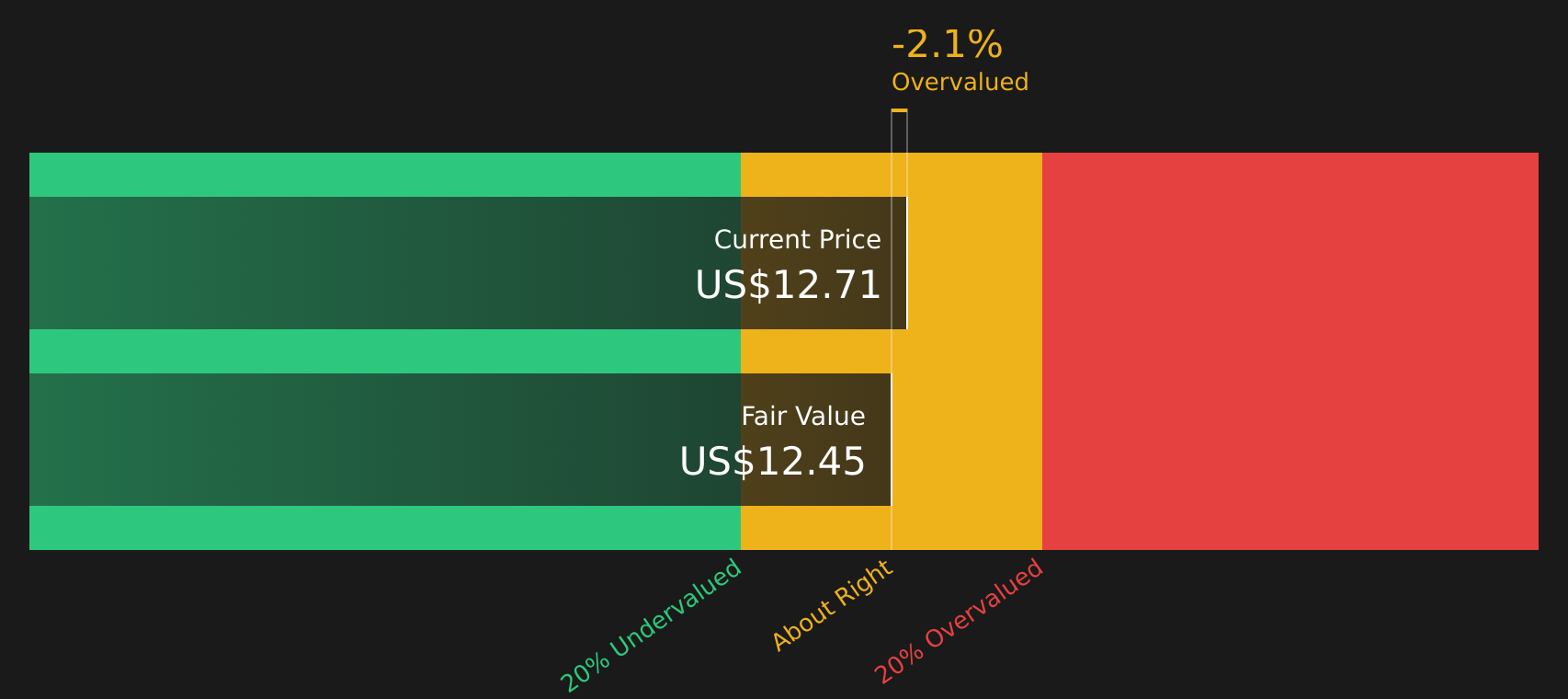

The popular narrative around ADTRAN Holdings leans on a fair value of $19.50, yet our DCF model tells a cooler story. On those cash flow assumptions, the stock at $12.73 sits slightly above an estimated value of $12.45, pointing to a small premium rather than a clear bargain.

This raises a simple question for investors: is the richer narrative or the more cautious cash flow math closer to how you see ADTRAN Holdings?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ADTRAN Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 42 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around ADTRAN Holdings and its valuation, do not wait on others to frame the story for you. Weigh the data, stress test both sides of the argument, and see how the balance of 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond ADTRAN Holdings?

If the debate around ADTRAN Holdings has sharpened your thinking, use that momentum to line up other opportunities that match your risk tolerance and return goals.

- Target stronger fundamentals by scanning the solid balance sheet and fundamentals stocks screener (46 results) and focus on companies with healthier financial footing.

- Hunt for mispriced potential through the 42 high quality undervalued stocks and see which stocks the data suggests may trade below their underlying strength.

- Build a steadier income stream by reviewing the 7 dividend fortresses and spot companies offering higher yields with supporting fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.