Assessing Arbor Realty Trust (ABR) Valuation After Strong Sell Analyst Rating And Weaker Earnings Outlook

Arbor Realty Trust Inc ABR | 0.00 |

Analyst downgrade puts Arbor Realty Trust (ABR) under closer investor scrutiny

Recent analyst coverage assigning Arbor Realty Trust (ABR) a strong sell rating, tied to declines in earnings estimates and projected year-over-year drops in quarterly and full-year earnings and revenue, has pulled fresh attention to the stock.

At a share price of $7.88, Arbor Realty Trust shows mixed momentum, with a 5.07% 1 month share price return and 3.28% 3 month share price return set against a 12.80% 1 year total shareholder return decline. This suggests that recent strength has yet to offset longer term weakness in investor sentiment.

If this kind of uneven performance has you comparing options, it could be a good moment to see what else is moving and check out 17 top founder-led companies

With the stock trading below both its stated intrinsic value estimate and the average analyst price target, yet facing weaker earnings expectations, you have to ask: is ABR mispriced, or is the market already discounting its future growth?

Price-to-earnings of 14.1x: Is it justified?

At a last close of $7.88, Arbor Realty Trust trades on a P/E of 14.1x, which screens as good value against peers on some measures, but looks expensive on others.

The P/E multiple compares the current share price to earnings per share and is a quick way to see how much investors are paying for each dollar of profit. For ABR, the stock is described as good value versus the peer average P/E of 20.4x and close to its estimated fair P/E of 14.3x. Yet it is also labeled expensive versus the wider US Mortgage REITs industry average of 11.4x. That mix suggests the market may be assigning a premium to ABR relative to the sector, while still pricing it below a subset of higher rated peers.

Compared to the industry, the current 14.1x looks meaningfully higher than 11.4x, which points to a richer earnings multiple than many Mortgage REITs. However, with the fair ratio estimate sitting at 14.3x, the current multiple is also described as broadly in line with what the SWS fair ratio model suggests the market could settle around if pricing tracks underlying fundamentals more closely.

Result: Price-to-earnings of 14.1x (ABOUT RIGHT)

However, weaker annual revenue growth and recent negative 1 year and 5 year total returns mean sentiment could sour further if earnings or credit quality disappoint.

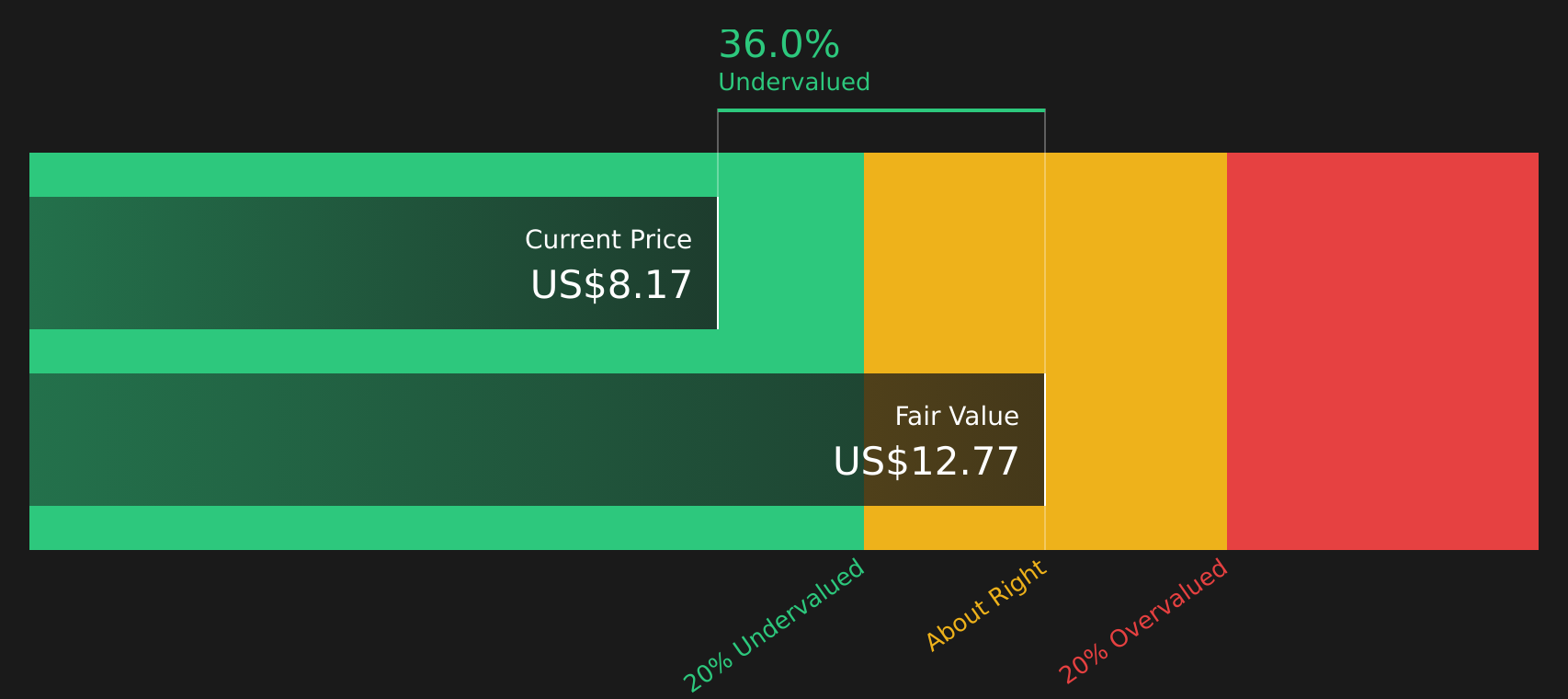

Another angle on value: cash flows paint a different picture

While the 14.1x P/E suggests ABR is roughly in line with its 14.3x fair ratio, our DCF model tells a different story. With the stock at $7.88 and an estimated future cash flow value of $12.58, ABR screens as trading at a 37.4% discount. This raises a simple question: is this a margin of safety or a signal that cash flow assumptions are too optimistic?

For a closer look at how this cash flow view is built, and what could cause it to change, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Arbor Realty Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly mixed, this is the moment to look past the headlines, review the underlying numbers, and form your own view using the 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If ABR has raised questions, do not stop there. Broaden your watchlist with a few focused stock ideas that match how you like to invest.

- Target potential upside with companies that pair quality fundamentals and attractive pricing by reviewing the 48 high quality undervalued stocks.

- Strengthen your income focus by zeroing in on higher yielding opportunities using the 12 dividend fortresses.

- Reduce portfolio stress by concentrating on businesses that score well on resilience with the 70 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.