AI-Enabled ATTR-CM Care Pathway Initiative Might Change The Case For Investing In Alnylam Pharmaceuticals (ALNY)

Alnylam Pharmaceuticals, Inc ALNY | 318.85 | -3.01% |

- Alnylam Pharmaceuticals recently outlined new efforts to improve earlier recognition and coordinated care for cardiomyopathy in wild-type and hereditary transthyretin-mediated amyloidosis, partnering with Viz.ai to integrate an FDA-cleared echocardiography AI algorithm into real-world clinical workflows through the AWARE study at five US health systems.

- In parallel, Alnylam is backing a three-year American Heart Association program that will convene a 10-center national learning collaborative to refine, standardize, and scale best-in-class ATTR-CM diagnosis and care pathways across multidisciplinary teams.

- We’ll now examine how this AI-enabled ATTR-CM care pathway initiative could influence Alnylam’s existing investment narrative around its TTR franchise.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Alnylam Pharmaceuticals Investment Narrative Recap

To own Alnylam, you have to believe its RNAi platform and TTR franchise can justify a rich valuation while the company manages pricing pressure, margin compression, and concentration in AMVUTTRA. The new AI-enabled ATTR-CM care initiatives look directionally supportive for earlier disease recognition but do not materially change the near term focus on pricing, gross margin trends, and execution across the TTR franchise.

Among recent developments, Alnylam’s 2026 revenue guidance of US$4,900 million to US$5,300 million sits at the center of the current catalyst debate. Against that backdrop, the Viz.ai and American Heart Association collaborations matter mainly if they eventually support broader identification of ATTR-CM patients, potentially reinforcing confidence in the TTR revenue outlook while leaving existing risks around net price erosion and high royalty burdens firmly in view.

Yet against this constructive setup, investors should also recognize the concentration risk in AMVUTTRA and the potential impact of tighter payer controls on...

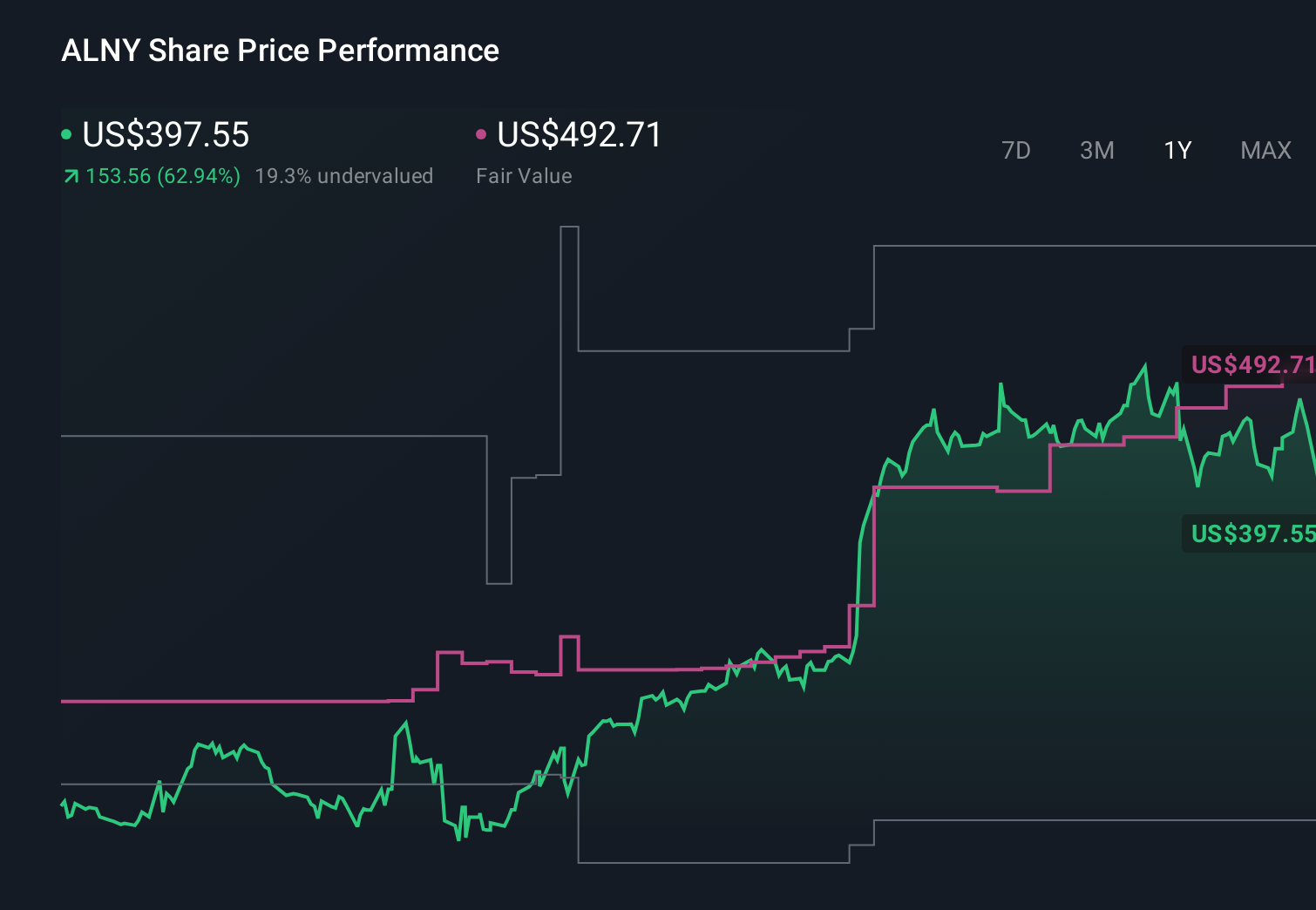

Alnylam Pharmaceuticals’ narrative projects $7.0 billion revenue and $1.9 billion earnings by 2028. This requires 41.8% yearly revenue growth and about a $2.2 billion earnings increase from -$319.1 million.

Uncover how Alnylam Pharmaceuticals' forecasts yield a $491.92 fair value, a 55% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already modeled revenue reaching roughly US$11.4 billion and earnings of about US$3.4 billion by 2029, so this kind of AI-enabled ATTR-CM initiative could eventually shift those projections further, or challenge them, depending on how you view the concentration risk around AMVUTTRA and whether these care pathway efforts truly broaden the TTR opportunity set over time.

Explore 5 other fair value estimates on Alnylam Pharmaceuticals - why the stock might be worth as much as 95% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alnylam Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alnylam Pharmaceuticals' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 62 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.