AllianceBernstein (AB) Stock Looks Near Fair Value, Not A Clear Bargain

AllianceBernstein Holding L.P. AB | 0.00 |

AllianceBernstein Holding stock has delivered a 50.5% gain over the past three years, yet current checks suggest it now sits close to intrinsic value on the Excess Returns model, while earnings based multiples lean on the expensive side. That split, together with a mixed overall value score, puts the focus on whether the recent share price around US$36.79 still offers an appealing entry point.

- AllianceBernstein Holding has returned 50.5% over three years, a solid outcome that raises the bar for what counts as good value from here.

- Future fee income and cash flows from its asset management franchise can support the valuation, but pressure on margins or assets under management would quickly matter for what investors are willing to pay.

- With a value score of 3 out of 6, the broader checks point to a mixed picture rather than a clear bargain or clear overvaluation.

The issue now is whether AllianceBernstein Holding’s current price fairly reflects its intrinsic value estimate, or if the premium signaled by market multiples leaves limited room for disappointment.

Where Does AllianceBernstein Holding Sit on Excess Returns?

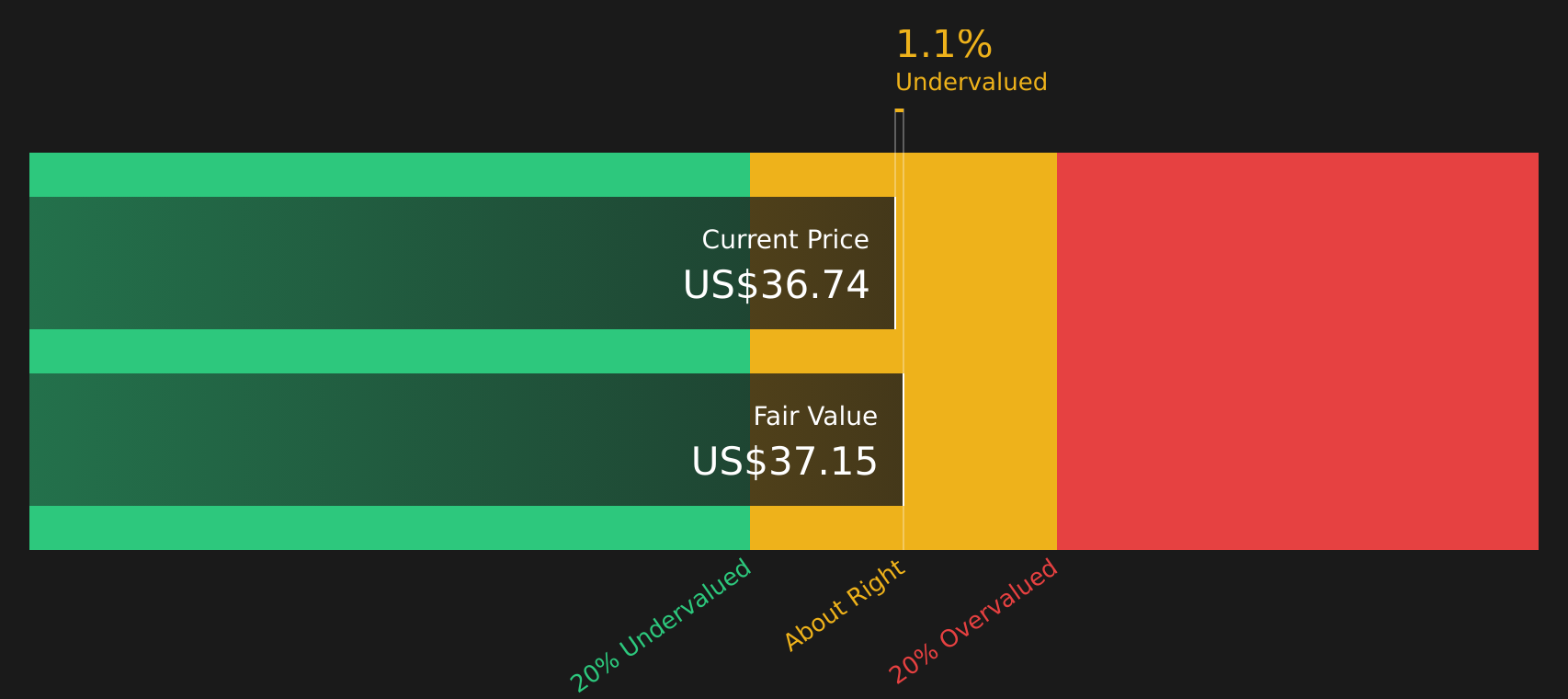

The Excess Returns model looks at how efficiently AllianceBernstein Holding turns its equity base into profits above the cost of that equity. For this stock, the framework uses a Book Value of $13.50 per share and a Stable EPS estimate of $2.76 per share, based on the median return on equity over the past five years. With a Cost of Equity of $1.67 per share and an Excess Return of $1.09 per share, the model assumes the company can continue to earn returns above what investors require, supported by an Average Return on Equity of 15.31% and a Stable Book Value of $18.00 per share.

These inputs produce an intrinsic value estimate of $36.96 per share, very close to the recent share price around $36.79. That gap points to a small implied discount of about 0.5%, suggesting AllianceBernstein Holding is trading in line with what its excess returns profile supports rather than at a clear bargain or premium.

On this model, AllianceBernstein Holding looks roughly fairly valued, with the share price sitting very close to the computed intrinsic value.

AllianceBernstein Holding is fairly valued according to our Excess Returns, but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Does AllianceBernstein Holding Look Pricey on Earnings?

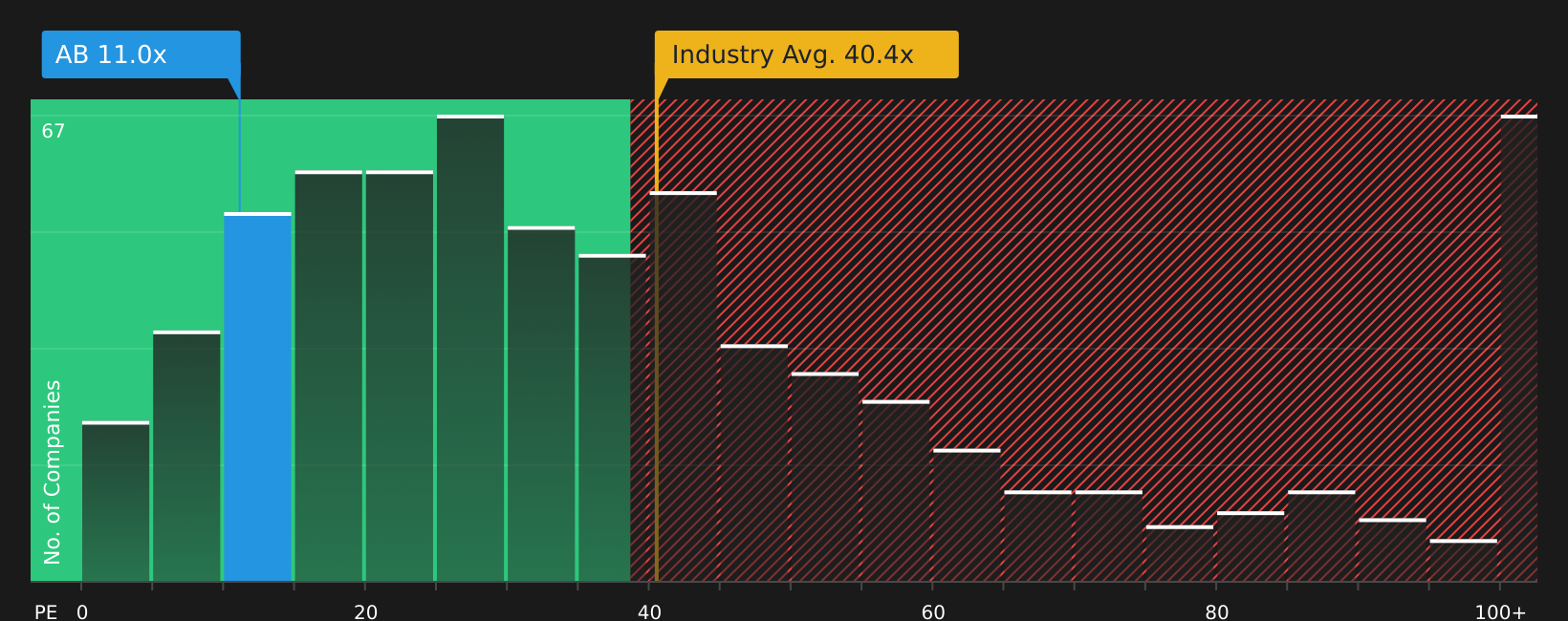

P/E is a useful anchor for AllianceBernstein Holding because earnings and fee income are central to how investors typically price asset managers. On this measure, the stock trades on about 11.0x earnings, compared with a peer average of roughly 14.0x and a much higher Capital Markets industry average of about 40.6x. That puts AllianceBernstein Holding at a discount to both direct peers and the broader industry on simple P/E comparisons.

The fair P/E ratio implied by the model is around 8.2x, which is lower than the current 11.0x. Even though the raw P/E looks modest next to many Capital Markets stocks, this framework, which also considers factors such as the company’s risk profile and business mix, points to AllianceBernstein Holding trading above the level it would flag as justified on earnings.

On this P/E yardstick, AllianceBernstein Holding screens as overvalued relative to the model’s fair multiple.

The AllianceBernstein Holding Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where AllianceBernstein Holding's valuation puzzle leaves off by spelling out which paths for growth, margins and earnings would need to play out for the stock to be worth materially more or less than today’s price. Each narrative ties its number to a clear view on how AllianceBernstein Holding's growth, profitability and risks could evolve, giving you a reference point to revisit as new information surfaces on the Community page.

If you have a clear, number driven view on where AllianceBernstein Holding's growth, margins and execution go from here, add your Narrative to the Simply Wall St community and put your case on the record. It is a chance to set out your valuation logic today and see how it stacks up as fresh data comes through.

Do you think there's more to the story for AllianceBernstein Holding? Head over to our Community to see what others are saying!

The Bottom Line

For AllianceBernstein Holding, the Excess Returns intrinsic value estimate and the current share price sit almost on top of each other, which points to the stock being roughly fully priced on that framework. The earnings multiple, however, suggests the shares are overvalued relative to what the model views as a fair P/E. Together, the mixed valuation picture implies you are no longer looking at an obvious bargain, but not a clear excess either. The key swing factor from here is whether AllianceBernstein Holding can deliver the fee income and profitability that keep justifying a premium to its intrinsic value markers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.