Assessing Arbor Realty Trust (ABR) Valuation After Weak Earnings And Dividend Cut

Arbor Realty Trust Inc ABR | 0.00 |

Arbor Realty Trust (ABR) is back in focus after a weak Q1 2026 earnings report, a cut in the common dividend from US$0.30 to US$0.17, and rising distress in its US$12b loan book.

Those pressures are clearly reflected in Arbor Realty Trust’s share price, with a 30 day share price return down 26.35% and a year to date share price return down 33.21%, while the 1 year total shareholder return has declined 42.41%. This points to fading momentum as investors reassess risk.

If the stress in commercial real estate has you rethinking where you look for opportunities, it may be worth scanning 20 top founder-led companies

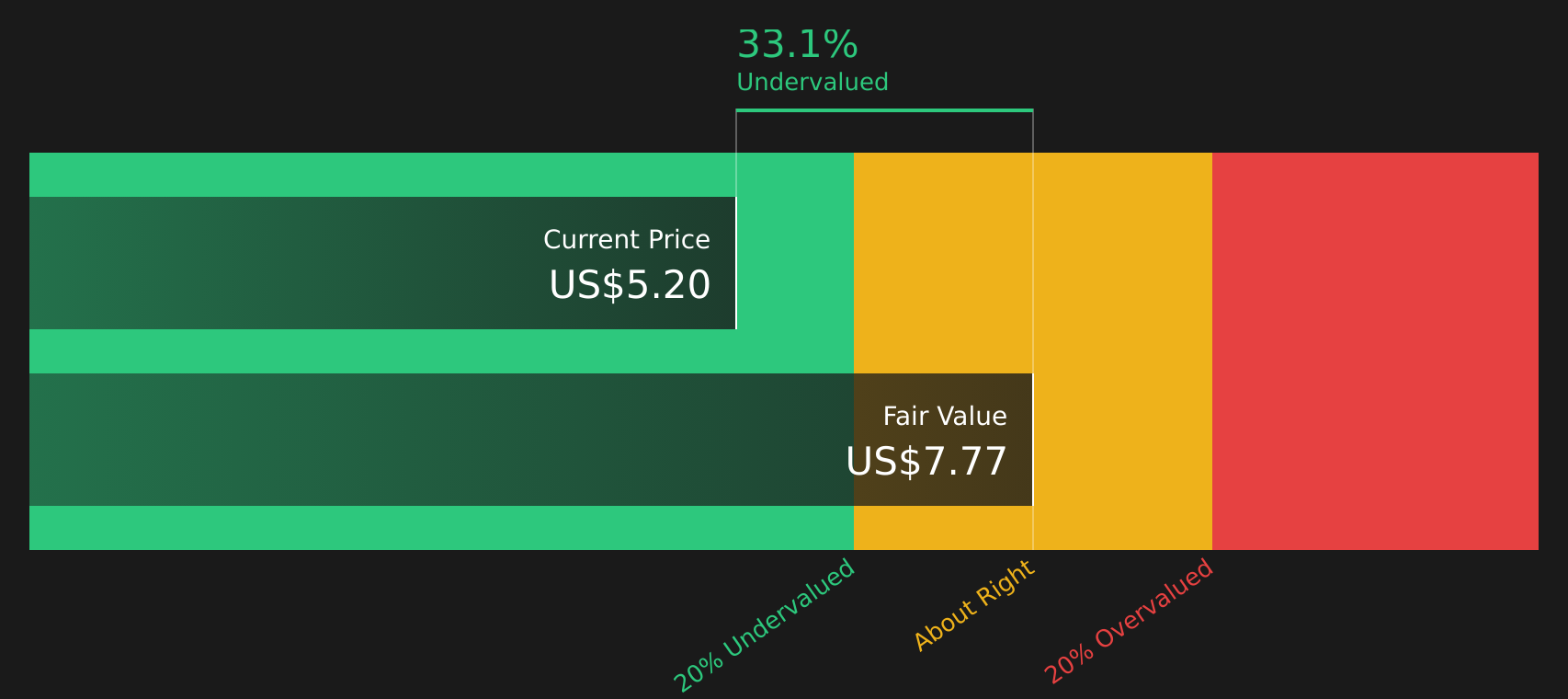

With the stock down sharply, trading at US$5.31 and at a reported discount to some analyst and intrinsic estimates, you need to ask whether ABR is now trading below its underlying value or if the market is already bracing for weaker growth.

Price-to-Earnings of 13.2x: Is it justified?

On a P/E of 13.2x, Arbor Realty Trust does not screen as outright cheap, despite the share price sitting at $5.31 and trading below some valuation estimates.

The P/E multiple compares the current share price to the company’s earnings per share and is a common way to see how much investors pay for each dollar of earnings. For Arbor Realty Trust, the current level is framed as good value against its peer group, with the stock described as good value based on its P/E of 13.2x versus a peer average of 15.3x.

However, that same 13.2x P/E is described as expensive versus the broader US Mortgage REITs industry at 11.2x and also sits above the estimated fair P/E of 12.5x. Our fair ratio work suggests the market could trend toward that level over time. That mix of signals implies the stock looks relatively cheap compared to closer peers, but still carries a premium to the wider industry and to the level suggested by the fair ratio model.

Against that backdrop, the stock is also flagged as trading 32.4% below an internal fair value estimate based on a discounted cash flow model, with Arbor Realty Trust at $5.31 compared to an estimated future cash flow value of $7.85. The DCF, which projects future cash flows and discounts them back to today, effectively assumes the market is pricing in weaker cash generation than that model implies.

Result: Price-to-Earnings of 13.2x (ABOUT RIGHT)

However, you also need to weigh rising stress in the US$12b loan book and a near 49% annual revenue decline, which could pressure the resilience of earnings.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Paint a Different Picture

While the 13.2x P/E sits slightly above the 12.5x fair ratio, the SWS DCF model points in a different direction, with ABR at $5.31 compared with an estimated future cash flow value of $7.85. If cash flows are closer to the mark than earnings multiples, is the current discount giving you enough comfort?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Arbor Realty Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between pressure on earnings and potential valuation support, it may be useful to move quickly and weigh the signals for yourself using the 3 key rewards and 4 important warning signs.

Looking for more investment ideas?

If ABR has sharpened your focus on risk and reward, treat that momentum as a cue to broaden your watchlist with other targeted opportunities.

- Target potential value opportunities by scanning 46 high quality undervalued stocks that pair solid fundamentals with room for sentiment to improve.

- Prioritize resilience first by using the 63 resilient stocks with low risk scores and concentrate on companies with lower risk scores that may offer a smoother ride.

- Seek out future potential by reviewing the screener containing 21 high quality undiscovered gems before more investors start paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.