Assessing Ashland (ASH) Valuation After A Modest Dividend Increase And Mixed Shareholder Returns

Ashland Inc. ASH | 0.00 |

Ashland (ASH) has declared a quarterly cash dividend of $0.42 per share, a 1.2% increase from the prior payout. This move highlights ongoing cash returns to shareholders ahead of its May investor conference.

While the dividend increase may appeal to income investors, the stock’s performance has been more mixed. The share price is down 7.85% over 90 days, but this is offset by a 12.01% one year total shareholder return, indicating that momentum has cooled in the near term.

If you are weighing Ashland against other opportunities, this could be a good moment to scan the market for fresh ideas through our screener of 19 top founder-led companies

With Ashland trading at $56.15, sitting at a discount to analyst targets and an indicated intrinsic value, the key question is whether that gap signals mispricing or whether the market already reflects the company’s future growth.

Most Popular Narrative: 16.3% Undervalued

Ashland’s most followed narrative places fair value at $67.10 per share versus the recent $56.15 price, framing the stock as trading at a visible discount.

The global shift toward sustainable and bio-based materials, driven by regulatory requirements and consumer preference, continues to gain momentum, benefiting Ashland's specialty chemicals portfolio that is now more focused on high-value, sustainable, and compliant solutions; this is expected to support top-line revenue growth and margin resilience over the long term.

There is a full earnings roadmap behind that fair value, tying together revenue growth assumptions, a sharp profit margin reset and a future earnings multiple below many peers. The tension between modest sales growth and much stronger profitability expectations is at the core of this narrative, and those moving parts are what investors tend to scrutinize most closely.

Result: Fair Value of $67.10 (UNDERVALUED)

However, this depends on demand holding up in key personal care and life sciences markets, and on cost savings continuing once current manufacturing and restructuring programs run their course.

Another Angle on Valuation

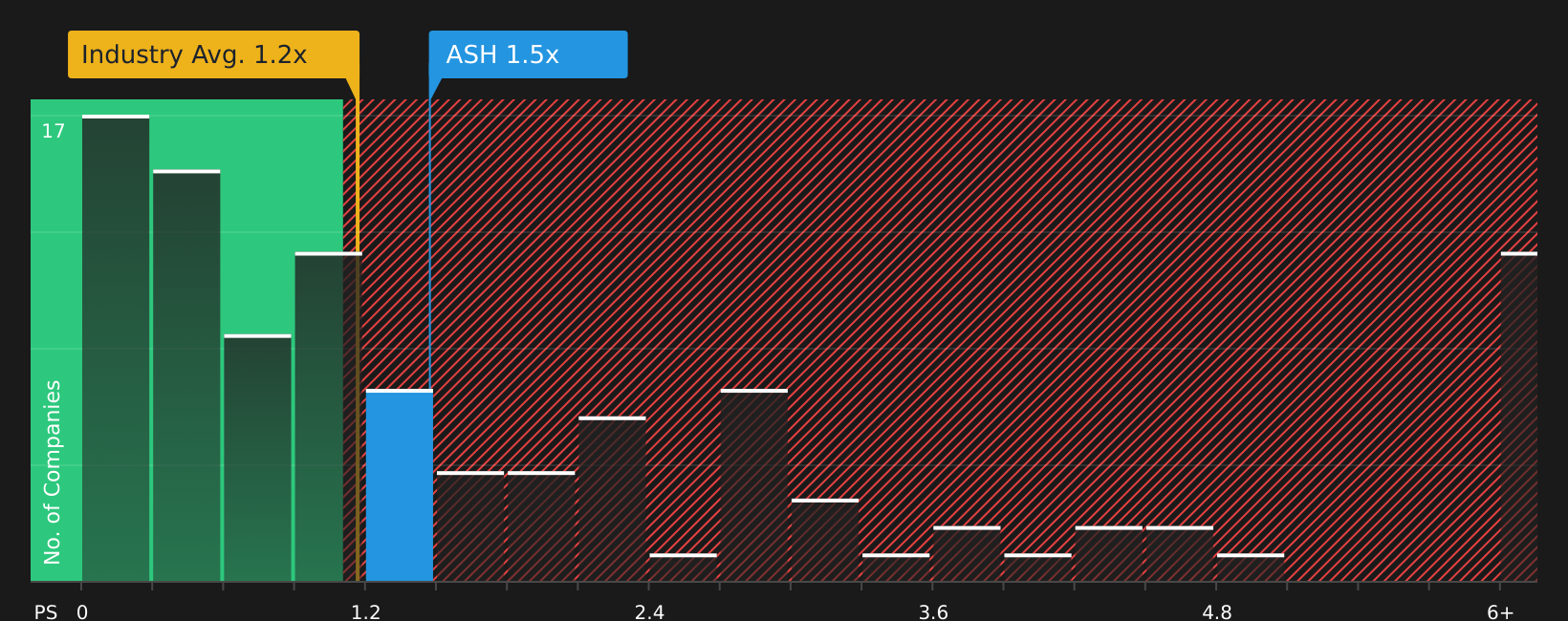

While the narrative suggests Ashland is trading below fair value based on future cash flows, the current P/S of 1.4x looks similar to both the US Chemicals industry at 1.2x and peers at 1.4x, with a fair ratio also at 1.4x. So is this really a clear discount, or just in line with the pack?

To stress test that question against the current pricing, take a closer look at how the numbers line up in our valuation breakdown. Start with the fair ratio view, then see how it might shift if sentiment or growth expectations change.See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mix of optimism and caution in this story feels familiar, that is exactly why it is worth checking the full risk and reward profile yourself using the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop with a single stock when you can quickly line up other candidates that match your goals and see how they compare side by side.

- Spot potential turnaround opportunities early by scanning 27 elite penny stocks with strong financials that pair smaller market sizes with stronger financial profiles.

- Hunt for quality at a reasonable price by reviewing the 47 high quality undervalued stocks that combine solid fundamentals with compressed expectations.

- Prioritize resilience by focusing on 67 resilient stocks with low risk scores that score well on financial strength and risk metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.