Advance Auto Parts (AAP) Same Store Sales Rebound Tests Profitability Turnaround Narratives

Advance Auto Parts, Inc. AAP | 56.59 | -0.51% |

Latest earnings snapshot and why it matters for the AAP story

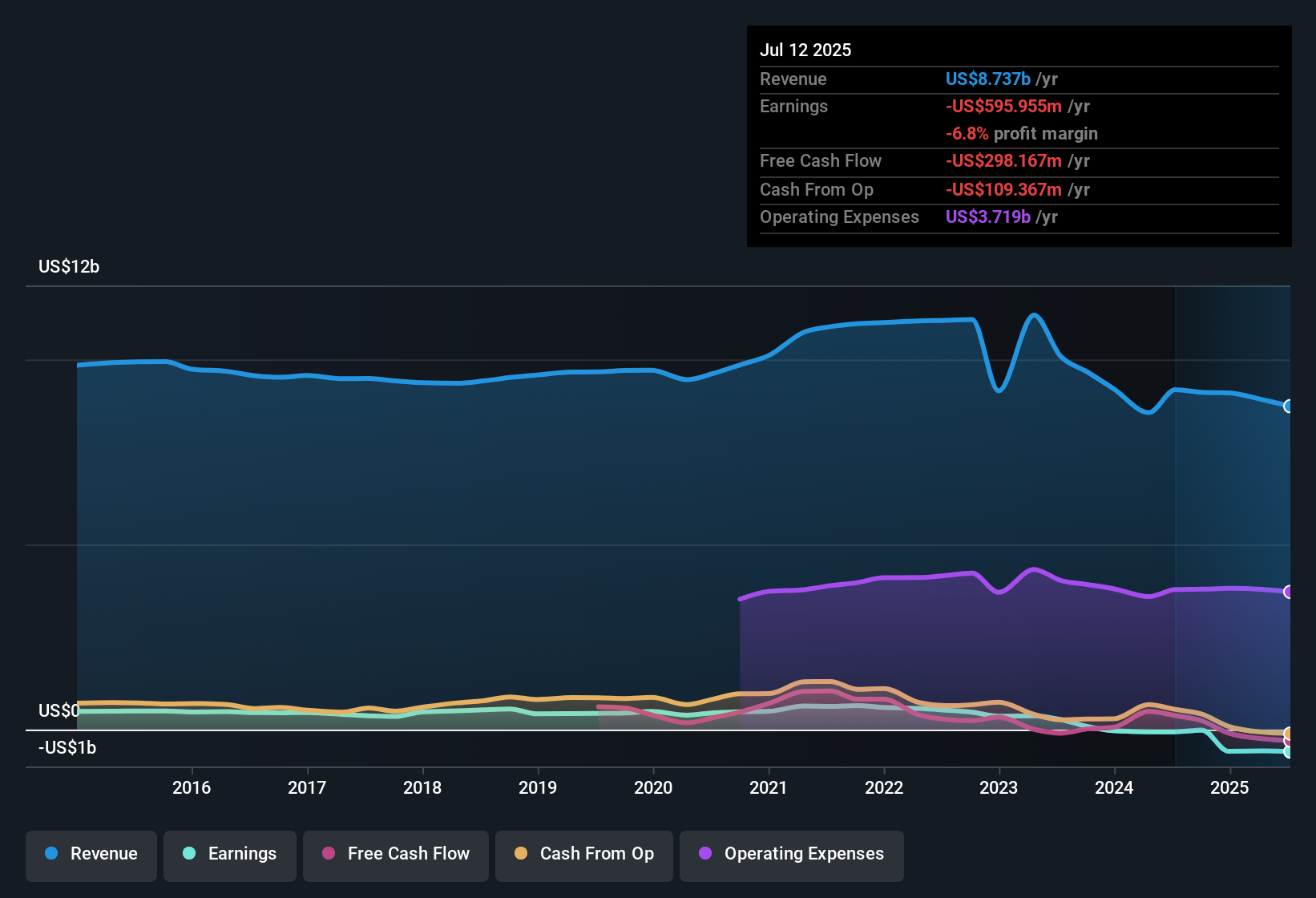

Advance Auto Parts (AAP) just posted third quarter FY 2025 revenue of about US$2.0 billion with basic EPS near breakeven at roughly US$0.02 loss, setting a cautious tone after a run of mixed results. The company has seen quarterly revenue move from US$2.18 billion in the second quarter of FY 2024 to US$2.58 billion in the first quarter of FY 2025, while basic EPS has swung from a US$10.20 loss in the fourth quarter of FY 2024 to a US$0.40 profit in the first quarter of FY 2025 before slipping back into a small loss this quarter. This keeps the focus squarely on how much of that top line is actually making it through to the bottom line.

See our full analysis for Advance Auto Parts.With the numbers on the table, the next step is to see how this margin story lines up against the prevailing Advance Auto Parts narratives that investors have been using to frame the stock.

Same store sales improve to 3%

- Comparable sales moved from 0.1% growth in Q2 FY 2025 to 3% in Q3, while total revenue was roughly flat at US$2.0 billion versus US$2.0 billion in the prior quarter.

- Supporters of the bullish narrative argue that better assortments and supply chain optimization can lift comps, and this sales mix shift lines up with that view, but:

- Same store sales in Q1 FY 2025 were slightly weaker at a 0.6% decline, so the latest 3% figure is an improvement on what has been a choppy pattern.

- Trailing 12 month revenue is about US$8.6b, with growth cited at 1.9% a year, which is still modest even if store level metrics are starting to look healthier.

Bulls suggest that if operational fixes are working at the store level, that could be an early sign their margin and growth story is taking hold, and the detailed upside case is laid out in 🐂 Advance Auto Parts Bull Case

Trailing losses vs 55.61% growth forecasts

- On a trailing 12 month basis AAP reported a net loss of roughly US$572 million and Basic EPS of US$9.55 loss, yet the same data set points to forecast earnings growth of 55.61% a year with an expectation of returning to profit within three years.

- Analysts who are bullish see today’s loss making base as a starting point for a sharp recovery, but the current numbers set a high bar for that view:

- Losses have grown at about 64.2% a year over the past five years, which sits in clear tension with the idea that earnings can now compound positively at 55.61% a year.

- The latest quarterly income line shows a US$1 million loss, not a profit, so any turnaround case still rests on future improvement rather than earnings that are already consistently positive.

Unprofitable with a 1.72% dividend

- AAP remains unprofitable on a trailing 12 month view with about US$8.6b in revenue and a US$572 million net loss, while the dividend yield of 1.72% is flagged as not being covered by earnings or free cash flow.

- Bears focus on this payout gap and cash strain as a key weak point, and the current data gives that concern some weight:

- Net income excluding extra items has been negative in three of the last five reported quarters, including a US$610 million loss in Q4 FY 2024, so there is limited recent history of the business fully funding its dividend from profits.

- Analysts also highlight that revenue growth around 1.9% a year trails an expected 10.4% for the wider US market, so slower top line progress may make it harder to grow into the existing payout.

If you are more aligned with the cautious camp that worries about sustained losses and dividend coverage, the detailed downside case is unpacked in 🐻 Advance Auto Parts Bear Case

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Advance Auto Parts on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Take a couple of minutes to test your own view against the data and turn it into a clear narrative: Do it your way

A great starting point for your Advance Auto Parts research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

AAP is dealing with trailing losses, a thinly covered 1.72% dividend and uneven earnings results, which may leave income-focused investors facing additional uncertainty.

If that mix of losses and dividend pressure feels uncomfortable, you might want to review companies in our 13 dividend fortresses that aim for stronger, more reliable income profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.