Arbor Realty Trust (ABR) After Its Note Deal Faces A Fresh Valuation Test

Arbor Realty Trust Inc ABR | 0.00 |

Arbor Realty Trust (ABR) has just completed a private offering of US$325 million in 6.25% Convertible Senior Notes due 2029, a funding move that immediately reshaped how the stock is being discussed.

Arbor Realty Trust's recent capital moves come after a tough stretch for the stock. The latest share price is US$5.36, with a 7 day share price return of 5.30%, but a year to date share price return down 32.58% and a 1 year total shareholder return down 45.13%. This suggests recent momentum has picked up slightly while longer term performance has been weak as the market reassesses risk around its real estate credit exposure.

If this kind of repricing has you looking beyond a single real estate lender, it could be a good moment to widen your search and check out 20 top founder-led companies

With Arbor Realty Trust trading at US$5.36 and the new notes carrying an initial conversion price around US$6.10, the key question now is simple: is this reset creating a mispriced opportunity, or is the market already factoring in any future recovery?

Preferred P/E of 13.3x: Is It Justified for Arbor Realty Trust?

The latest data suggests Arbor Realty Trust is trading on a P/E of 13.3x, which looks slightly expensive both against peers and its own estimated fair ratio.

The P/E ratio compares the current share price to earnings per share and is a common way to see how much investors are paying for each dollar of profit. For a mortgage REIT like Arbor Realty Trust, it can hint at how the market is weighing earnings power against risks in the lending book and funding structure.

On one hand, Arbor Realty Trust is described as good value when compared to a peer average P/E of 15x, which suggests the market is not assigning a premium relative to similar stocks. On the other hand, that same 13.3x multiple is higher than both the US Mortgage REITs industry average of 11.7x and the estimated fair P/E ratio of 12.7x, so the market is paying more than both the sector benchmark and the level the SWS fair ratio points to as a potential equilibrium.

For investors, that spread means the stock is cheaper than some direct peers but richer than the broader industry and the modelled fair P/E, which may limit how far valuation could stretch if expectations stay the same. Explore the SWS fair ratio for Arbor Realty Trust

Result: Price-to-earnings of 13.3x (OVERVALUED)

However, Arbor Realty Trust still faces clear risks, including annual revenue declining about 49% and multiyear total returns down sharply, which could pressure sentiment further.

Another View on Arbor Realty Trust: What the DCF Says

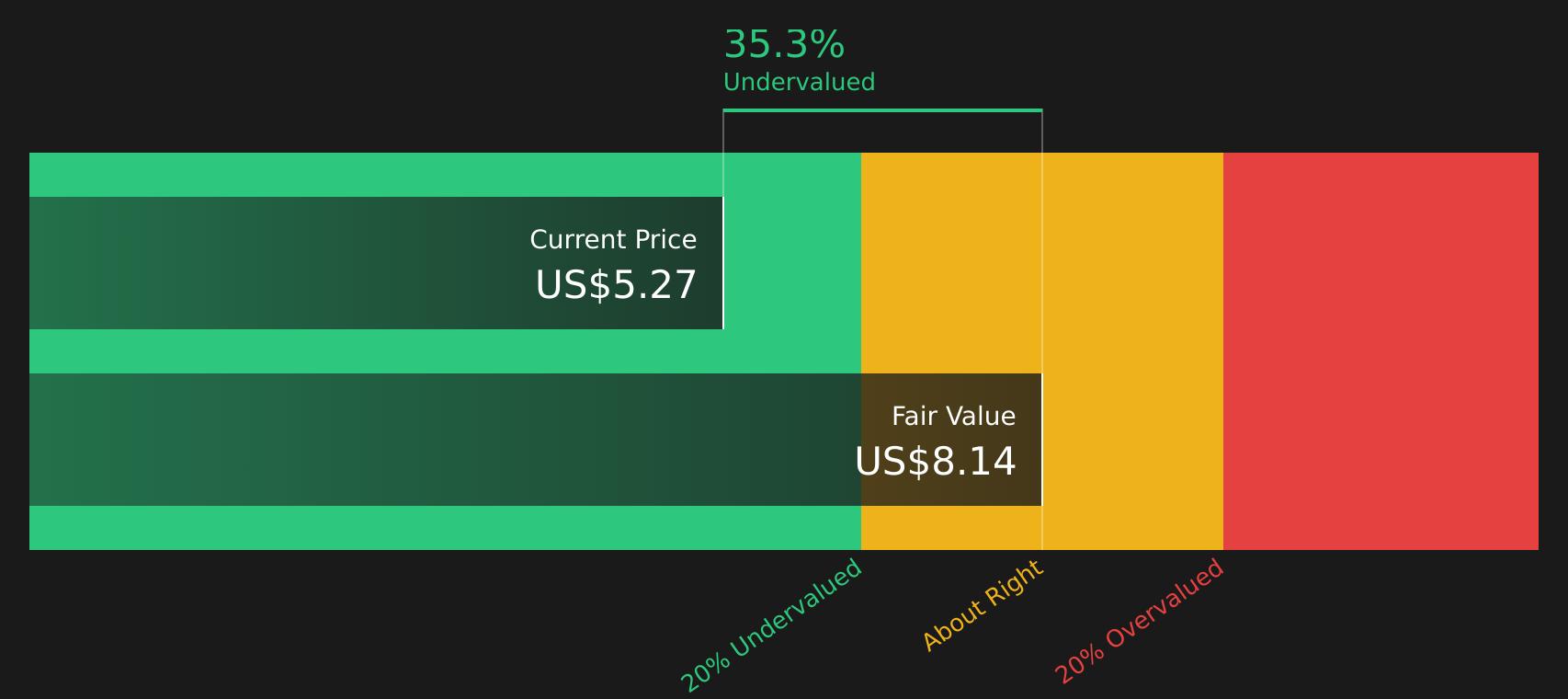

While the P/E of 13.3x suggests Arbor Realty Trust is slightly expensive relative to its fair ratio and industry, the SWS DCF model points the other way, with an estimated future cash flow value of US$8.07 versus the current US$5.36 share price. This implies the stock trades below that cash flow based value. Which lens do you trust more when cash flows and earnings are telling different stories?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Arbor Realty Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of concerns and potential upside around Arbor Realty Trust leaves you undecided, act while the data is fresh and weigh both sides with the 2 key rewards and 4 important warning signs.

Looking for more investment ideas beyond Arbor Realty Trust?

Do not stop with Arbor Realty Trust. Use fresh data to spot other opportunities now, before the next round of market moves leaves you reacting instead of prepared.

- Target potential upside in companies the market may have overlooked by scanning the screener containing 19 high quality undiscovered gems.

- Prioritize stability first and seek out businesses with more resilient profiles through the 73 resilient stocks with low risk scores.

- Focus on financial strength and filter for companies with healthier funding and asset backing using the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.