Assessing Align Technology (ALGN) After Years Of Share Price Declines And DCF Upside Potential

Align Technology, Inc. ALGN | 0.00 |

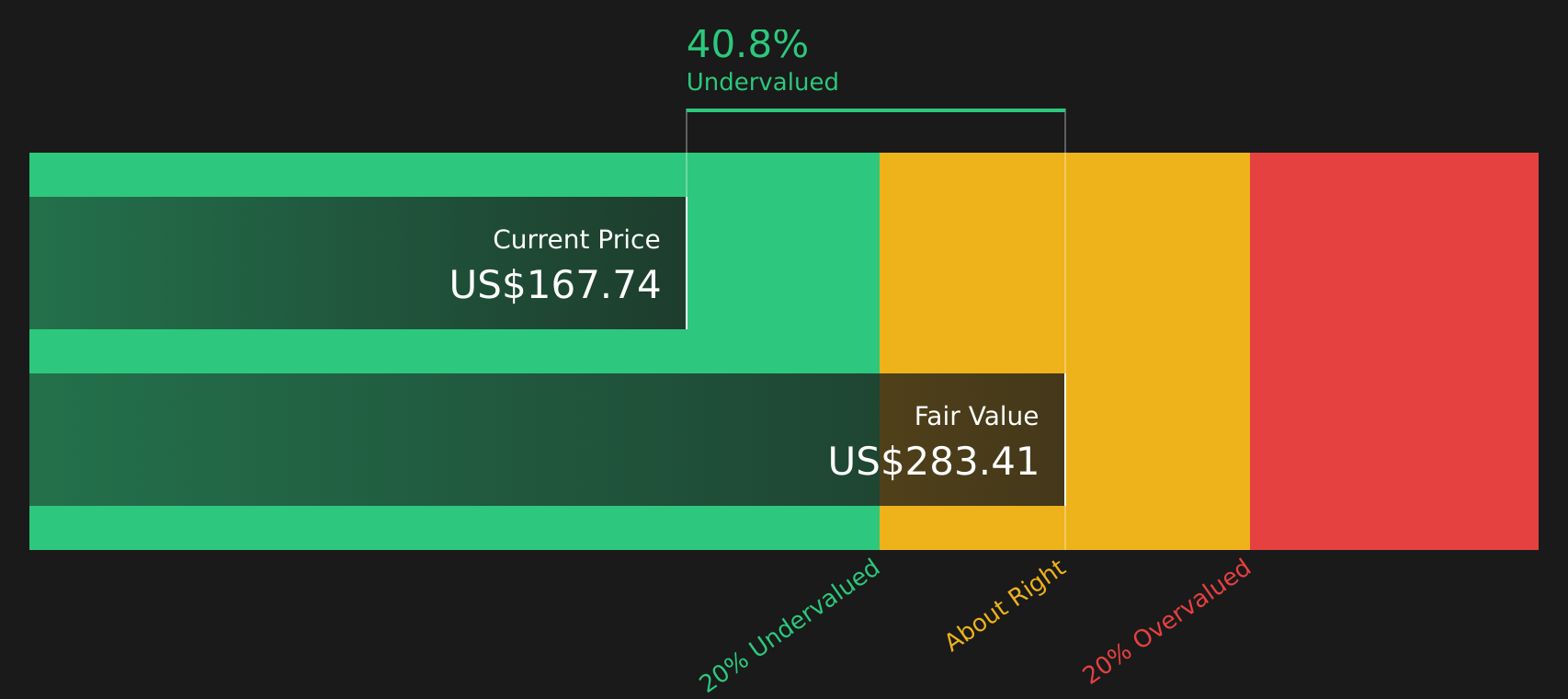

Before deciding whether Align Technology stock looks attractive or not, you probably want to know if the current price around US$167.74 fairly reflects what the business might be worth.

Over the short term, the stock has been under pressure, with the share price down 4.1% over the last week and 3.6% over the last month, although it is up 7.5% year to date. The one year and three year returns show declines of 7.1% and 44.9% respectively, with a 72.6% decline over five years.

Recent news coverage has focused on Align Technology's positioning in clear aligners and digital orthodontics, as investors weigh how demand trends and competitive pressures could affect future cash flows and sentiment around the stock. Broader coverage has also highlighted how medical equipment stocks with growth stories can see sharp valuation swings when expectations change. This provides useful context for the share price moves seen here.

Simply Wall St gives Align Technology a valuation score of 5 out of 6, which suggests the stock screens as undervalued on most of its checks. The next sections will break down what different valuation methods say about that, before finishing with a way to assess value that goes beyond any single model.

Approach 1: Align Technology Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of the cash a company could generate in the future and discounts those amounts back to today, giving a single estimate of what the business might be worth right now.

For Align Technology, the latest twelve month Free Cash Flow is about $567.8 million. Using a 2 Stage Free Cash Flow to Equity model, analysts and Simply Wall St project future cash flows, with forecast Free Cash Flow of $931.9 million in 2030. Estimates out to 2030 are based on analyst inputs for earlier years and are then extrapolated by Simply Wall St.

On this DCF setup, the estimated intrinsic value for the stock comes out at about $283.38 per share. Compared with the current share price around $167.74, the model implies the stock trades at a 40.8% discount to this intrinsic value. This indicates a notable gap between the current price and this cash flow based estimate of worth.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Align Technology is undervalued by 40.8%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Approach 2: Align Technology Price vs Earnings

For profitable companies, the P/E ratio is a useful way to relate what you pay for the stock to the earnings the business is currently generating. Investors usually accept a higher or lower P/E depending on how they see the trade off between future growth potential and the risks around those earnings.

Align Technology currently trades on a P/E of 27.94x. That sits above the broader Medical Equipment industry average P/E of 25.29x and slightly below the peer group average of 29.16x. On the surface, this points to the stock being priced somewhere between the wider industry and closer peers that investors group it with.

Simply Wall St's Fair Ratio for Align Technology is 29.08x, which is its estimate of a suitable P/E once factors like earnings growth, profit margins, industry, market cap and specific risks are taken into account. This tailored measure is more informative than a simple comparison with industry or peers because it adjusts the benchmark to the company’s own profile. With the actual P/E of 27.94x sitting a little below the Fair Ratio of 29.08x, the stock screens as slightly undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 21 top founder-led companies.

Upgrade Your Decision Making: Choose your Align Technology Narrative

Earlier it was mentioned that there is an even better way to think about valuation, and that is where Narratives come in, giving you a clear story behind the numbers you see for a company like Align Technology.

A Narrative on Simply Wall St is your view of the business written as a story that ties together your assumptions about future revenue, earnings and margins with the fair value you think is reasonable.

Instead of looking at a single DCF or P/E number in isolation, a Narrative connects three pieces in one place: how you think the business will evolve, what that means for its future financials, and the fair value that follows from those assumptions.

Narratives sit inside the Simply Wall St Community page, where millions of investors can see different storylines on the same stock using an accessible, guided format rather than complex models.

Each Narrative then helps you decide what action might make sense for you by comparing the Fair Value from that story to the current share price, so you can see whether your view sits closer to a hold, buy or sell mindset.

Because Narratives update when new earnings, news or guidance arrive, your fair value view is not static; it is refreshed as the facts change and your story does too.

For Align, one investor might build a more cautious Narrative aligned with a Fair Value around US$175.00, while another leans into a more optimistic Narrative closer to US$240.00. Seeing both side by side can make it easier for you to decide which story you find more reasonable.

For Align Technology however we will make it really easy for you with previews of two leading Align Technology Narratives:

Narrative fair value: US$201.69

Implied discount vs current price: about 16.8% below this fair value

Analyst revenue growth assumption: 4.94% a year

- Analysts see expansion into new clinical segments and wider international use of Invisalign and digital tools as key supports for future revenue and earnings.

- Model assumptions include revenue growth of 4.94% a year, profit margins rising from 10.2% to 15.6%, and earnings reaching US$726.5m by around April 2029.

- The narrative ties these assumptions to a fair value of about US$201.69 a share, with a future P/E of 23.29x and a discount rate of 7.77%.

Narrative fair value: US$154.62

Implied premium vs current price: about 8.5% above this fair value

Revenue growth assumption: 4.80% a year

- This narrative focuses on cost conscious patients, rising competition and pressure on clear aligner pricing as tests of Align Technology's premium positioning.

- It highlights that while Invisalign and the digital ecosystem support brand strength and practitioner loyalty, margins can still come under pressure when marketing, R&D and manufacturing costs rise.

- The story frames Align Technology as a premium orthodontics business in a more price sensitive world, with a fair value of about US$154.62 a share and revenue growth assumptions of 4.80% a year.

If you want to go beyond these previews and see the full context, including risks and detailed assumptions, you can review the wider set of Align Technology Narratives alongside the current market price to judge which story feels closer to your own view.

Do you think there's more to the story for Align Technology? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.