Assessing Amcor (AMCR) Valuation After Reverse Stock Split And Ahead Of Unsettled Earnings Report

AMCOR PLC AMCR | 39.93 | -1.89% |

Amcor (AMCR) has just completed a 1-for-5 reverse stock split and is heading into a closely watched December quarter earnings report, with sentiment around its near term earnings prospects still unsettled.

After the reverse stock split and ahead of the December quarter earnings release, Amcor’s recent 90 day share price return of 12.59% contrasts with a 1 year total shareholder return decline of 4.04%. This suggests shorter term momentum against a weaker longer term picture at a latest share price of $44.19.

If Amcor’s update has you reassessing packaging and manufacturing exposure, it can also be useful to cast a wider net and look at fast growing stocks with high insider ownership as potential ideas for your watchlist.

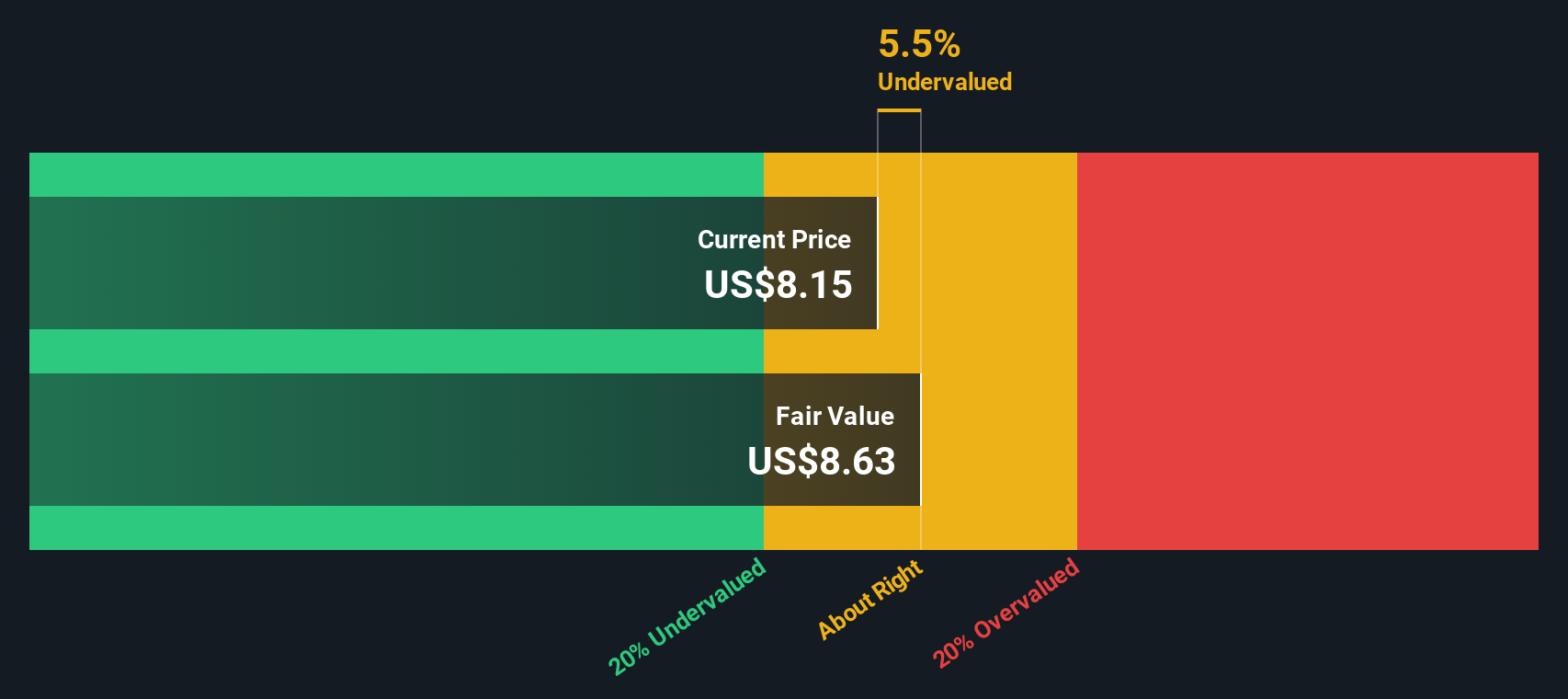

With shares up 12.59% over 90 days but showing a 4.04% decline over 1 year, a 56.57% intrinsic discount and a 24.49% gap to the latest analyst target raise the key question: is this a genuine mispricing, or is the market already factoring in future growth?

Most Popular Narrative: 783.8% Overvalued

According to the most followed narrative, Amcor’s fair value of $5.00 sits far below the recent $44.19 price, setting up a sharp valuation gap that hinges on how investors weigh leverage, cash flows and long term dividend appeal.

Free Cash Flow: 5 year average 815 million dollars (described as volatile). Buffett’s preferred: Consistent and growing. Status: ⚠️. Explanation: Five year average FCF is solid but TTM free cash flow of roughly 725 million dollars is depressed by integration and transaction costs.

Curious how a mature packager ends up with such a low fair value against today’s price? The narrative leans heavily on modest earnings progress, pressured margins and a future profit multiple that looks more demanding than the headline growth might suggest. Want to see which cash flow assumptions and profit profile sit behind that $5.00 figure and why they point to such a steep gap?

Result: Fair Value of $5.00 (OVERVALUED)

However, this 783.8% valuation gap could narrow quickly if merger synergies improve earnings clarity or if deleveraging progress shifts sentiment on Amcor’s balance sheet risk.

Another View on Amcor’s Valuation

That user narrative points to a very low fair value around $5.00, but our DCF model presents a different picture. On those cash flow assumptions, Amcor at $44.19 is described as trading well below an estimated future cash flow value of $101.74. This comparison suggests a wide valuation gap in the other direction. So which story do you think better reflects the risks around leverage, margins and growth?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Amcor for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Amcor Narrative

If you see the numbers differently or prefer to lean on your own work, you can quickly build a custom Amcor narrative in just a few minutes, starting with Do it your way.

A great starting point for your Amcor research is our analysis highlighting 3 key rewards and 5 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Amcor is only one piece of your watchlist, give yourself a broader view by lining up a few more targeted ideas that might suit your style.

- Spot potential value ideas early by reviewing these 877 undervalued stocks based on cash flows built around cash flow focused fundamentals.

- Tap into the growth story in machine learning and automation by scanning these 24 AI penny stocks for companies tied to this theme.

- Turn income into a core part of your approach with these 14 dividend stocks with yields > 3% that concentrate on yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.