Allison Transmission Holdings (ALSN) Valuation Under Scrutiny As Growth Expectations Cool In Challenging Demand Conditions

Allison Transmission Holdings, Inc. ALSN | 117.06 | -1.50% |

Allison Transmission Holdings (ALSN) has been under scrutiny as recent commentary points to a challenging demand backdrop, with anticipated sales decline and slower revenue and earnings growth than industrial peers weighing on sentiment.

The recent executive reshuffle and the acquisition of Dana’s Off-Highway Drive & Motion Systems have arrived alongside a 90 day share price return of 28.58% and a 30 day share price return of 9.03%. However, the 1 year total shareholder return is a 6.23% loss and the 5 year total shareholder return is 167.66%, so momentum appears stronger in the short term than over the last year.

If Allison’s recent move has you watching capital goods more closely, it could be worth scanning aerospace and defense stocks for other companies exposed to commercial and defense related demand shifts.

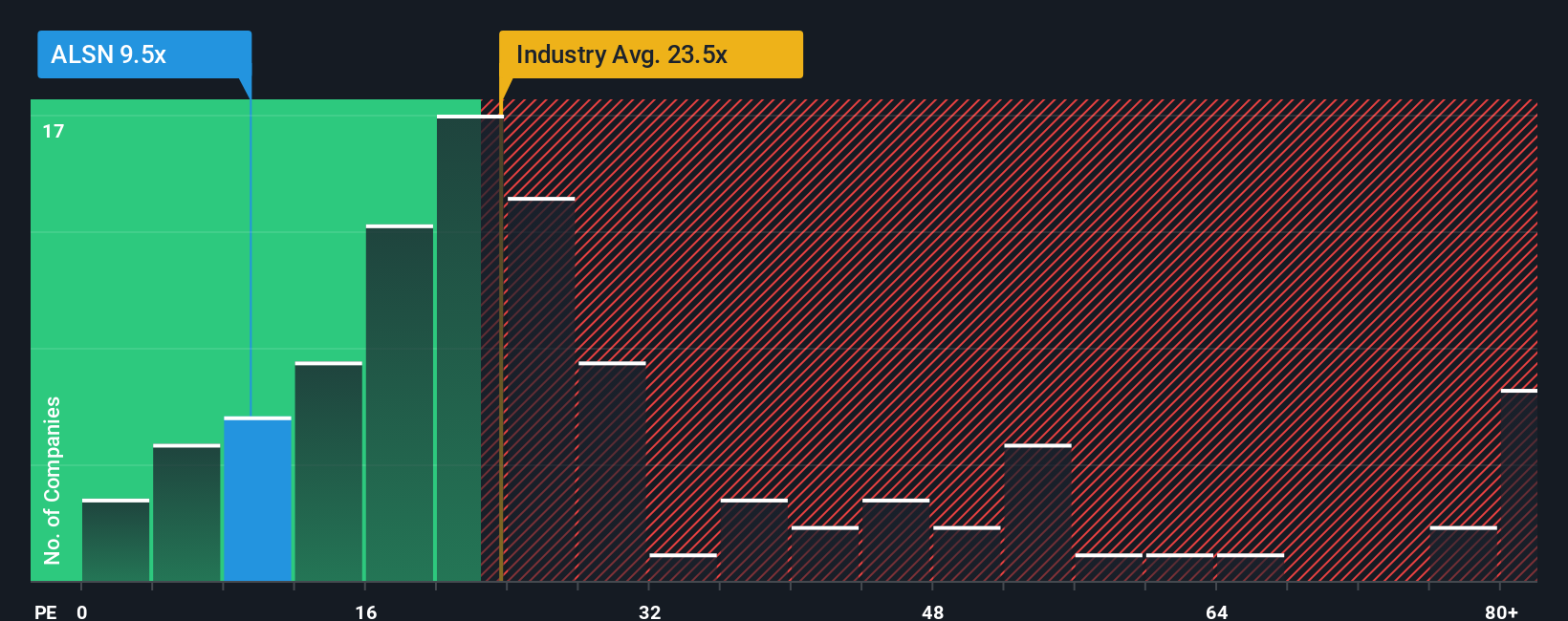

Allison now trades close to its US$104.80 analyst price target on a forward P/E of 14.3x, despite forecasts for a 4.7% sales decline and slower earnings growth. Is this a genuine opportunity, or is future growth already priced in?

Most Popular Narrative: 2% Overvalued

Compared with the last close at US$102.18, the most followed narrative sees fair value at US$100.20, hinting at only a small valuation gap.

Structural trends in global infrastructure investment highlighted by strong growth in international markets (notably South America and Europe) are broadening Allison's addressable market and are likely to drive sustained demand for its drivetrain solutions, bolstering top-line growth and reducing geographic earnings concentration risk.

Curious what earnings path, margin profile, and future P/E this narrative leans on to call out that price gap? The full story spells it out.

Result: Fair Value of $100.20 (OVERVALUED)

However, the story could change quickly if electrification trends accelerate faster than Allison’s hybrid and transmission offerings, or if the Dana Off-Highway integration falls short of expected synergies.

Another View: Multiples Send a Different Signal

While the popular narrative flags Allison as about 2% overvalued around US$100.20, our P/E based view points in a different direction. At 12.2x earnings versus 22.7x for both peers and the fair ratio, the current price leaves a wide gap that could be a cushion or a value trap, depending on how you see the risks around debt, truck demand and electrification.

Build Your Own Allison Transmission Holdings Narrative

If you see the numbers differently or prefer to test your own assumptions against the data, you can build a custom view in minutes: Do it your way.

A great starting point for your Allison Transmission Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Allison has your attention, do not stop here. Use the Simply Wall St Screener to quickly spot fresh stock ideas that fit your own style.

- Target high potential turnarounds by scanning these 881 undervalued stocks based on cash flows that the market may be pricing cautiously despite their cash flow profile.

- Spot early movers in transformative tech by tracking these 28 AI penny stocks shaping how businesses use artificial intelligence.

- Lock in income-focused ideas by reviewing these 11 dividend stocks with yields > 3% that offer yields above 3% as part of a diversified watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.