Arbor Realty Trust (ABR) Valuation Check As Dividend Cut And Weaker Earnings Signal A Slower Recovery

Arbor Realty Trust Inc ABR | 0.00 |

Arbor Realty Trust (ABR) is back in focus after first quarter 2026 results showed net income at US$10.97 million versus US$40.78 million a year earlier, along with another reset of its quarterly dividend to US$0.17 per share.

The latest earnings and dividend reset appear to have weighed on sentiment, with the stock’s 7 day share price return down 29.07% and its 1 year total shareholder return down 38.42%. This suggests momentum has been fading as unresolved multifamily loans and real estate owned continue to cloud the recovery story.

If this kind of pressure on a real estate focused lender has you thinking about where growth might be more durable, it could be worth scanning companies linked to the infrastructure behind new technologies such as 37 power grid technology and infrastructure stocks

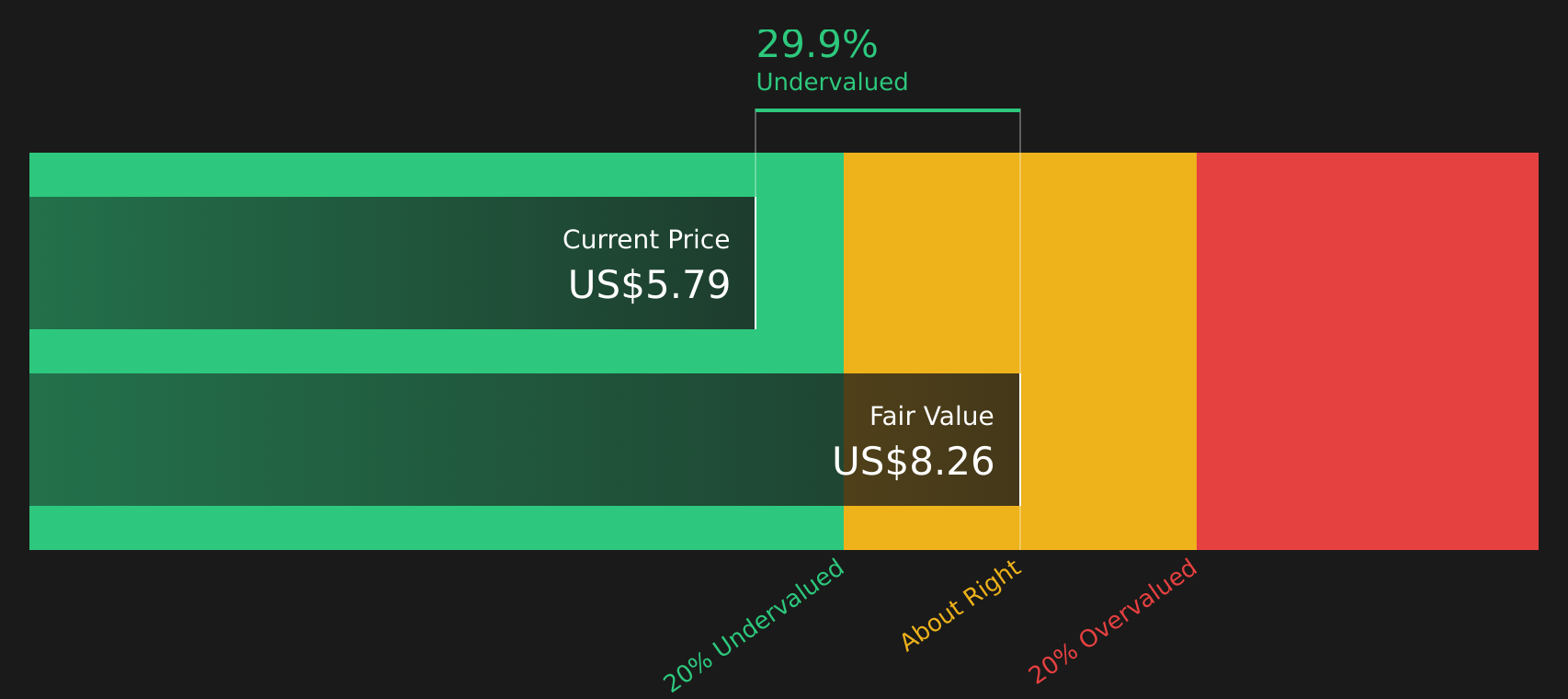

With the stock down sharply over the past year, trading at US$5.88 and at a sizable discount to some analyst and intrinsic value estimates, is Arbor Realty Trust now undervalued, or is the market already pricing in any future recovery?

Preferred P/E of 14.6x: Is it justified?

On traditional valuation metrics, Arbor Realty Trust trades on a P/E of 14.6x, which sits between its own fair ratio estimate and the wider Mortgage REITs peer group.

The P/E ratio compares the current share price with earnings per share, so it reflects what investors are currently paying for each dollar of earnings. For a real estate focused lender like Arbor, this is one way the market weighs up the earnings profile against sector specific risks such as funding mix and credit quality.

Arbor’s 14.6x P/E is higher than the US Mortgage REITs industry average of 12.3x, so the market is assigning a richer earnings tag than the typical sector peer. However, it is below the peer average of 19x and below the estimated fair P/E of 16.1x. This suggests some room for the valuation to move closer to that fair ratio level if earnings forecasts and sentiment remain supportive.

Result: Price-to-earnings of 14.6x (ABOUT RIGHT)

However, still keep an eye on the pressure from unresolved multifamily loans and real estate owned, along with the recent dividend reset, which may keep sentiment fragile.

Another view on value: what does cash flow say?

The earnings based P/E story is only one angle. Our DCF model values Arbor at $9.20 per share, compared with the current $5.88 price, which points to the stock trading at a 36.1% discount. That is a very different message from a P/E that looks only “about right.”

For investors, this kind of gap can either flag a margin of safety if the cash flow assumptions hold up, or a value trap if loan quality and funding risks erode those cash flows. The key question is which story you trust more: the earnings multiple or the cash flow math.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Arbor Realty Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mixed signals here, with pressure on earnings alongside potential value, make sentiment tricky to read. It makes sense to move quickly and review the underlying data yourself. To weigh both the downside and upside potential in one place, start with the 3 key rewards and 4 important warning signs.

Looking for more investment ideas?

If Arbor Realty Trust has you reassessing where you put fresh capital, now is the moment to widen your watchlist before the next round of opportunities moves on.

- Spot potential value opportunities early by scanning companies trading below what their fundamentals might justify through the 47 high quality undervalued stocks.

- Prioritize resilience by focusing on companies with healthy finances using the solid balance sheet and fundamentals stocks screener (45 results).

- Turn income goals into a concrete watchlist by checking out stocks in the 14 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.