American Tower (AMT) Stock May Be 40% Undervalued Following Hybrid IT Demand News

American Tower Corporation AMT | 0.00 |

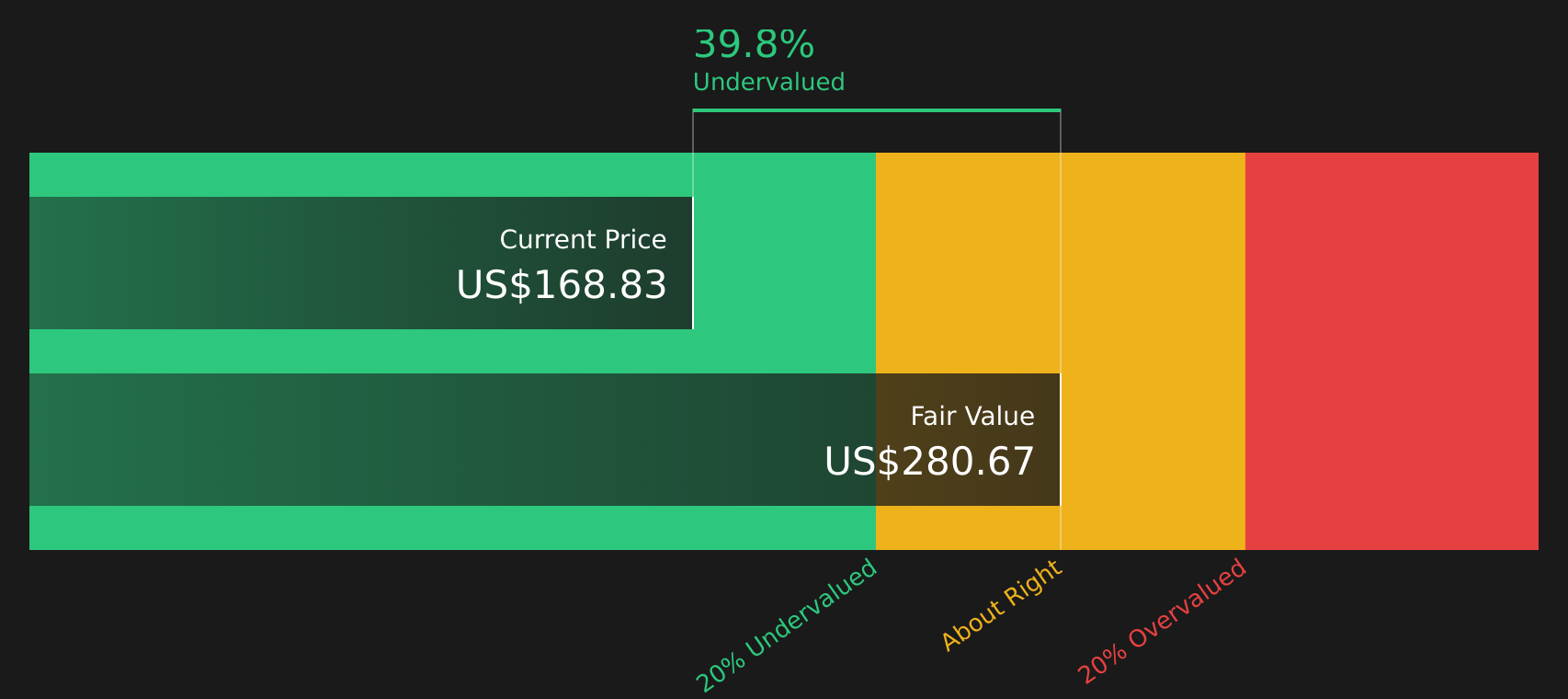

American Tower stock has fallen about 29.4% over the past five years. On current checks it screens as undervalued, with both an intrinsic value estimate based on a Discounted Cash Flow (DCF) approach and market multiples pointing to a discount relative to the current share price of US$169.50.

- The roughly 29.4% decline over five years puts the spotlight on whether the recent share price still reflects cautious sentiment rather than the company’s underlying cash flow potential.

- Growth expectations around American Tower’s tower and data center assets, including the recent focus on hybrid IT and AI workloads at CoreSite, can support valuation, while contract disputes and tenant churn, such as the resolved Echostar issue, highlight how revenue visibility risks may weigh on what investors are willing to pay.

- With a high value score of 6 out of 6, the broader set of valuation checks currently leans toward American Tower trading on the cheap side rather than at a premium.

The issue now is whether the gap between American Tower’s current price and an intrinsic value estimate that suggests roughly 39.5% undervaluation is wide enough to compensate investors for the risks around its tower and data center cash flows.

Is American Tower a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) model here is built on American Tower’s adjusted funds from operations and projected free cash flows. On the latest twelve month numbers, American Tower is generating about $5.0b in free cash flow, which the model treats as a base that is growing over time rather than shrinking.

Feeding those projections into the two stage DCF framework produces an estimated intrinsic value of about $280 per share, well above the recent share price of $169.50. This implies the stock screens around 39.5% undervalued on this cash flow view. Goldman Sachs highlighting American Tower’s growing data center exposure and international footprint helps explain why a cash flow based model can point higher than where the market is currently pricing the stock.

On this DCF view, American Tower stock currently looks undervalued relative to the cash flows it is modeled to produce.

Our Discounted Cash Flow (DCF) analysis suggests American Tower is undervalued by 39.5%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Does American Tower Look Undervalued on Earnings?

The P/E ratio fits American Tower well because earnings remain a key yardstick for how investors value established, cash generative REITs. On this metric, American Tower trades around 27.2x earnings, which is above the Specialized REITs sector average of about 16.3x, but below a peer group average of roughly 33.9x.

The modeled fair P/E ratio for American Tower is about 35.3x, which reflects what investors might be willing to pay given its business mix, risks and sector. That is higher than the current 27.2x. This suggests the stock is pricing in a discount relative to this tailored benchmark even though it already carries a premium to the broader industry.

On the P/E multiple, American Tower stock currently appears undervalued compared with the level implied by its own fundamentals and peer group.

The American Tower Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where this American Tower valuation puzzle leaves off by spelling out which assumptions about American Tower's future growth, margins and earnings would need to hold for the stock to be worth significantly more or less than today’s price on the Community page. Each narrative treats fair value as a thesis about the business that can be tracked over time, rather than a one off snapshot.

Share your own Narrative on American Tower to present a clear, number-driven case around its tower and data center exposure. Include a view on whether CoreSite's hybrid IT and AI workload positioning and the latest analyst calls really support the current share price. Add your voice to the Simply Wall St community and track how your thesis holds up as new results and data points emerge.

Do you think there's more to the story for American Tower? Head over to our Community to see what others are saying!

The Bottom Line

For American Tower, both the Discounted Cash Flow (DCF) estimate and the tailored P/E view currently indicate that the stock appears undervalued on cash flow and earnings multiples. The broader valuation checks also lean in the same direction, which shifts the focus away from price and toward how reliably tower and data center cash flows can support that intrinsic value estimate.

The key dividing line between more optimistic and more cautious views is whether contract risks, tenant churn, and execution around CoreSite and AI related workloads justify the current discount or eventually narrow it. Your assessment of that cash flow durability is what ultimately determines whether this gap is attractive or warranted.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.