Aon Stock Stands Out As Political Risk Puts US Financial Names In Focus

Moody's Corporation MCO | 0.00 |

Political risk is no longer just background noise for investors, it is starting to shape which stocks could face pressure and which might see fresh demand as trust in US legal and regulatory institutions comes under strain. With senior legal figures warning about retribution prosecutions and signs of stress inside the Department of Justice, companies closely tied to enforcement, oversight, and risk management are squarely in focus. This article breaks down three stocks exposed to the latest news: one where the backdrop could support its role as a risk partner and two where greater uncertainty may work against the business.

Moody's (MCO)

Overview: Moody's is a global risk assessment company that earns fees by rating debt issued by governments and corporations and by selling data, models, and software that help banks, insurers, and other institutions assess credit, regulatory, and counterparty risk.

Operations: Moody's generates about US$3.7b from Moody's Analytics and US$4.4b from Moody's Investors Service (before US$212m of eliminations), with revenue spread across the United States, EMEA, Asia Pacific, and the rest of the Americas.

Market Cap: US$81.8b

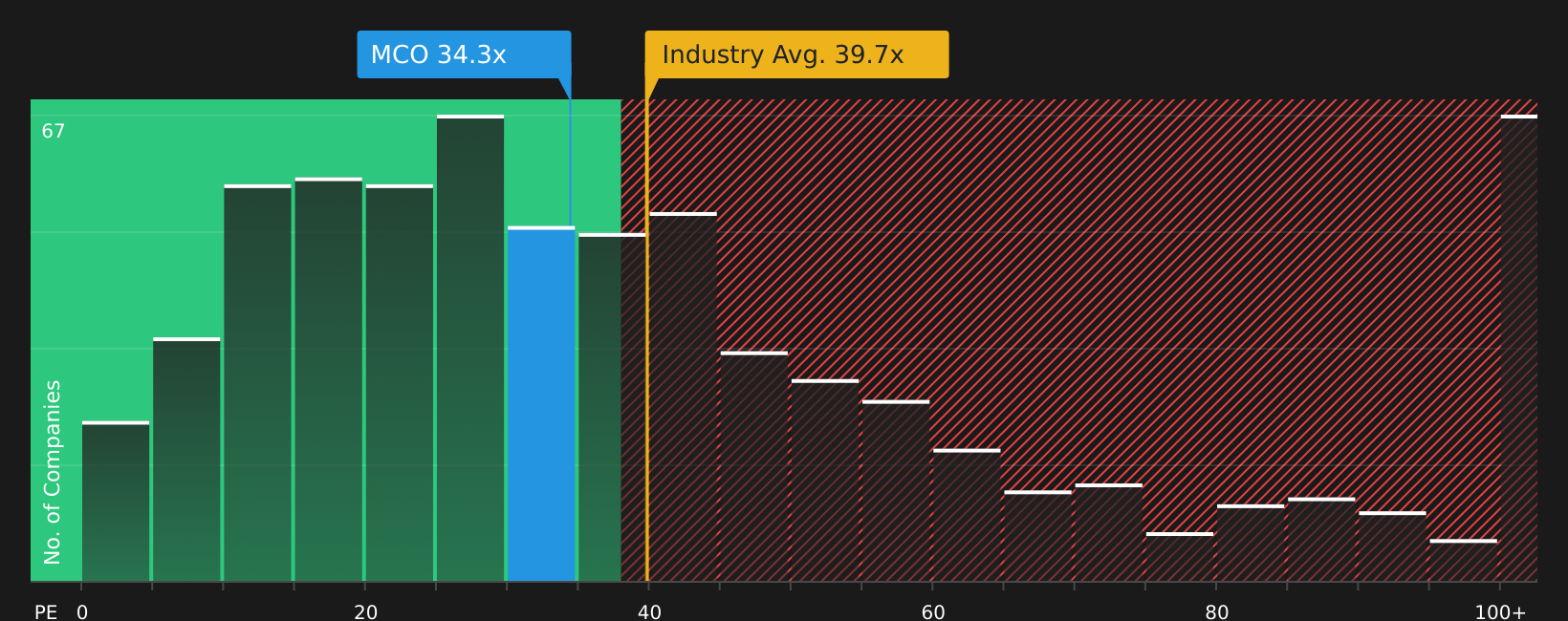

Moody's sits at the heart of global credit markets, but in a period of politicised justice and falling trust in US institutions, that position cuts both ways. The stock screens well on quality, with net margins above 30% and a long record of converting a capital light model into buybacks and dividends. At the same time, the business is tied to confidence in rule of law, clear regulation, and functioning debt markets, all of which look shakier as talk of retribution prosecutions grows. A P/E above 30 and heavy use of debt amplify the downside if issuance slows or regulators rethink how much power to give rating agencies. Investors weighing this mix of structural strength and rising political and financial risk have more to unpack before feeling comfortable here.

Moody's rich P/E and reliance on rule of law could be masking pressure points investors are underestimating, so it is worth reading the 3 key rewards and 1 important warning sign that may reveal where this story could abruptly turn

Aon (AON)

Overview: Aon is a global professional services firm that helps companies manage risk and people, from arranging insurance and reinsurance coverage to advising on employee benefits, retirement plans, and investment programs for corporations, public pensions, endowments, and foundations.

Operations: Aon generates about US$11.6b from its Risk Capital segment and US$5.9b from Human Capital, with the United States its largest market at US$8.3b of revenue, followed by Europe, the Middle East and Africa and the United Kingdom.

Market Cap: US$73.4b

Aon stands out as political and legal risk climbs because its core business is helping clients understand and transfer those risks through insurance, reinsurance, and advisory work. The company is leaning into this with its 3x3 Plan, AI enabled tools like Claims Copilot, and products tailored to areas such as data centers and transaction liability. Net margins of 22.5% point to solid earnings quality. At the same time, high debt and a P/E above the US Insurance average mean investors are paying for that quality and resilience, and performance has recently lagged the broader US market. For anyone weighing whether this mix of risk exposure and fee based earnings is worth the premium, there is more beneath the surface that deserves attention.

Aon's premium valuation and 22.5% net margins suggest something more is going on beneath the surface, so review the analysis report for Aon to see what the market might be missing about its risk engine.

Boeing (BA)

Overview: Boeing is a global aerospace and defense company that designs, builds, sells, and services commercial jetliners, military aircraft, satellites, missile defense systems, space launch and human spaceflight hardware, and a wide range of support services for airlines and governments worldwide.

Operations: Boeing generates about US$42.6b from Commercial Airplanes, US$28.5b from Defense, Space & Security, and US$21.2b from Global Services, with a heavy revenue tilt toward the United States at about US$48.9b.

Market Cap: US$172.3b

Boeing sits at the crossroads of government contracts, export controls, and global trade, which makes the current deterioration in rule of law and DOJ stability especially uncomfortable for investors. On one side, there is a record backlog, large China and defense deals, and a services business that could support cash flow if production problems ease. On the other side, there is a very high P/E, heavy debt, recent reliance on one off gains, and a commercial division that has not yet proven it can earn healthy margins again. If DOJ capacity weakens or enforcement becomes more unpredictable, export compliance, investigations, and contract security all become harder to value, leaving plenty for investors to consider beneath the surface.

Boeing's record backlog and heavy debt are pulling in opposite directions, and a very high P/E could be masking how fragile that balance is. Read the 3 key rewards and 2 important warning signs (1 is major!)

Take Control of Your Investment Journey

If Moody's or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd?

Fresh ideas can move fast, and some of the most interesting stories may still be flying under the radar. Review these focused stock lists before momentum shifts further.

- Target resilient paychecks by reviewing 7 dividend fortresses that aim to keep income flowing even when markets cool, so your portfolio continues working while others are still reacting.

- Spot early infrastructure activity by using 35 power grid technology and infrastructure stocks to review companies tied to grid upgrades and electrification trends before they become more widely recognized.

- Explore long term materials demand through 8 top copper producer stocks highlighting producers involved in wiring, vehicles, and energy projects while pricing dislocations may still offer potential entry points.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.