Agilent Technologies (A): Is the Stock Undervalued After Recent Momentum Cools?

Agilent Technologies, Inc. A | 115.01 | +0.41% |

Agilent Technologies (A) shares recently caught the attention of investors following a move in the broader pharmaceuticals and biotech sector. The company has delivered solid annual revenue and net income growth, even as short-term returns remain mixed.

After a robust rally throughout the past quarter, Agilent's share price has cooled slightly in the last week, settling at $146.89. Despite this short-term pause, momentum remains positive for the stock, which notched a strong 23.2% 90-day share price return and has delivered a 13.7% total return for shareholders over the past year.

If this kind of momentum sparks your curiosity, it might be the perfect moment to explore leaders across the healthcare space with the See the full list for free.

With shares hovering just below analyst targets and strong growth metrics in hand, the real question remains: Is Agilent still undervalued, or has the market already baked in the company’s future prospects? This raises the question of whether this is a true buying opportunity or not.

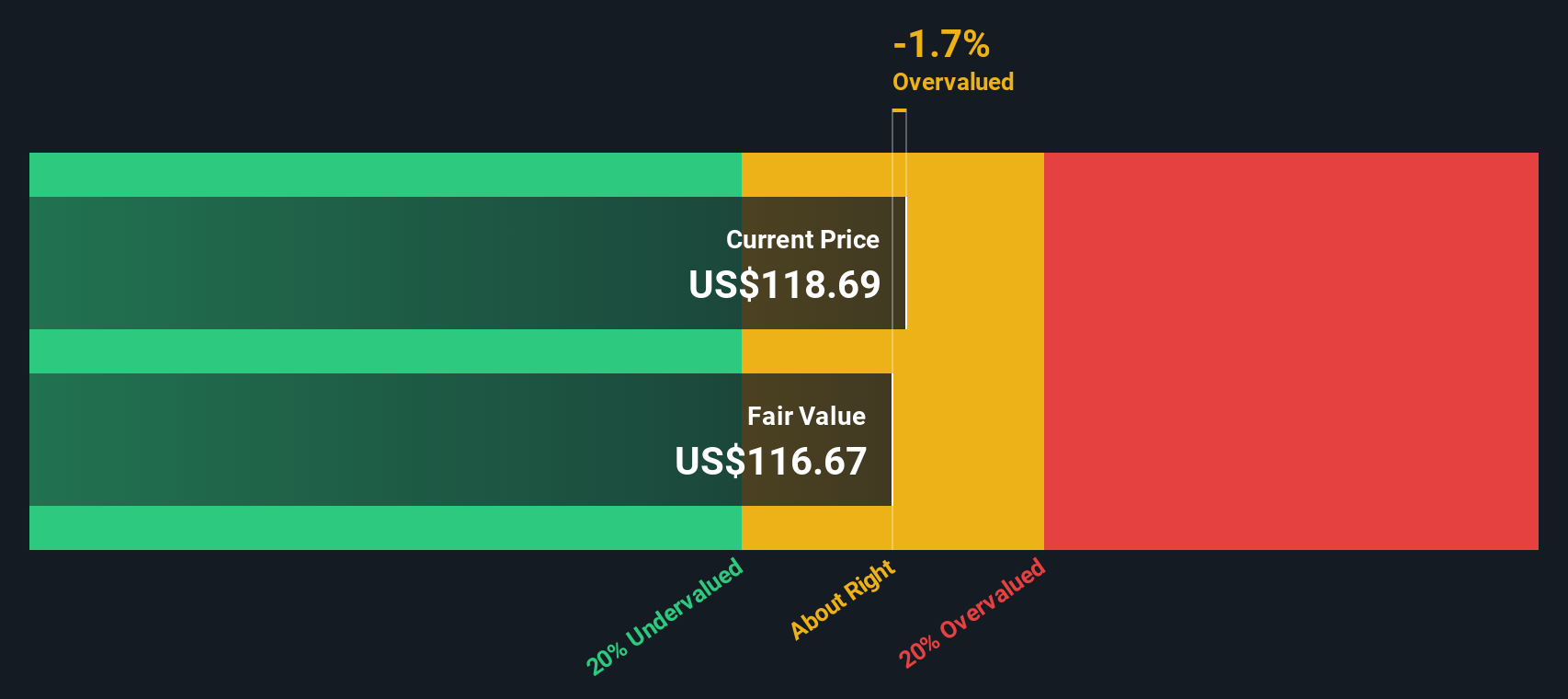

Most Popular Narrative: 2% Undervalued

Agilent Technologies’ most widely followed narrative places its fair value at $149.90, just above the last close of $146.89. The debate is heating up as analysts and investors try to justify this premium and what could propel the stock higher from here.

Strategic investments in higher-margin recurring revenue streams, including consumables, software, services, and digital platforms, are gaining traction. CrossLab and services are delivering consistent mid-single-digit growth and high customer satisfaction, indicating further margin expansion and greater earnings stability in future periods.

Curious how recurring revenues and margin advances drive Agilent's compelling valuation? The secret sauce lies in bold margin assumptions and a specific profit leap engineered into this narrative. Dive in to discover which future financial shifts are the linchpin of this bullish outlook.

Result: Fair Value of $149.90 (UNDERVALUED)

However, heightened tariffs or prolonged funding pressures in key markets could present challenges and affect sentiment regarding Agilent’s growth narrative.

Another View: What Does the DCF Model Say?

While analysts see Agilent as slightly undervalued, our DCF model takes a different view. By projecting future cash flows, it estimates Agilent's fair value at $90.53 per share, which is well below the latest trading price. Could the market be far too optimistic about Agilent’s growth prospects, or is the DCF model missing something investors can see?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Agilent Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 874 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Agilent Technologies Narrative

Prefer to form your own view? You can explore the numbers, test your perspective, and shape your own narrative in just a few minutes: Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Agilent Technologies.

Looking for More Investment Ideas?

Don’t let opportunity pass you by. Take the next step and supercharge your investment search with uniquely targeted stock ideas tailored for bold investors.

- Capture the upside of market mispricings when you dig into these 874 undervalued stocks based on cash flows to find significant growth potential at bargain prices.

- Tap into the explosive rise of intelligent tech by checking out these 27 AI penny stocks that are positioned to benefit from the AI revolution.

- Boost your income strategy and financial security with these 15 dividend stocks with yields > 3% featuring attractive yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.