Arthur J. Gallagher (AJG) Margin Compression Tests Bullish Growth And Premium Valuation Narratives

Arthur J. Gallagher & Co. AJG | 217.61 | +0.59% |

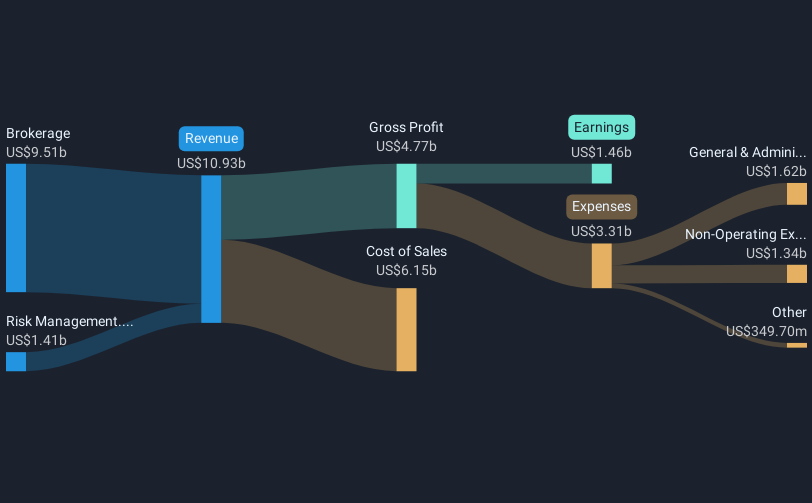

Arthur J. Gallagher (AJG) has wrapped up FY 2025 with fourth quarter revenue of US$3.6b and basic EPS of US$0.58, alongside net income of US$151m. This puts the spotlight on how this year’s figures line up against recent history. The company has seen quarterly revenue move from US$2.5b and basic EPS of US$1.14 in Q4 2024 to US$3.6b and US$0.58 in Q4 2025. Trailing twelve month revenue came in at US$13.9b with basic EPS of US$5.74. With trailing net profit margins at 10.7% versus 13.4% a year earlier, investors are likely to focus on how the latest results balance solid top line scale with some margin compression.

See our full analysis for Arthur J. Gallagher.With the headline numbers on the table, the next step is to see how this earnings print lines up against the widely followed growth and valuation narratives that have built up around the stock.

TTM earnings slow to 2.1% growth

- Over the last 12 months, earnings growth came in at 2.1%, compared with a 5 year earnings growth rate of 12.7% per year.

- For a more bullish view, what stands out is that this slower 2.1% earnings growth sits alongside trailing twelve month net income of US$1.5b and Basic EPS of US$5.74. These still reflect a sizeable profit base. However, the recent moderation means investors who expect a smooth compounding path need to reconcile that shorter term figure with the stronger 5 year average.

P/E of 42.9x versus 13.1x industry

- AJG trades on a P/E of 42.9x, compared with a US Insurance industry average of 13.1x and a peer average of 21.7x.

- Critics highlight this higher 42.9x multiple as a key concern, and the data gives them points on both sides.

- On one side, earnings are forecast to grow about 20.7% per year and revenue about 12.9% per year, which is faster than the US market forecasts of 16.1% earnings growth and 10.6% revenue growth.

- On the other, the one year earnings growth rate of 2.1% compared with the 12.7% per year five year trend shows that the most recent year has not matched that longer term pace, even though the market is valuing the company well above the sector on P/E.

DCF fair value sits at US$349.38 vs US$249.37 price

- The current share price of US$249.37 is about 28.6% below a DCF fair value estimate of US$349.38.

- For a generally bullish angle, it is notable that this DCF indication of upside sits next to a flagged balance sheet risk.

- Rewards include expected earnings growth of about 20.7% per year and five year earnings growth of 12.7% per year, alongside trailing twelve month revenue of US$13.9b and net income of US$1.5b.

- At the same time, a key risk is that debt is not well covered by operating cash flow over the last 12 months, and there has been insider selling over the past three months, so the growth and valuation story is paired with a need to watch cash generation and leverage.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Arthur J. Gallagher's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

AJG pairs a relatively rich 42.9x P/E and slower 2.1% earnings growth with a balance sheet where debt coverage by operating cash flow and recent insider selling are flagged as concerns.

If that mix of higher valuation, softer recent earnings momentum, and balance sheet flags gives you pause, check out solid balance sheet and fundamentals stocks screener (391 results) to focus on companies built on sturdier cash generation and lower financial strain.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.