Arrow Electronics (ARW) Is Up 8.2% After U.S. Lifts Trade Restrictions on China, Hong Kong Units

Arrow Electronics, Inc. ARW | 143.41 | +5.22% |

- Arrow Electronics recently announced that the U.S. government is reversing previously imposed trade restrictions on its China-based subsidiaries and Hong Kong affiliates, following concerns about the sale of U.S. components found in weaponized drones operated by Iran-backed groups.

- This regulatory decision allows Arrow's affiliates to resume transactions, directly impacting the company's ability to operate globally and improving its standing with U.S. authorities.

- We'll examine how the lifting of these U.S. trade restrictions may affect Arrow Electronics' operational outlook and future growth prospects.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Arrow Electronics Investment Narrative Recap

To be a shareholder in Arrow Electronics, an investor needs to believe in the company's capacity to benefit from global growth in electronics content and its exposure to recurring, higher-margin segments like cloud and cybersecurity. The reversal of U.S. trade restrictions is a positive step for Arrow’s global operations but does not materially change the most important near-term catalyst: broad-based backlog growth and recovery in mass-market segments. The largest risk remains the potential for digitalization trends to enable direct sourcing, threatening core revenue streams and market share.

Among recent announcements, Arrow's partnership with CrowdStrike to distribute advanced AI-native cybersecurity solutions stands out. This move aligns with the key catalyst of expanding into higher-margin, recurring revenue streams, representing efforts to enhance long-term earnings resilience despite ongoing industry volatility.

However, investors should also recognize risks arising from supply chain automation and digital platforms potentially disintermediating traditional distribution, details about this risk are essential for anyone considering Arrow Electronics...

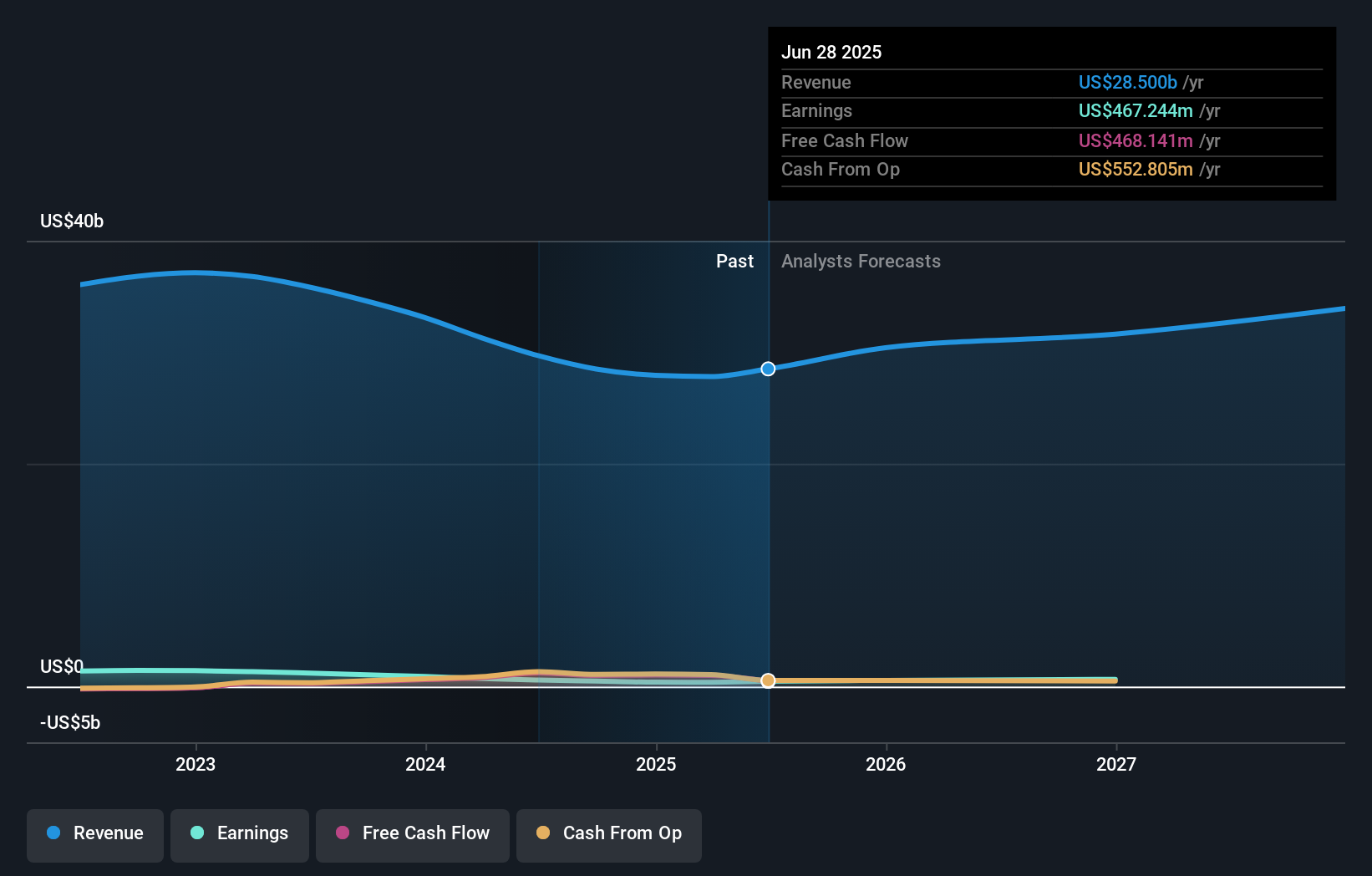

Arrow Electronics is forecasted to reach $35.2 billion in revenue and $734.1 million in earnings by 2028. This projection assumes a 7.3% annual revenue growth rate and a $266.9 million increase in earnings from the current $467.2 million.

Uncover how Arrow Electronics' forecasts yield a $116.75 fair value, a 7% downside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community members currently estimate Arrow’s fair value at US$116.75, with no variation in projections. In contrast, evolving supply chain technology and digital procurement may ultimately reshape the company's revenue model and wider market dynamics, explore multiple viewpoints to better understand your own outlook.

Explore 2 other fair value estimates on Arrow Electronics - why the stock might be worth 7% less than the current price!

Build Your Own Arrow Electronics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Arrow Electronics research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Arrow Electronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arrow Electronics' overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.