Assessing Alaska Air Group’s Valuation As Investors Position For Potential Earnings Surprise

Alaska Air Group, Inc. ALK | 0.00 |

Alaska Air Group (ALK) is drawing attention ahead of its next earnings release, with forecasts pointing to an earnings per share loss of $0.87 and revenue of $4.1 billion.

Investors appear to be positioning ahead of earnings, with Alaska Air Group’s share price up 19.38% over the past month and 11.32% over the past week, even though the year to date share price return is down 10.68% and the 1 year total shareholder return is down 9.64%. This suggests short term momentum has picked up while the longer term picture remains weak.

If you are weighing Alaska Air Group’s recent move and want more ideas in transportation and infrastructure, it could be a good moment to check out 33 power grid technology and infrastructure stocks

With Alaska Air Group expected to post an earnings loss alongside higher forecast revenue, and the stock trading below the average analyst price target, you have to ask: is there real value left here, or is the market already pricing in future growth?

Most Popular Narrative: 29.7% Undervalued

At a last close of $46.02 versus a narrative fair value of $65.47, Alaska Air Group screens as materially discounted, with that gap resting on some punchy long term assumptions.

The expansion and optimization of the Seattle international gateway, including new long-haul routes and a growing fleet of Boeing 787s, positions Alaska Air Group to benefit from sustained urban growth and increasing travel demand in West Coast cities, anticipated to drive higher passenger volumes and top-line revenue growth.

Want to see what is baked into that valuation gap? Revenue stepping up, margins rebuilding, and a future earnings profile that assumes real operating leverage. The full narrative lays out the numbers.

Result: Fair Value of $65.47 (UNDERVALUED)

However, higher unit costs and the execution risk around integrating Hawaiian Airlines could quickly erode the margin rebuild that supports this upside story.

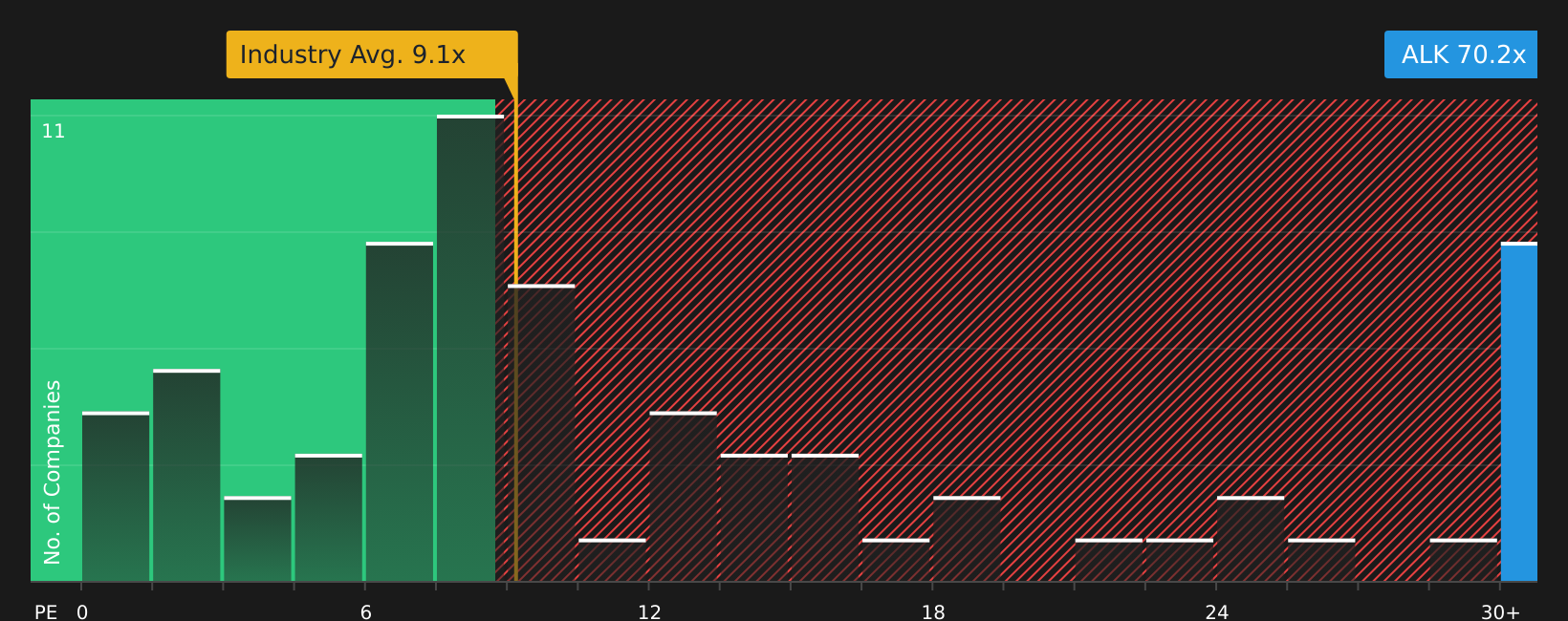

Another View: Earnings Multiple Tells a Different Story

The narrative fair value and DCF style work suggest upside, but the current P/E of 70.2x is far above the global airlines average of 9.1x and the peer average of 17.8x, even though the fair ratio is 87x. That gap points to meaningful valuation risk if sentiment cools. Which signal do you trust more right now?

Next Steps

The mix of optimism and concern around Alaska Air Group is clear, so check the data now and shape your own view with 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If Alaska Air Group has you thinking harder about your portfolio, do not stop here. The right watchlist today could shape your next big decision tomorrow.

- Target stability with companies that show resilient fundamentals and lower risk scores by checking out the 62 resilient stocks with low risk scores.

- Hunt for potential bargains with strong balance sheets and cash generation by scanning the 46 high quality undervalued stocks.

- Spot lesser-known opportunities with solid financial foundations by reviewing the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.