Aritzia Stock Leads 3 Cash Rich Picks Trading Below Fair Value

FTAI Aviation Ltd. FTAI | 0.00 |

With inflation signals mixed across regions, central banks weighing their next moves and earnings season set to test profit resilience, many investors are focusing on what companies are doing with real cash rather than headlines. The Undervalued Stocks Based On Cash Flows screener highlights companies where discounted cash flow estimates from SWS suggest the current share price is below fair value. That combination of cash flow potential and a discount can be attractive for value oriented investors looking for ideas across sectors. This article highlights 3 stocks from the screener that stand out for further research.

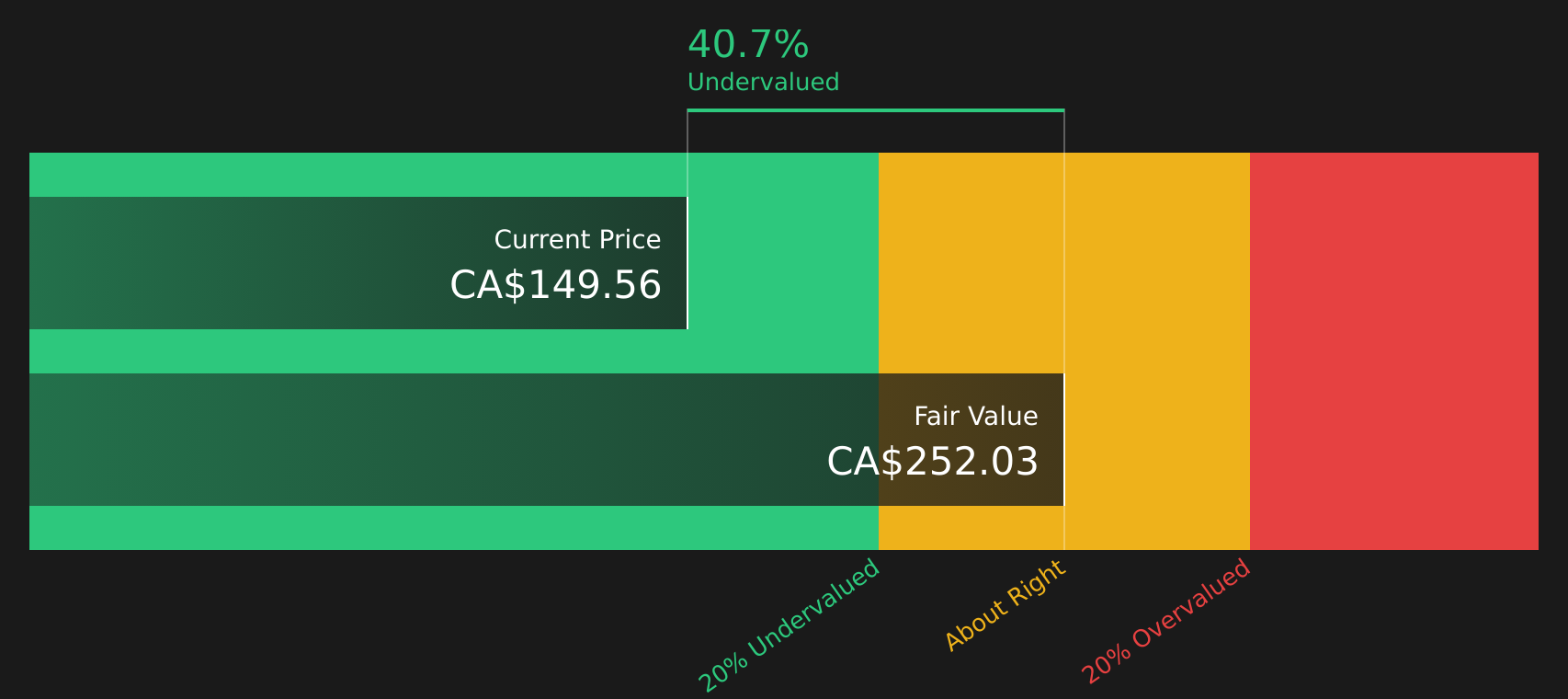

Aritzia (TSX:ATZ)

Overview: Aritzia is a Vancouver based fashion retailer that designs and sells its own portfolio of womenswear and accessories brands through boutiques and online channels in Canada and the United States.

Operations: Aritzia generates about CA$4.0b in revenue, primarily from apparel, with around CA$2.5b from the United States and CA$1.5b from Canada.

Market Cap: CA$18.3b

Aritzia is attracting attention because it combines rapid earnings growth with an expansion story that is still playing out, particularly in the U.S., where revenue recently accounted for roughly two thirds of the business and digital sales are gaining traction. Forecast earnings growth of around 20.3% per year, expanding margins and very high recent ROE are described in relation to a valuation that sits well below the Simply Wall St cash flow estimate, which may appeal to value focused investors. At the same time, heavy investment in marketing, new boutiques and distribution capacity increases execution risk, especially if U.S. consumer demand softens or new stores underperform. Along with insider selling and higher executive pay, these factors make Aritzia a growth story that may warrant closer scrutiny rather than unquestioned enthusiasm.

Aritzia’s rapid earnings story and U.S. expansion can look compelling, but the real tension is how that growth stacks up against execution risk and valuation, so it is worth reviewing the analyst forecasts for Aritzia

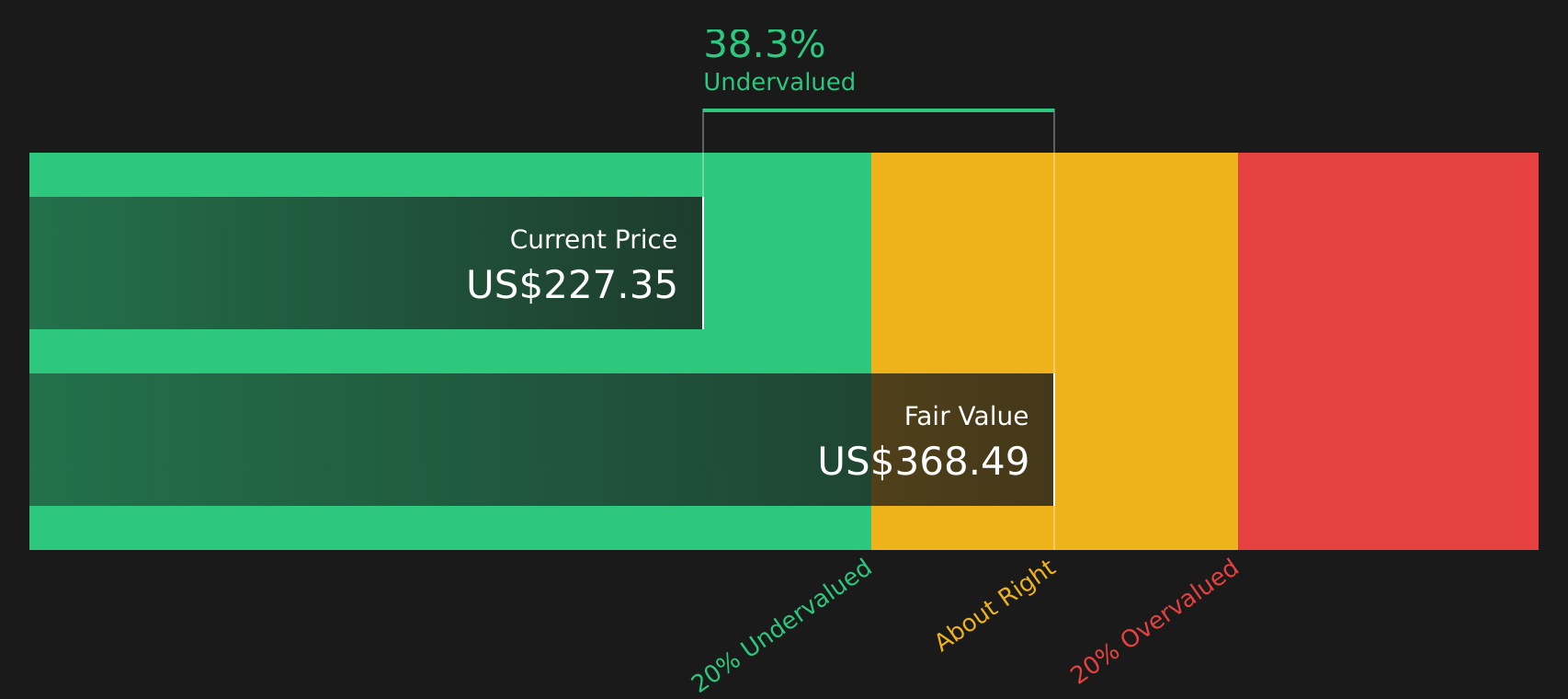

FTAI Aviation (FTAI)

Overview: FTAI Aviation is a New York based company that owns, leases, and trades aircraft and engines while also providing maintenance, repair, and aftermarket parts that keep commercial fleets in service for airlines around the world.

Operations: FTAI Aviation generates about US$2.8b in revenue, with roughly US$2.3b from Aerospace Products and US$0.5b from Aviation Leasing.

Market Cap: US$23.3b

FTAI Aviation stands out because it sits at the heart of a tight aviation supply chain, supplying engine leasing and mid life maintenance programs as airlines keep older 737NG and A320ceo aircraft flying longer and face delays on new jets. The company’s engine focused model, long term collaboration with Aeronautical Engineers on freighter conversions, strong free cash flow and a rising dividend point to a business built around recurring service income rather than one off aircraft trades. At the same time, high leverage, dependence on legacy engine platforms and ambitious expansion plans introduce real execution and funding risk. This makes the current gap to cash flow based fair value estimates something investors may want to examine more closely.

FTAI Aviation’s engine centric cash flows and rising dividend suggest a potential opportunity that investors may be underpricing right now, but the real twist sits inside the 4 key rewards and 3 important warning signs (2 are major!)

Tenable Holdings (TENB)

Overview: Tenable Holdings provides cyber exposure management software that helps organisations identify, measure and reduce security risks across IT networks, cloud environments, identities, operational technology and AI related systems.

Operations: Tenable Holdings generates about US$1.0b in revenue from security software and services, with around US$539.2m from the United States, US$283.8m from Europe, the Middle East and Africa, US$118.6m from Asia Pacific and US$80.7m from the rest of the Americas.

Market Cap: US$4.4b

Tenable Holdings sits at the centre of rising demand for exposure management, with earnings forecast to grow 87.32% per year and the business expected to move into profit over the next 3 years as customers consolidate spending onto platforms such as Tenable One and its AI Exposure solutions. The stock trades below Simply Wall St’s cash flow based estimate of fair value, even as analysts highlight AI driven cybersecurity spending, larger deal sizes and stronger recurring revenue as key drivers. However, Tenable is still loss making today, leans on higher risk external funding and faces intense competition from large platform vendors. That mix of rapid forecast improvement, valuation gap and real execution risk is what makes the full Tenable Holdings story worth examining in more detail.

Accelerating forecast earnings and a move toward profitability put Tenable Holdings in rare territory, but the real story sits inside the analyst forecasts for Tenable Holdings, including one expectation shift that could change how you view the stock.

The three stocks covered here are just a sample of the idea, and the full Undervalued Stocks Based On Cash Flows screen on Simply Wall St currently flags 693 more companies that combine discounted cash flow valuations with stories that could be just as compelling as Aritzia, FTAI Aviation and Tenable Holdings. You can unlock a broader opportunity set by using the Undervalued Stocks Based On Cash Flows screener to identify and analyze the specific cash flow catalysts, balance sheet profiles and risk reward narratives that align with your highest conviction ideas.

Take Control of Your Investment Journey

If Tenable Holdings or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Do

Fresh opportunities do not stay under the radar for long, and the next breakout stocks often build momentum quietly while attention is elsewhere. Scan these ideas now to explore them at an earlier stage.

- Identify steady compounders before they gain wider attention by focusing on companies with resilient finances inside the list of solid balance sheet and fundamentals (12 results).

- Explore structural shifts in computing by scanning the 26 quantum computing stocks curated for businesses positioned around quantum hardware, software and infrastructure while it still feels early.

- Review income opportunities that are not yet widely followed through the 6 dividend fortresses built around higher yielding companies that aim to keep investors focused on cash returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.