Assessing Avista (AVA) Valuation After First Quarter Earnings Show Mixed Revenue And Profit Trends

Avista Corporation AVA | 0.00 |

First quarter earnings as a fresh signal for Avista stock

Avista (AVA) stock is back in focus after first quarter 2026 results showed revenue of US$570 million versus US$617 million a year earlier, while net income reached US$92 million and earnings per share from continuing operations came in at US$1.11.

At a share price of US$40.56, Avista has had a 4.75% year to date share price return, while the 1 year total shareholder return is 1.59%. This hints at fading near term momentum but steadier long term gains.

If earnings volatility in utilities has you thinking about diversification, this could be a good moment to look at 36 power grid technology and infrastructure stocks as another way to find ideas in the grid and infrastructure space.

So with Avista trading at US$40.56, sitting close to one analyst price target and carrying a middling value score, are you looking at an undervalued utility stock here, or is the market already pricing in future growth?

Most Popular Narrative: 5.2% Undervalued

With Avista’s fair value narrative sitting at $42.80 against a last close of $40.56, the current price lines up closely with a modest undervaluation story built around regulated growth and grid investment.

The sharp rise in large industrial and commercial load inquiries, with over 3,000 megawatts in the pipeline compared to a roughly 2,000 megawatt current peak load, signals accelerating electrification and potential for outsized rate base and revenue growth if even a fraction of these loads materialize over the next 3 to 5 years. Robust, multi-year capital investment plans approaching $3 billion (2025 to 2029), with additional potential from grid expansion projects and new generation needs tied to large load requests, position Avista to earn regulated returns and support long-term earnings expansion.

Curious what has to happen in the income statement for that fair value to hold up? The narrative focuses on steady load growth, firmer margins and a richer earnings multiple. The exact mix of revenue assumptions, profitability shift and valuation premium is where the story gets interesting.

Result: Fair Value of $42.80 (UNDERVALUED)

However, keep an eye on wildfire exposure in the Pacific Northwest and the potential for less constructive rate decisions, either of which could quickly weaken this fair value story.

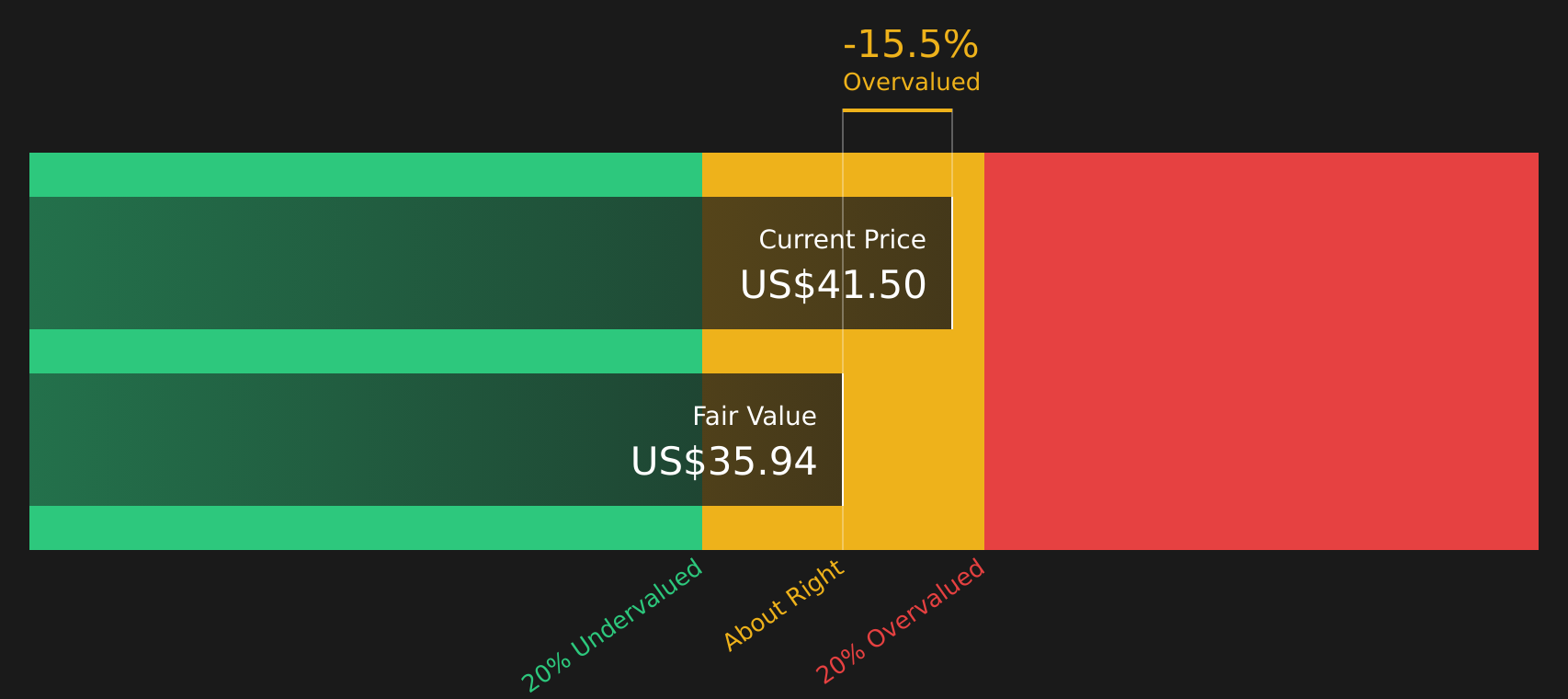

Another View: Cash Flows Paint a Different Picture

There is a clear tension between the modest 5.2% undervaluation suggested by analyst targets and the output of our DCF model, which points to a fair value of $36.25, below the current $40.56 share price. On that view, Avista looks overvalued. Which story do you think fits your own assumptions better?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Avista for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of risks and rewards feels finely balanced, it is worth looking through the data yourself and deciding how it lines up with your own expectations. To see both sides set out clearly, start with the full breakdown of 4 key rewards and 2 important warning signs

Looking for more investment ideas?

Once you have a view on Avista, do not stop there. The market is full of other opportunities that could fit your goals just as well.

- Target resilient compounding by checking out 70 resilient stocks with low risk scores that aim to keep portfolio swings in check while still pursuing returns.

- Hunt for quality at a discount by scanning screener containing 25 high quality undiscovered gems that many investors may not be watching yet.

- Strengthen your core holdings by focusing on the solid balance sheet and fundamentals stocks screener (44 results) and keep your capital tied to sturdier financial foundations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.