Allstate (ALL) Q4 Combined Ratio Of 80.1% Challenges Bearish Profitability Narratives

Allstate Corporation ALL | 0.00 |

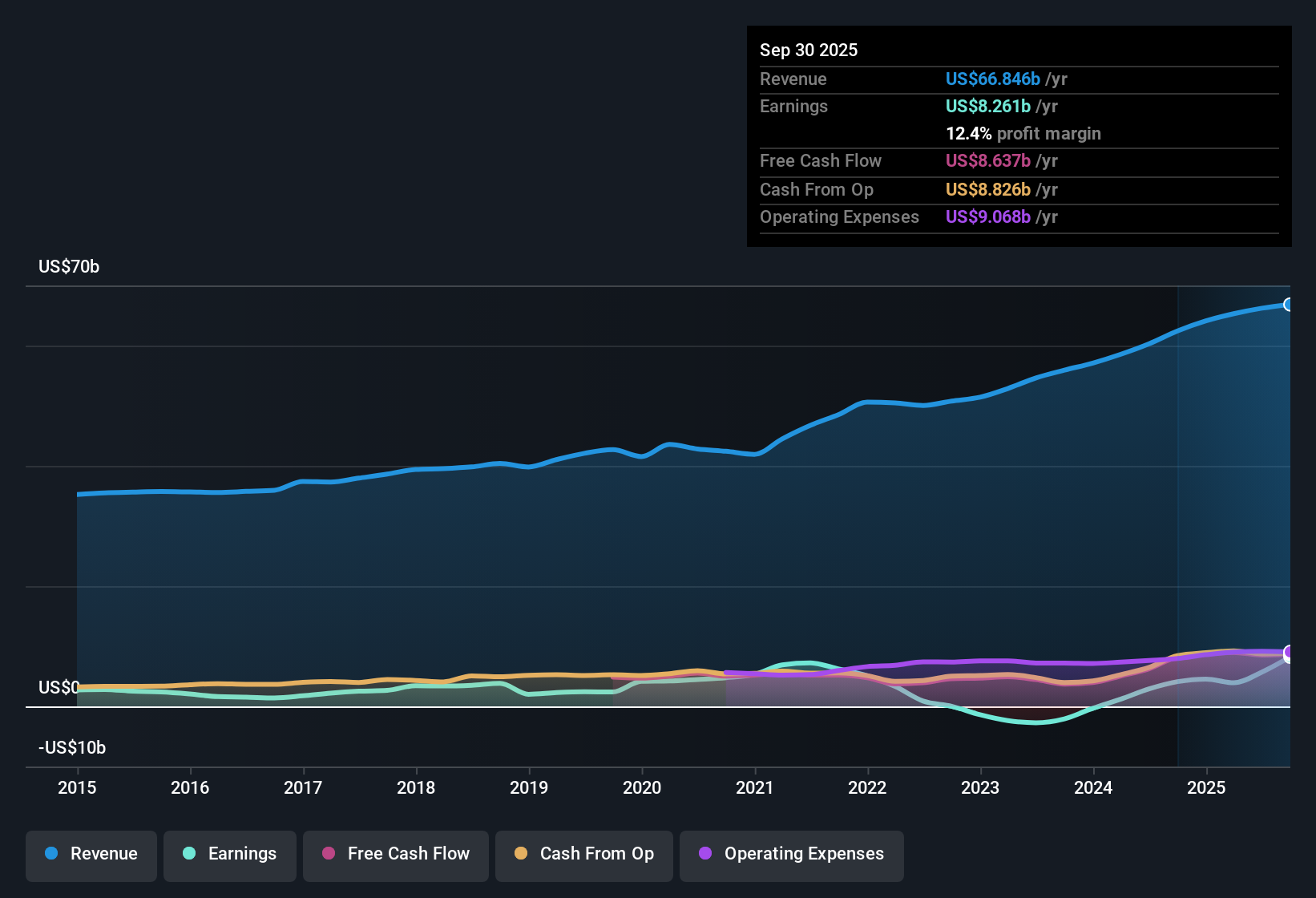

Allstate (ALL) just wrapped up FY 2025 with Q4 revenue of US$17.3b and basic EPS of US$14.55, capping off a trailing twelve month stretch where revenue reached US$67.7b and EPS came in at US$38.56 alongside year over year earnings growth of 123.4%. Over the past few quarters, the company has seen revenue move from US$16.5b and EPS of US$7.16 in Q4 2024 to US$16.6b and EPS of US$7.86 in Q2 2025, then to US$17.3b and EPS of US$14.55 in Q4 2025, setting up a story where stronger profitability and fatter margins are front and center for investors parsing this latest report.

See our full analysis for Allstate.With the headline numbers on the table, the next step is to see how these results line up with the dominant market narratives. This highlights where the story around growth, risk, and sustainability gets reinforced and where it might be challenged.

Margins Tighten Up, Combined Ratio Drops To 80.1%

- Allstate reported a combined ratio of 80.1% in Q3 2025, improving from 91.1% in Q2 2025 and 97.4% in Q1 2025, pointing to much stronger underwriting profitability through the year.

- What stands out for a bullish view is how this underwriting performance lines up with net income rising from US$566 million in Q1 2025 to US$3.7b in Q3 2025 and US$3.8b in Q4 2025. This heavily supports the idea that better loss and expense control has been a key driver of the 123.4% trailing earnings growth and the move in net margin to 15% from 7.1% a year earlier.

- Bulls who focus on earnings quality can point to the shift in quarterly net income from under US$1b early in FY 2025 to above US$3b in the second half as evidence that the improvement is not only large but also spread across multiple quarters.

- At the same time, the trailing twelve month data shows net income at US$10.2b on revenue of US$67.7b. Anyone leaning on the bullish angle needs to decide whether this margin level feels sustainable given how quickly the combined ratio moved over just a few quarters.

123.4% Earnings Growth Meets 31.2% Forecast Decline

- Over the last 12 months, earnings growth is reported at 123.4% with a trailing net margin of 15% compared with 7.1% a year earlier, while the same dataset shows analysts expecting earnings to fall by about 31.2% per year over the next three years.

- Critics highlight that this sharp contrast between very strong trailing profitability and an expected 31.2% annual decline creates a clear test for the bearish view, because it suggests the recent US$10.2b of trailing net income may not be repeated at the same level according to those forecasts.

- Bears can point to the forecast decline to argue that the recent jump in EPS to US$38.56 on a trailing basis might be closer to a high point than a new base, especially with revenue growth described at 4.3% per year compared with a 10.2% rate for the broader US market.

- On the other hand, the size of the 123.4% earnings increase over the last year gives investors a concrete counterpoint, and you as a reader have to weigh whether that strength or the projected decline feels more important when thinking about future profitability.

Strong trailing profitability paired with a sharp forecasted earnings drop is exactly the kind of tension long term holders watch closely, and it is a big part of how the wider market narrative around Allstate is taking shape right now. 📊 Read the full Allstate Consensus Narrative.

P/E Of 5.5x And DCF Fair Value Of US$611.50

- Allstate is shown trading on a trailing P/E of 5.5x compared with peer and industry averages of 12.1x and 12.9x, with a DCF fair value of US$611.50 per share and a current share price of US$215.19, alongside a 1.86% dividend yield.

- What is interesting for a bullish angle is that this combination of a lower P/E and a large gap to the DCF fair value sits next to forecasts calling for a 31.2% annual earnings decline. The low multiple and the flagged discount can be read either as a sign the market is overly cautious or as a sign that investors are already factoring in the weaker outlook.

- Supporters of the bullish case can highlight that recent trailing net income of US$10.2b and EPS of US$38.56 are being valued at a P/E less than half the peer and industry averages, which could appeal to value focused investors who are comfortable with slower revenue growth and the current 1.86% dividend yield.

- At the same time, the expected earnings decline means the low P/E does not automatically tell you the shares are inexpensive on a forward basis, so readers looking at the US$611.50 Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Allstate's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

The big tension here is that Allstate pairs very strong trailing earnings with forecasts calling for a 31.2% annual earnings decline and slower revenue growth than the broader US market.

If that mix of possible earnings pressure and cautious sentiment has you hesitating, take a look at our 55 high quality undervalued stocks that screens for companies where current pricing and fundamentals line up more comfortably with your expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.